💡The Dangerous Hedge Fund Basis Trade

Issue 160 - FREE FULL VERSION

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🫶 If this email was forwarded to you, then you have awesome friends, click below to join!

👉 And you can always check out the archives to read more of The Informationist.

Today’s Bullets:

What’s the Basis Trade?

Dangers of the Basis Trade

What’s the Fed Considering?

The End Result

Inspirational Tweet:

Here we go again.

Hedge funds have reportedly plowed capital back into the so-called Basis Trade, using massive leverage this time and setting themselves up, and the rest of the markets for that matter, for a cataclysmic implosion.

Hold on, you say, what is this Basis Trade, and how are they leveraged?

And are you saying, the hedgies didn’t learn their lesson from the last (two) time(s)???

Say it isn’t so!

Well, if all this has you scratching your head in wonder and worry, have no fear. Because we are going to unpack this Basis Trade business and the risks that come with it for both you and me, right here today.

And we are going to do it nice and easy, as always.

So pour yourself a nice big cup of coffee and settle into your favorite chair for some simplified bond-speak with this Sunday’s Informationist.

Partner spot

America's Most Secure Mobile Service

Really quickly and before we start, I cannot stress this enough. If you’re not protecting yourself from cyber attacks and SIM-swaps, you’re at serious personal risk these days. After seeing four of my colleagues go through the nightmare of SIM-swaps (someone literally taking control of your phone from afar)—identities stolen, bank accounts compromised, emails hijacked, social media held for ransom—I knew I was at risk, too.

So, I switched to a service called Efani, and it was super easy and seamless. It feels just like being with Verizon or AT&T—because you are—but with layers of security, I can rest easy knowing that my phone is ultra-secure. My colleagues learned the hard way, but now we’re all on Efani, and I couldn’t be happier. I honestly wouldn’t share this with you if I didn’t completely believe in the service myself. Whether you use Efani or something else, please don’t wait until it’s too late to protect yourself.

And if you choose Efani by using the link below, you’ll get $99 OFF.

The Efani SAFE plan is a bespoke cybersecurity-focused mobile service protecting high-risk individuals against mobile hacks, providing best in class protection with 11-layers of proprietary authentication backed with $5M Insurance Coverage. Don’t wait. Protect yourself today.

🧐 What’s the Basis Trade?

As you likely know, hedge funds are always looking for ways to generate profits. And the best of these can be through arbitrage.

You know, capturing true inefficiencies in the markets, where one security is worth the same as another but trading at a different price.

You can imagine how, when they find such an opportunity, they employ leverage to enhance the returns.

Since, you know, they’re really just crumbs of inefficiency, not chunks.

The leverage multiplies these crumbs and makes them more bite-size, more enticing.

I mean, instead of a penny on a hedged trade, if they leverage the trade 20X, that penny becomes 20 cents.

And if they lever it up 50X, well…you get the point…

So, what is this Basis Trade opportunity, and how are they levering it up?

Pretty simple. The hedge fund will buy a US Treasury and then hedge against it (sell short) a similar futures security.

Huh?

Here’s how it works: funds buy long-term Treasury bonds (say, 10-year notes yielding 4%) while shorting Treasury futures contracts tied to the same maturity.

The futures price typically trades at a slight discount to the cash bond price due to financing costs and market mechanics, creating a spread—often just 10-20 basis points (0.1%-0.2%).

This trade is dollar-neutral: profits don’t hinge on bond prices rising or falling, just the spread getting smaller.

But the real juice comes from leverage.

Funds borrow heavily in the repo market—where they pledge the Treasuries as collateral for short-term loans at ever-so slightly lower rates—and then amplify their positions.

With $1 billion in capital, a fund might control $10 billion to $20 billion in Treasuries at 10:1 or 20:1 leverage.

And a 15-basis-point spread on $10 billion nets $15 million annually—a 1.5% return unlevered.

But levered 10X, that becomes $150 million, or a 15% profit.

