💡 Informationist Alpha Newsletter

August, 2024

👊 Hey there Informationist Alpha, this is your monthly macro update. Unpolished and raw, these are the main macro themes and factors I'm taking into account for my own portfolios.

Let's get right to it!

General Economic Indicators

Uncertainty. This is the operative word of the month.

Let’s face it. We’ve had an assassination attempt on a former/current candidate for President. The current President dropped out of the race due to declining cognitive ability. The presumptive/selected Democratic nominee is a person who had <1% of primary votes when she dropped out of the race the first time.

We have accelerating conflict in the Middle East. We have unsettled and continuing conflict in Ukraine.

And that’s just the geo-political side. Add in the economic data we’ve been seeing, and the markets’ reaction has been none other than spooked.

The market hates uncertainty, see here (draw down from recent highs):

So large-cap markets (SPY & NASD) had marched to all-time highs in July, only to turn over and sell off the past few weeks.

We will come back to the dynamics here, but a current theme is that AI-fluff is coming off the top of the market, causing the S&P 500 to drop sharply from the frothy highs.

The Fed doesn’t mind this, of course. In fact, it is almost welcome at this point, to tame the inflation engine of financial assets.

Fed Outlook

If you heard Powell speak this past week, then you know that he primarily seemed comfortable with the current situation. How so?

Well, inflation reading have come down recently, and unemployment (up to the day of the meeting—we will address changes here in a moment) has largely been in check.

And so The Fed slightly red—lined the last press release, with a few key changes.

First, they removed the word ‘modest’ when describing progress on inflation.

Second, they reiterated that they acknowledge progress is being made.

Third, they turned their attention to unemployment, saying they are now ‘attentive to the risks to both sides of [their] dual mandate’

This opened the door to the unemployment factor as a tipping point soon.

Powell in the presser also laid out scenarios that covered everything from several cuts this year to none at all. But I believe this was just talk to keep the market at bay. He needs it to moderate (sell off) a bit. He just doesn’t want a crash.

So, he said, '“If inflation moves down in line with expectations, growth remains reasonably strong, and the labor market remains consistent with its current condition, a rate cut could be on the table in September.”

The market’s reaction?

It immediately priced in 100% probability of a cut in September and 85%+ chance of another cut in December. But then the unemployment figures came out a few days later.

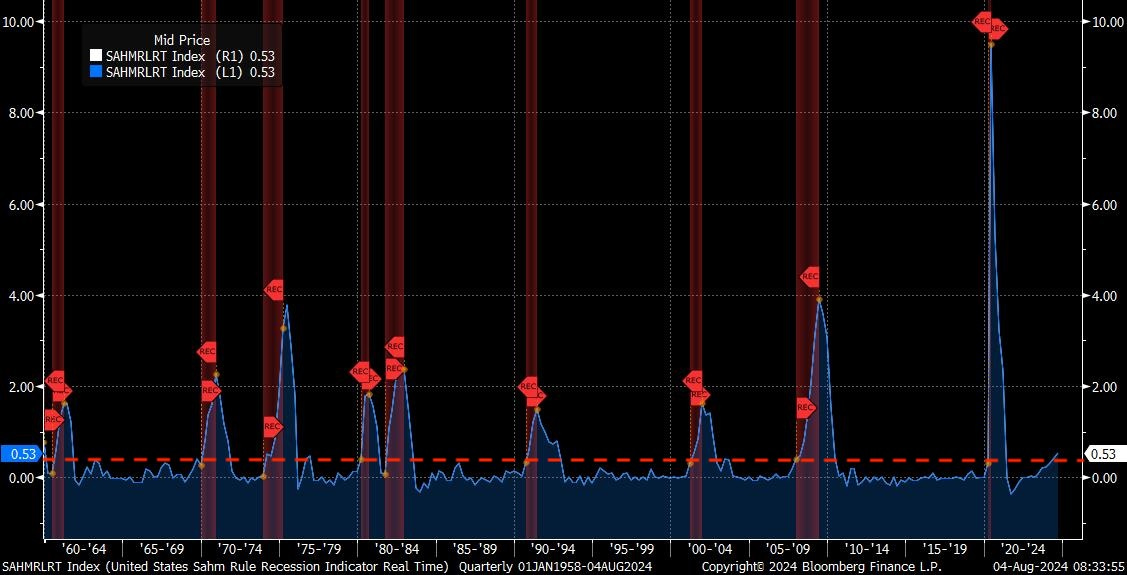

Sahm Rule Triggered

Let’s just say that the report was dismal across the board.

