The Elusive R-Star: The Fed's Key to Ending Rate Hikes

Issue 64

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🧠 Sound smart? Feed your brain with weekly issues sent directly to your inbox:

Today’s Bullets:

All the ‘Flations

What is R-Star?

Historical R-Stars

Fed is TIPS-y

Is the Fed Done Raising Rates?

Inspirational Tweet:

Jurrien lays out a case here for the Fed to pause rate raises after the May meeting, where—after that Tweet—the Fed raised rates by yet another 25 basis points (.25%). This marked the seventh consecutive rate increase since the Fed began raising rates in 2022.

Wowzer.

But what exactly is the neutral rate (or R*Star, as Jurrien notes above)? How is it determined? And does this mean the Fed is done raising rates now?

If you have no idea what the heck all those questions mean, don’t worry. We’re going to get you all sorted and smarter on Fed-speak today.

Simple. Quick. And a little bit of fun (at the expense of you-know-who).

Let’s get to it.

Join the 🧠Informationist community and get access to every single post + the entire archive of articles, all for a fraction of the cost of a college finance course.

You’ll learn a whole lot more, faster and easier. That’s my guarantee.

Partner spot

Some of you have been asking recently what I read in the morning for fast, digestible news, and I’m happy to report that my new favorite source, hands down, is 1440.

The folks at 1440 scour over 100 sources every morning so you don't have to. You'll save time and start your day smarter. What more could you ask for?

Sign up for 1440 now and get your first issue, immediately. It's completely free—no catches, no nonsense, and absolutely no BS. I wouldn’t recommend it, if I wasn’t sure you’d love it, too.

Join 1440 for free today.

🎯 All the ‘Flations

Last week, we talked about hyperinflation, so let’s run through the other terms describing economic conditions regarding the ‘flations today.

If you missed last week’s study of hyperinflation, you can find that here:

Could the US Dollar Hyperinflate?

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week. 🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

Outside of hyperinflation, we have inflation, stagflation, disinflation, deflation, and reflation.

We know what inflation is, we’ve been talking about that problem for over a year now. But lately we’ve been hearing the term stagflation being tossed around.

So, what is it?

Stagflation is the phenomenon of prices of goods and services continuing to rise while the economy stagnates or even begins to shrink. In other words, prices are rising for companies and consumers, yet profitability is not keeping up.

And this means that even though GDP may be rising, it is negative when including the rate of inflation. Reasons for stagflation can be things like serious and ongoing supply chain issues, high energy costs, monetary manipulation, and of course, all three of the above.

In short, stagflation is not good for consumers. Not good for businesses. Not good for the Treasury.

And not good for policymakers. It puts them in quite a pickle.

raise rates → economy gets worse

lower rates → inflation gets worse

What’s the opposite of nirvana?

You could say that the onset of stagflation is the epitome of this chart for the Fed.

Then we have disinflation, where the Fed insists we are currently at in this cycle of monetary manipulation, er…policy.

Disinflation just refers to a decrease in the rate of inflation—that is, prices are still rising, but at a slower pace. Disinflation can be a sign that the Fed Funds rate has surpassed the neutral rate.

R-Star. (Don’t worry, we will get to that in a bit)

Deflation on the other hand, refers to a decrease in price levels.

The opposite of inflation.

Deflation can occur because the Fed Funds rate has far exceeded the neutral rate, and it can also happen because of natural technological forces, such as revolutionary technology being introduced that expands productivity significantly.

Repeat after me: AI and ChatGPT.

Now we would not yet be seeing broad price decreases because of this new technology, as it will take a bit for that to filter into and impact the economy.

But that force is likely coming.

This will fight the Fed’s need for inflation, something my good friend Jeff Booth explains in his book The Price of Tomorrow (highly recommended, BTW).

But we aren’t talking about that quandary today, just the Fed’s problem with manipulating money to achieve its ideal rate of inflation, regardless of the forces out there.

And once the Fed over-tightens access to capital by raising rates and removing liquidity from the system with quantitative tightening (QT), they will start to look to inflate prices once again.

Reinflation.

Sounds like a stupid and totally unnecessary financial rollercoaster they put us on, doesn’t it?

Fact is, the Fed will likely slam us into a painful recession, where jobs are lost, prices decrease, GDP falls significantly, along with—you got it—taxes.

And we can’t have that. Not with all the debt on our books and the need to pay those Treasury coupons.

No sir.

So, the Fed will open the floodgates, inject money into the supply, and lower rates, while Wall Street, all the while, chants:

Do not wait. Re-inflate!