Here are 5 Keys to the Basis Trade:

Borrowing at Low Rates: Hedge funds typically borrow in the short-term funding markets, often through repurchase agreements (repos). In a repo, they sell securities (like Treasuries) to a lender with an agreement to buy them back later at a slightly higher price, effectively paying an interest rate on the loan. Repo rates are usually low because they’re secured by collateral and tied to short-term benchmarks like the Secured Overnight Financing Rate (SOFR).

Investing in Higher-Yielding Treasuries: The borrowed funds are used to buy longer-term US Treasuries, like 10-year or 30-year bonds, paying higher yields due to the term premium (longer maturities carry more risk, so they pay more). I.e., if the repo rate is 3.5% and the 10-year Treasury yields 4%, the fund pockets a 50 basis point (.5%) spread on the notional amount.

Leverage: To amplify returns, hedge funds borrow significantly more than their own capital. For instance, with $1 million of their own money, they might borrow $9 million via repos, controlling $10 million in Treasuries. If the spread is 1%, they earn $100,000 annually on that $10 million, a 10% return on their $1 million, minus borrowing costs and fees. Leverage ratios can vary widely, from 5:1 to 20:1 or more, depending on risk appetite and market conditions.

Financing Mechanics: The repo market is key. It’s liquid and allows funds to roll over short-term loans daily or weekly, while holding long-term bonds. They post the Treasuries as collateral, so lenders feel secure. Hedge funds may also use prime brokers, who provide financing and facilitate trades, usually at competitive rates due to their scale.

Profit and Risks: The profit comes from the yield spread, magnified by leverage. But it’s not risk-free. If short-term rates spike (raising borrowing costs) or long-term yields drop (raising bond prices), the trade can turn unprofitable. Leverage amplifies losses too. Using the example above, a 1% price drop on $10 million of bonds wipes out $100,000, a 10% loss on the fund’s $1 million equity. Other risks include margin calls (if collateral values fall) or liquidity crunches in the repo market.

The Basis Trade: A Super Simple Example

🎯 What’s the Goal?

Make money by exploiting a tiny price difference between a Treasury bond and its futures contract—without betting on interest rates going up or down.

⚙️ The Setup

You buy a 10-year Treasury bond for $100. It pays a 4% annual yield (like a coupon).

You don’t have $100, so you borrow the money in the repo market at 3% annual cost. Here’s how:

You lend the $100 bond to a repo counterparty (like a money market fund).

They give you $100 in cash to fund the purchase, and you agree to buy the bond back later.

You pay 3% interest for borrowing the cash.

You sell a Treasury futures contract (same bond, delivers in 3 months) for $100.50.

Step 1: The Bond Side

You earn 4% on the bond = $1 over 3 months ($100 × 4% × 0.25).

You pay 3% to borrow in the repo market = $0.75 over 3 months ($100 × 3% × 0.25).

Net: $1 - $0.75 = $0.25 profit from holding the bond.

Step 2: The Futures Trick

The futures price ($100.50) is a bit “rich” (overpriced) compared to the bond’s value. By the time the futures contract ends in 3 months, its price has to match the bond’s price—let’s say the bond is still worth $100.

You sold the futures at $100.50.

At delivery, the futures price is $100 (same as the bond).

You “buy back” the futures at $100, making a profit: $100.50 - $100 = $0.50.

💰 Total Profit

From holding the bond: +$0.25 (after borrowing costs).

From the futures: +$0.50 (price convergence).

Total: $0.25 + $0.50 = $0.75 on a $100 bond.

That’s a 0.75% return in 3 months, or 3% annualized ($0.75 ÷ $100 × 4).

🚀 Add Leverage

Hedge funds use leverage to boost returns. If you put up $5 of your own money and borrow $95 (20:1 leverage), that $0.75 profit becomes:

15% return on your $5 in 3 months ($0.75 ÷ $5).

Annualized: 15% × 4 = 60%!

And that’s what hedge funds loooooooove this trade 😍

Tiny price differentials + lots o’ leverage = bigly profits 🤩

Bigly profits = Huge-O Bonuses 🤑

But what if prices move the wrong way?