Payrolls lower than expected, unemployment rate higher than expected, and underemployment higher than expected (7.8% vs. last month of 7.4%).

But worst of all, the unemployment rate at 4.3% triggered what is known as the Sahm Rule. Created by Claudia Sahm (A former Fed official), this rule states that when the three month average unemployment rate is more than .5% above the lowest rate in the last year, we have likely entered a recession.

Makes sense, as it means the jobless rate is accelerating higher.

And it has held true for the last umpteenth recessions (red shaded areas):

Once we cross that .5 (red dotted line) threshold, we are already in recession.

And so, the markets reacted as you saw above, with the S&P 500 and NASD both selling off 3.8% and 5.7% in just two days.

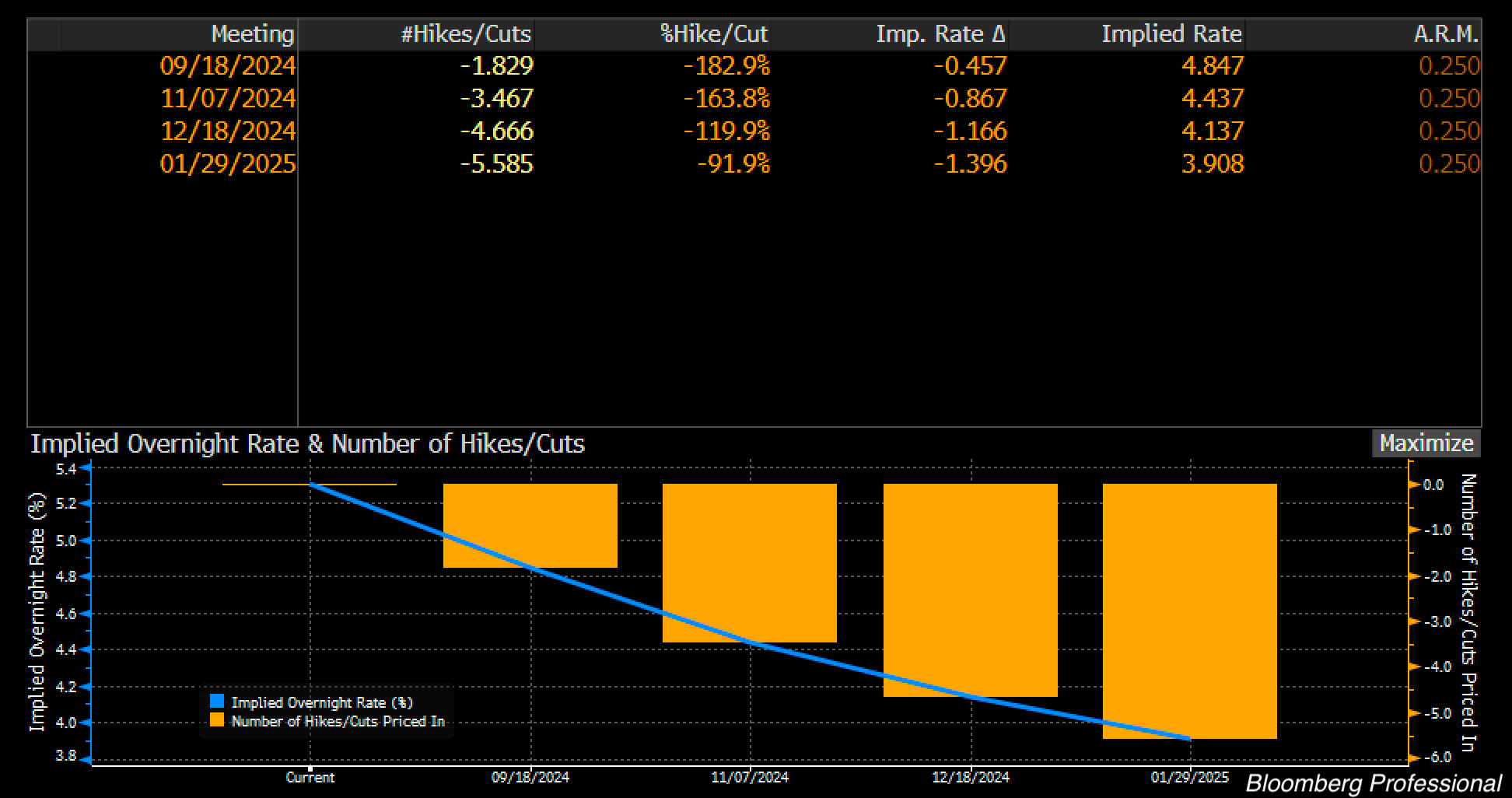

Fed Futures

On top of this, the market has declared that we are going to get not just one, but probably two, rate cuts by September.

