💡 Term Premium: Bessent's Brewing Nightmare

Issue 163

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🫶 If this email was forwarded to you, then you have awesome friends, click below to join!

👉 And you can always check out the archives to read more of The Informationist.

Today’s Bullets:

What is Term Premium?

Where is Term Premium Now?

Bessent’s Nightmare

What Bitcoin is Telling Us

Inspirational Tweet:

If you watch CNBC or Bloomberg or maybe follow people like Fidelity’s Jurrien Timmer, you’ve likely heard the phrase “term premium”.

And unless you are finance expert, you’ve also likely thought, what the heck does that even mean?

Perhaps also, why should I care?

And, why would US Treasury Secretary Scott Bessent be so worried about it?

Well, we’re going to answer those questions and a whole lot more today, and we’re going to do it nice and easy, as always.

So, grab yourself a big cup of coffee and settle into your favorite seat for a simplified but important peek into the world of US Treasuries with this Sunday’s Informationist.

🤓 What is Term Premium?

First, let’s unpack just what this so-called Term Premium actually is and how it is calculated.

Or, estimated.

We’re going to keep this all high-level and simple for everyone to grasp the most important concepts, as we like to do around here. And we are going to focus on the 10-year US Treasury for our examples.

Why?

Because, as you may have heard me say before, the 10-year US Treasury is the global benchmark bond.

Not just sovereign bond, but any bond. This is the one that the entire world looks to for clues to financial strength and direction of the largest economy in the world.

We will talk a lot more about that in a bit. Let’s talk about the pricing of a bond first. Specifically, the yield that is demanded by investors to buy the 10-year UST.

See, when you buy a 10-year Treasury bond, you're taking two big risks:

Interest rate risk — rates could rise, pushing down the price of your bond, and

Inflation risk — inflation could eat away at the real value of your future payments.

The Term Premium is the extra yield investors demand above and beyond the expected path of short-term rates to compensate for those risks.

Read that again, slowly.

In other words, investors look at the current rates of shorter term bonds, like the overnight rate (Fed Funds) or maybe the 2-year UST, and then decide what they need as an interest rate (the yield) over and above that shorter term rate to protect themselves in the future.

Why?

Think of it like an insurance premium—a cushion against uncertainty about inflation, growth, Fed policy, and financial market stability.

In a world with no uncertainty, the 10-year Treasury yield would just equal the average of where the market expects short-term interest rates (like the Fed Funds rate) to go over the next 10 years.

But we live in the real world, and so, because risks are real and future outcomes are uncertain, the Term Premium adds a "concern cushion" on top.

In other words:

10-Year Treasury Yield = Expected Path of Short Rates + Term Premium

When Term Premium rises, long-term yields rise too—even if the Fed isn’t moving rates at all.

And when Term Premium falls (like it did during the excessive Quantitative Easing, aka QE, era), long-term yields stay suppressed even as short-term expectations rise.

So, by now you may be asking, how is Term Premium calculated?

Unlike bond yields, which you can simply observe in the market, Term Premium isn't exactly obvious or even visible.

Nope. Just like any good opaque Wall Street measurement, it has to be estimated using models.

And the most widely used is the ACM model, developed by economists Tobias Adrian, Richard Crump, and Emanuel Moench at the New York Fed.

In essence, the ACM model breaks Treasury yields into two parts:

Expected future short-term rates, and

Term Premium (the "leftover" after accounting for expected rates).

Other methods exist, but the idea is the same:

Estimate where the market expects short rates to go, subtract that from observable yields, and what's left over is the Term Premium.

“Term premiums reflect investors' uncertainty about the future and their willingness to bear risk. Changes in the term premium can drive large movements in long-term interest rates, with important implications for financial conditions and the economy.”

— Adrian, Crump, and Moench, Federal Reserve Bank of New York Staff Reports

A couple of keys here:

Term Premium moves based on sentiment, inflation fears, fiscal outlook, monetary policy credibility, and global demand for Treasuries.

It can even go negative (as it did after COVID) when investors are so desperate for safety that they accept yields below expected future short rates.

And when Term Premiums rise rapidly, this is usually attributed to what we call Bond Vigilantes.

The ones demanding higher yields to be compensated for higher risks.

If you are wondering what Bond Vigilantes are and where that term even comes from, I wrote a whole newsletter about them a while back that you can find right here:

Though the article is from a while ago, I highly encourage a read for more context about what is going on today and why Bessent is worried about yields.

And especially Term Premium and where it is now—or at least where it is headed.

🧐 Where is Term Premium Now?

After years of being suppressed by Fed bond-buying (QE) and a flood of global savings, Term Premium is finally reawakening.

In the past year, and especially over the last few months, Term Premium on the 10-year Treasury has climbed sharply—helping drive long-term yields higher, even as expectations for Fed rate cuts remain in place.

In other words, it’s not the Fed pushing yields higher.

It’s bond buyers demanding more protection against the risks they see coming.

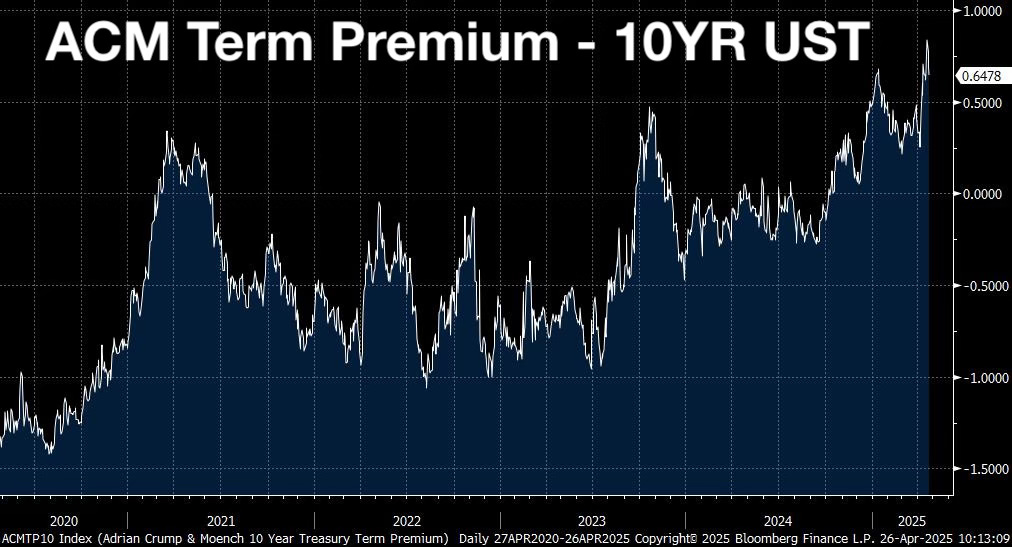

Let’s take a look at where the numbers stand today. Here’s a chart of the 10-year US Treasury Term Premium, as calculated by ACM.

What do we notice?

The 10-year Term Premium has surged to its highest level in over five years — and the momentum is seemingly building.

But before we get too ahead of ourselves here and become outright alarmists, let’s take step back.

Let’s zoom out a bit.

This is important for two reasons: to give context for the current levels and to set the stage for why Bessent is so deeply worried about where we may be headed.

Here is where Term Premiums have been in last 50 years.