What happens then?

Good question. Let’s talk about that.

⛷️ Dangers of the Basis Trade

You ever hear the expression, if you owe the bank $1 million it’s your problem, but if you owe the bank $100 million it’s the bank’s problem?

This situation is kind of like that.

See, this is not the first time that hedge funds have ventured over their ski-tips, so to speak.

Some of you may recall 1998 and the Long-Term Capital Managment debacle.

Or heard me talk about it before.

I won’t go too deep into it here, but to simplify, LTCM ran a similar playbook, leveraging bond spread bets as much as 100:1. When Russia defaulted, spreads blew out, and LTCM’s $4 billion in equity vaporized against $100+ billion in positions.

The Fed brokered a $3.6 billion private bailout to save Goldman Sachs (heavily exposed to the LTCM counterparty risks) and avert a systemic collapse.

For those of you who are interested and want to understand that financial disaster better, Roger Lowenstein wrote a fantastic book all about it called When Genius Failed.

Highly recommended.

In any case, today’s basis trade echoes LTCM: a sudden shock—like a repo rate spike to 5% or a volatility surge (VIX jumping from 15 to 30)—could cause a similar meltdown.

Except it would be more widespread and harder for the Fed to engineer a backstop.

How widespread and large?

Would you believe over $1 trillion?

That’s right. Because the long borrowed repo side of the trade does not show up here, the short futures leg is what gives us clues to the size of the hedge fund exposure out there.

And that looks to be about $1 trillion today.

Yikes.

This is why the Brookings Institute (see the source of the above chart) is looking at the problem and studying ways for the Fed to mitigate or eliminate it altogether.

Because if we have another repo crisis, like we did in March of 2020, the Treasury market could have something of a meltdown.

How?

Take a peek at this chart that shows the spread between cash Treasuries and their corresponding futures contracts, measured in basis points (1/100th of a percent). AKA, the spread of the basis trade.

What do we notice?

Pre-2020: The basis hovered mostly between -25 and +25 bps—relatively tight, manageable spreads

March 2020 Spike: A massive blowout to nearly +100 bps, during the COVID liquidity crisis

This sudden widening meant cash Treasuries were selling off hard, while futures were not falling as fast—creating huge losses for those holding the long cash/short futures position

Basis trades blew up, and the Fed had to intervene with emergency repo and QE measures

Post-2020: The basis returned to a more normal range, but with additional volatility, mostly due to rate hikes and debt ceiling drama in the last two years.

Remember. Even 15–30 bps swings here can crush a leveraged book.

But in 2020, the cash-futures basis spread spiked to over 70 basis points, compared to a typical spread of around 5 basis points. Dysfunction and contagion spread to other parts of the market, with Treasury bid-ask spreads more than quadrupling and repo rates also rising significantly.

Oops.

So what does this mean for the Basis Trade?

Simple.

When you're levered 20x–50x, a 20 basis point move against you isn't a headache—it's a catastrophic hit to P&L.

If a fund is:

Long $1 billion in cash Treasuries

Financed via repo

Short futures to hedge

A 20 bps basis widening means:

$2 million in losses per $100 million of exposure

At 20x leverage, that’s a 40% capital drawdown

Now multiply that across the $1T of global basis trades and you can see why Brookings is getting nervous.