This means the market expects the Fed to either lower rates by 50bps in September or maybe even have a mid-meeting cut of 25bps (i.e, sometime this month ahead of the September meeting) and then another 25bp cut in September.

This was also reflected in the Treasury market, as the 2yr UST yield fell to close the gap of the 10Yr UST yield.

Remember, this yield curve has been inverted for two years now.

Inversions signal a pending recession. Un-inverting means we are about to—or have already—entered one.

Meanwhile, we have a situation brewing in Japan.

Japanese Yen Carry Trade

I’ve talked a lot about the Japanese carry trade and its potential impact to the markets. If you haven’t read that and want more, you can find it here:

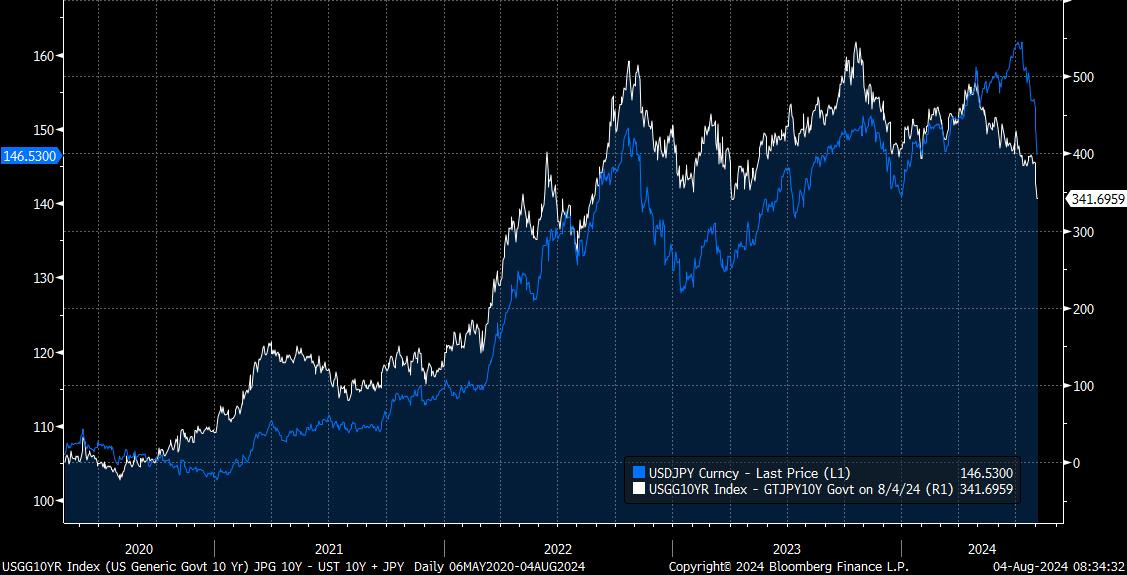

Bottom line, with the BoJ raising interest rates for the first time since 2007, the era of free money from Japan is officially over.