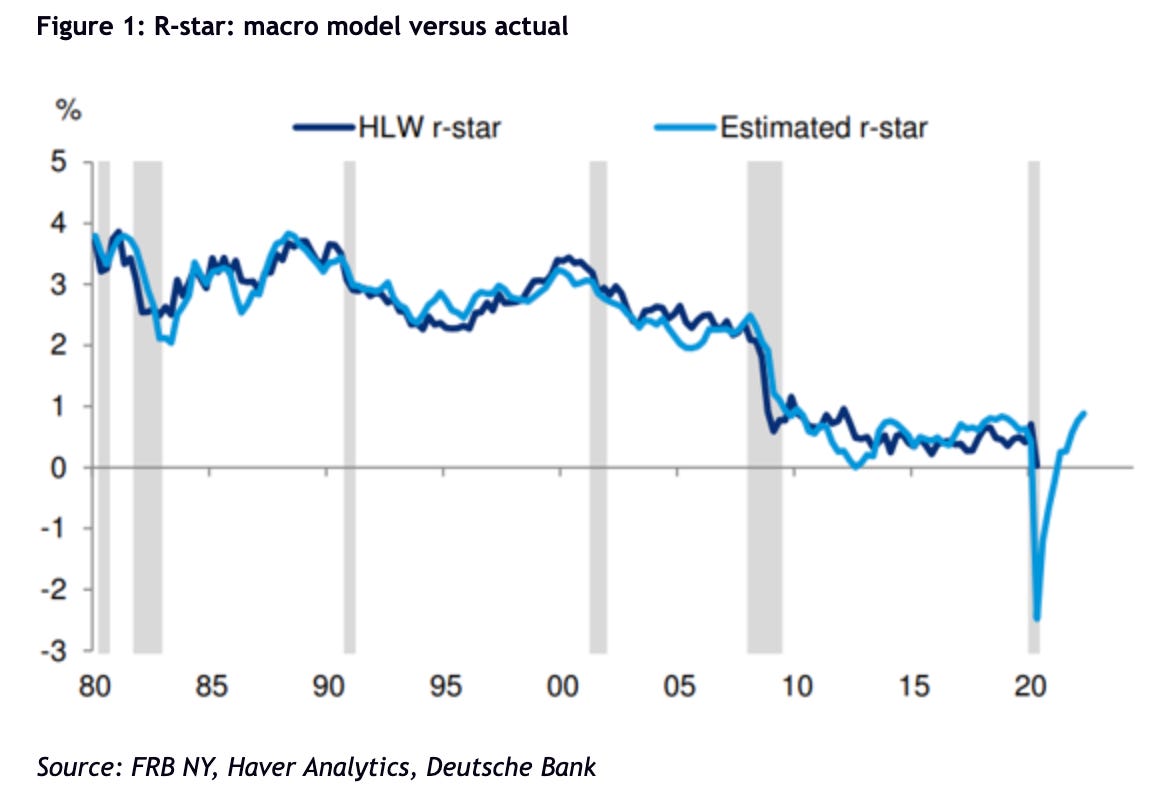

🔍 What is R-Star?

Back to R-Star.

Also known as r*, or the neutral rate, or the natural rate of interest (they have a whole lot of terms for that elusive level, don’t they?), R-Star is a theoretical concept in economics.

It's basically defined as the real interest rate (Fed Funds minus Inflation Rate) where with the economy is operating at its full potential, and theoretically, there's full employment, stable inflation at the targeted rate (they say that’s 2%), and sustainable economic growth.

R-Star is essentially the sweet spot where the economy is in equilibrium, without the need for monetary policy to either stimulate or slow down economic activity.

When at that magic level, we’re not inflating beyond that 2%, not disinflating or deflating or stagflating and there’s no need for reflating.

No need to raise or lower rates.

We are at r*.

Ahhhhhh. Nirvana.

Problem is, there’s no way to truly measure or observe R-Star, and so it’s little more than an economic exercise based on estimated current conditions.

What’s more, R-Star is a moving target due to constantly evolving economic conditions and demographics.

Here’s the kicker.

Ever since the pandemic blew up the Fed’s own R-Star models, the NY Fed stopped publishing its own estimates.

oops.

So, economists (like the ones at Deutsche Bank or Fidelity, who created the estimates in Jurrien’s chart above) are doing their best to estimate what the Fed is estimating.

A derivative on a derivative.

Awesome.