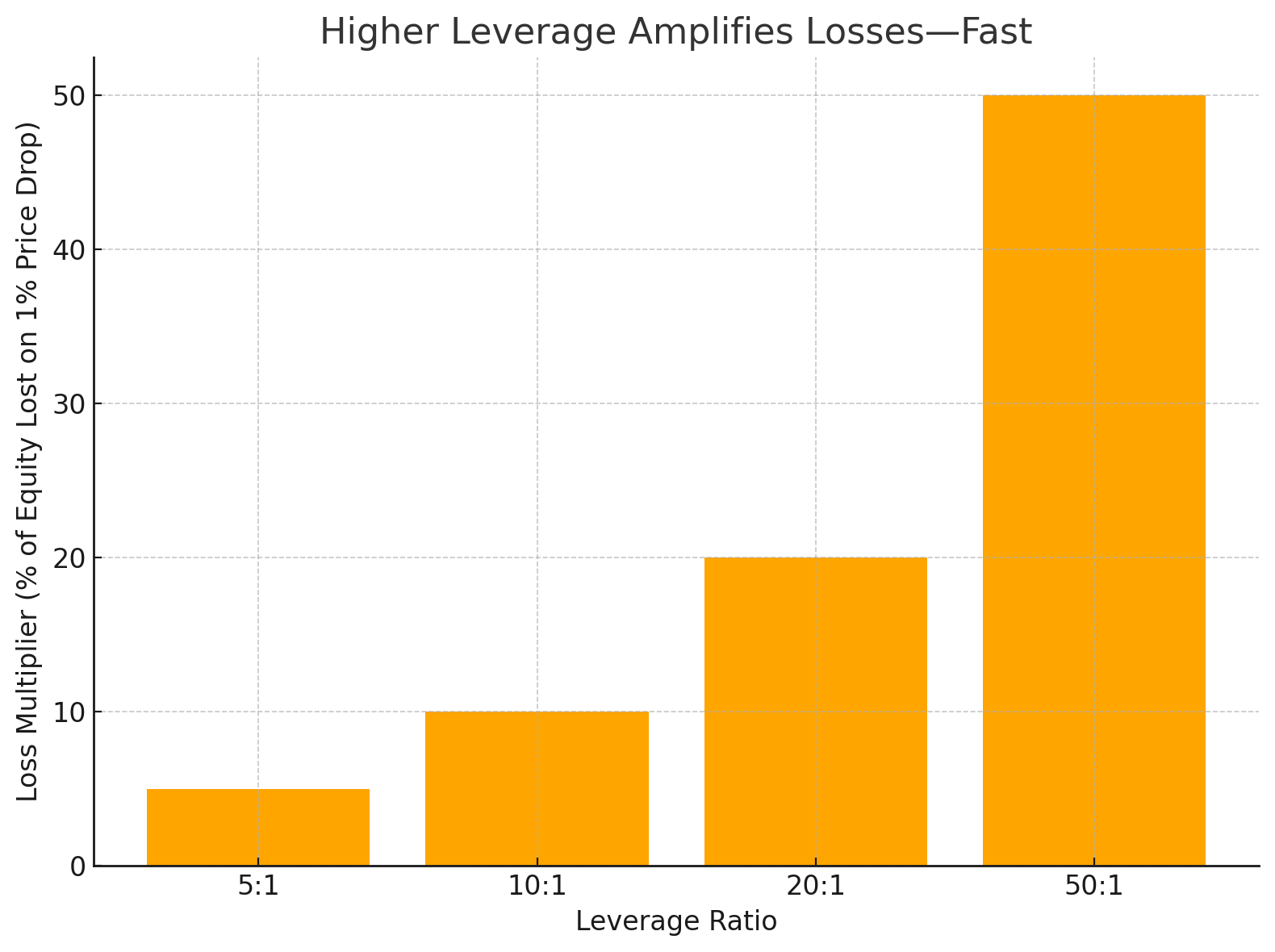

Per usual, leverage is the killer here.

Look at how brutal a simple 1% bond price drop becomes under extreme leverage: a full 50% equity wipeout at 50:1.

OK, so what does Brookings say the Fed should do?

🤨 What’s the Fed Considering?

First, the Brookings Institution is a century-old DC think tank, known for centrist policy research. But more relevant here: it’s an intellectual incubator for many Fed and Treasury officials.

Think of it as the Fed’s quiet brainstorming arm.

Brookings has floated ideas that later became policy—like the Sahm Rule (used for early recession detection) and various QE mechanisms.

To be clear: When Brookings studies something, it’s not just academic—it often signals what policymakers are preparing for.