Remember, as i-rates in Japan were being held artificially low, while rates here in the US and in other developed nations were kept high, this created tremendous pressure on the yen.

the BoJ had a choice to make: either keep defending the yen or let rates begin to normalize for their bonds. They chose the latter, raising their target by .25%

The impact for the yen was sharp, as it gravitated back to the normal level of the cash/carry trade versus the UST/JGB 10YR spread:

But there is further to go. Problem is, the ability to borrow money for free (by selling short 0% yielding JGBs and collecting the free yen) is now likely gone.

The result is these trades must be covered (hence the reversion you see above) and this means the selling of risk assets that were bought with this ‘free money’.

The Nikkei (Japanese stocks) felt it like a gut punch on Thur and Fri:

And risk assets across the world are now feeling the crunch.

Trump Trade

Another theme that was hit this past week was the ‘Trump Trade’, where investors, betting on the likelihood of another Trump Presidency, bought stocks that would benefit from his potential policies.

I wrote all about this also, you can find it here, if you haven’t seen it:

Because it was a fast and furious trade, I didn’t try to chase it, personally.

And now, with the Democrats seemingly fully mobilizing behind Kamala Harris as the nominee, she has gained serious momentum, all but stifling this Trump Trade.

You can see how the small caps (Russell 2K) rallied hard after the assassination attempt and have since retreated with the massive news media push of Kamala as a worthy opponent. 🙄 Our politics are a mess. There, I said it.

Bottom Line

I feel this is not the time to ‘get cute’, as we say on Wall Street.

Markets like this are easily spooked with so much uncertainty swirling around, especially as we appear to be grinding right into a recession.

I am pleased that my portfolios have been positioned with a solid balance of high-yielding cash (T-Bills), commodities and hard money (Gold, Silver, Bitcoin) and some deliberate allocations to risk equities.

Note re: the rate talk: while the TLT and long-term bonds could be a trade in here, as long-term yields fall, I just don’t want to hold paper that will ultimately give me a negative yield, in the long run.

As far as I can see it, there are two ways this can go: the market grinds lower for a few months here, sells off, and The Fed has to eventually step in, cut rates, calm the market, and reverse QT back into QE.

This could produce some opportunities in assets like large-cap stocks and Bitcoin, which is why I am happy to have the cash ballast, ready for re-allocation. And you should, too, IMO.

This scenario would actually be welcome from The Fed, IMO, as it would help drive inflation lower through the highly financially leveraged economy we have in the US.

This would allow them to stair-step rates lower and declare victory this fall.

However. The danger here is the ‘all assets correlate to one’ reaction of the market.

This could be tipped of by any or series of event(s).

All-out war seems more likely every day. Another assassination attempt? Maybe something more sinister, who knows?

We do know one thing, though.

The Fed and Treasury cannot have an all-out crash in risk assets without negatively affecting the Treasury market. This is simply not possible now.

And so, we would see an immediate and overwhelming response, much like March/April of 2020 (except larger), where The Fed steps in and splashes liquidity into the markets, once again.

Because of this belief and what I consider to be the harsh reality of the Treasury’s predicament, I continue to remain widely diversified in asset class exposures.

But this is one of those rare instances that I am adjusting a few select risk exposures.

I am mainly removing a lot of exposure from equity risk and re—allocating to high-yielding cash and gold, due to heightened geo-political and domestic political tensions. This is highest allocation I have ever personally had in gold, and this is because I believe it will act as a safe-haven for heightened tension and conflict.

Please note these changes in the portfolio spreadsheets.

*Note: I also have a high degree of confidence in Bitcoin, as many of you know. But this would only be a safe-haven at this point under extremely selective cases (bank and global financial failures, threatening access to money, i.e.), otherwise it must be treated as a long-term holding only (or a risk asset if you are trading actively).

That said, I am ready to use cash to re-allocate to Bitcoin on strong pullbacks into the mid to low 50K area, and would re-allocate to a much larger position with a pullback into the 40’s. FYI. This is a long-term holding for me, I have not sold any to this point.

->> LINK TO PORTFOLIOS <<-

And finally, I had a comprehensive discussion with Michelle Makori at Kitco last week. If you want to hear my thoughts re: the above macro environment and factors verbally, you can find that here:

That's it.

If you have questions or ideas, you can find me in the Informationist Alpha community!

Talk soon,

James✌️