So, what’s the Fed considering?

To put it simply, Brookings is studying a Fed-backed liquidity tool that would effectively allow the central bank to backstop the Treasury carry trade—by putting it on the Fed’s own balance sheet.

Don’t believe me? Read it here yourself.

From the paper:

The authors recommend that the Federal Reserve, in periods of extreme stress, be prepared to take over the hedge funds’ positions…the Fed could stand ready to purchase Treasury securities but it would also, as the hedge funds do, take offsetting short positions in derivatives.

Wait, the Fed will short Treasury Futures? Take hedged positions?

Right. That’s exactly what the recommendation of the study says:

The Fed would not…worry about how to reduce its holdings once market stress subsides….because the purchases would be hedged, the Fed would not have to take a loss on those holdings if it has to raise interest rates to quell inflation, as it did in the aftermath of the pandemic.

Holy 💩. We’re talking about The Fed just assuming the hedge fund positions, taking them right off their books.

The bailout of all bailouts.

And Brookings’ justification?

…this new approach would be strictly focused on market functioning, preserving…monetary policy actions to support economic growth and employment…[b]ecause the purchases would be hedged, they would not—as the Fed’s COVID-era purchases did—put upward pressure on growth and inflation by pushing down long-term interest rates.

So, let’s get this straight. All get on the same page here, shall we?

What this is saying is that in a crisis, in a moment of distress, the Fed would buy these leveraged Treasury positions directly from the hedge funds, and park them on its own $7 trillion balance sheet.

Why?

To prevent a fire sale that could destabilize the Treasury market, of course.

Good. God.

This is the epitome of QE / not QE.

And unlike LTCM’s all-but-private rescue, this would be public, deliberate, and Fed-led.

This, my friends is where we are at in the debt cycle and relentless leverage of the system.

The leverage is so high, so tightly coiled with loose risk management policies, that the thought of a few hedge funds and their own leverage blowing up, the mere idea of it, has former Fed officials (and likely current ones) scrambling to create a plan to save the system before it implodes on itself.

🤑 The End Result

Make no mistake, if executed, this would mute a market shock and spark a V-shaped recovery—just like the September 2019 repo crisis when the Fed injected $300 billion to calm markets.

But in this new response, liquidity would surge—not from direct Fed printing, but from confidence in the backstop.

Yields would stabilize, and funds could unwind safely.

Well, if “unwind” means unload the trades right onto the Fed’s books, that is...

In 2019, repo rates normalized in weeks, and stocks rallied 10% by year-end.

Here, the Fed owning Treasuries and futures would anchor prices, markets would get a liquidity jolt, indirectly turbocharging risk assets without the Fed cutting rates or doing explicit QE.

What a deal for everyone.

And just like in the 2020 drawdown and liquidity-driven v-shaped recovery, timing the market reversal and getting exposed to risk assets could prove difficult.

Because of this, I personally remain exposed and diversified in holdings of Bitcoin and gold, as well as some cash at the ready (stashed in higher yielding money markets) for deep discounts and market drawdowns.

Because I don’t portend to know if or when or how all of this unfolds.

But one thing remains ultra-clear.

The Fed will do whatever it takes to save the Treasury market.

And by extension, the rest of the markets, too.

And I intend to be ready for it.

That’s it. I hope you feel a little bit smarter knowing about the Hedge Fund Carry Trade and how the Fed may backstop any risks it poses to the markets.

If you enjoyed this free version of The Informationist and found it helpful, please share it with someone who you think will love it, too!

Talk soon,

James✌️

I'm beginning to believe that the deficit doesn't matter..at ..all.. There is always some way that thev fed will save the day... That is as long as the global markets are held together with confidence in the USD and there are countries willing to buy our treasuries? We look at doom and gloom scenarios that seemingly never materialize because the biggest superpowers have too much to lose and are the actually game makers?

Sorry for the technical question from a futures novice...in your example (step 2)...who is the buyer of the Treasury future (100.50)?