💡 How Warsh Plans to Beat Inflation Without Beating It

He played the hawk in Portugal this week. Underneath the tough talk, he was quietly building the case to cut rates and change the very ruler we use to measure inflation.

✌️ Welcome to The Informationist, the newsletter that makes you smarter about money in just a few minutes each week.

🙌 One topic. Exposed and explained so you can make better decisions with your money. Like a simple walk down Wall Street.

🫶 If this was forwarded to you, you have awesome friends. Join 45,000+ readers here.

Today’s Bullets:

🦅 The Hawk on the Sintra Stage

🕊️ The Dove Hiding Underneath

🧮 The Ruler Warsh Wants to Swap

🪤 The Trap in Changing the Measure

💰 What a Stealth Dove Means for Your Money

Inspirational Tweet:

Look closely at the highlighted text from today’s Inspirational Tweet, because it appears that Warsh just told on himself.

Reporters have been grumbling that the brand-new Fed Chairman won’t say where rates are headed. So he points them straight at the bond market. Volatility down. Yields down. Inflation expectations down.

Then the wink: the people wagering real money “understand quite well.”

This is the same man who spent the prior week sounding like the fiercest inflation hawk in a generation.

And look at the tone he lands on. Not worried in the slightest.

He calls it a “rare moment” to go back to first principles and rethink what the Fed is doing, and says he is encouraged. Keep that phrase in your back pocket. First principles is where the ruler we use to measure inflation comes back into play.

So which is it? Hawk, or something else entirely?

Picture the scene in Sintra.

Kevin Warsh, barely six weeks into the biggest job in global finance, sits down on a stage in Portugal next to Christine Lagarde and two other central bankers (we won’t waste a single breath on them here, don’t worry), and spends the afternoon talking like the toughest hawk in the building. Prices are too high. The Fed will deliver price stability.

Anyone waiting for him to go soft would be, in his own word, disappointed. The headlines wrote themselves. Hawk. Done.

But the tough talk on top and the bond-market wink underneath contradict one another. One says the fight is just beginning. The other says the fight is nearly over and the market has already figured it out.

Yet both came from the same man, on the same stage, in the same week.

And so, what Warsh built in Portugal is a setup to declare the inflation war won, start cutting rates, and never once admit to going dovish to get there. And there is a single technical lever, buried in how we measure inflation itself, that makes the whole thing work.

So what’s he going to do? How is he going to do it, and perhaps most importantly, how is he going to justify it?

All good and super important questions for any investor, and ones we are going to answer, nice and easy as always, right here today.

So, pour yourself a big cup of coffee, and settle into your favorite seat, for a look at the dove hiding inside Kevin Warsh’s hawk, with this Sunday’s Informationist.

Partner spot

You've spent years thinking about what happens to the dollar. Have you spent any time on what happens to your bitcoin after you are gone?

Most bitcoin holders think they have an inheritance plan, but they don't.

Knowing where your keys are isn't a plan. Neither is telling your spouse the seed phrase. And the will your attorney drafted years ago might not account for any of it. Bitcoin inheritance isn't just a technical problem, but a legal one too. Your heirs need both the keys and the legal authority to actually use them.

There's a quick way to find out how exposed you actually are. Get your free bitcoin inheritance readiness score in under 2 minutes.

🦅 The Hawk on the Sintra Stage

Let’s start with what Warsh actually did in Portugal, because on the surface it was a clinic in sounding tough.

As we explored last Sunday in How to Read a Fed That Stopped Talking, Warsh spent his first weeks running the Fed doing an impression of the most hawkish chairman in years.

He held rates at a target range of 3.50% to 3.75%.

He gutted the policy statement down to a skeletal 130 words.

He refused to pencil in his own dot on the dot plot.

And he told the country the Fed would deliver price stability, in his words “strong, unanimous, and unambiguous.”

Then he flew to Portugal and did it again, louder.

Every summer, the European Central Bank gathers the heads of the world’s major central banks in the hill town of Sintra to sit on panels and talk shop. Think Davos, but for the people who actually set your interest rates.

This year the guest of honor was the new American, and the room wanted an answer to one question.

Is Kevin Warsh a hawk or a dove?

He gave them the hawk.

Prices are still too high, he said. The Fed is going to deliver price stability in the US, and that is that.

And when the conversation drifted toward the idea that maybe the Fed could learn to live with inflation running a little hot, a little above its sacred 2% target, Warsh shut the door on it. Anyone counting on that, he said, would be disappointed.

Wall Street took him at his word.

In the days after his first official Fed meeting in June, traders piled into the bet that the Fed’s next move would be a rate hike, not a cut.

Fed funds futures, the contracts where the smart money wagers on where rates are headed, tilted toward an increase as soon as this summer, and the odds of a hike by the fall jumped sharply.

For a country that has spent two years waiting on cheaper mortgages and cheaper car loans, that was a splash of ice water.

And that silence carries a cost.

As we explored last Sunday, Warsh has pulled out the Fed’s old shock absorbers. No forward guidance, a bare statement, a buried dot plot.

Unfortunately, when the Chairman goes quiet and hawkish at the same time, the market is left to guess. And guessing shows up in our mortgage rates, our car loans, and everything else keyed to the US bond market.

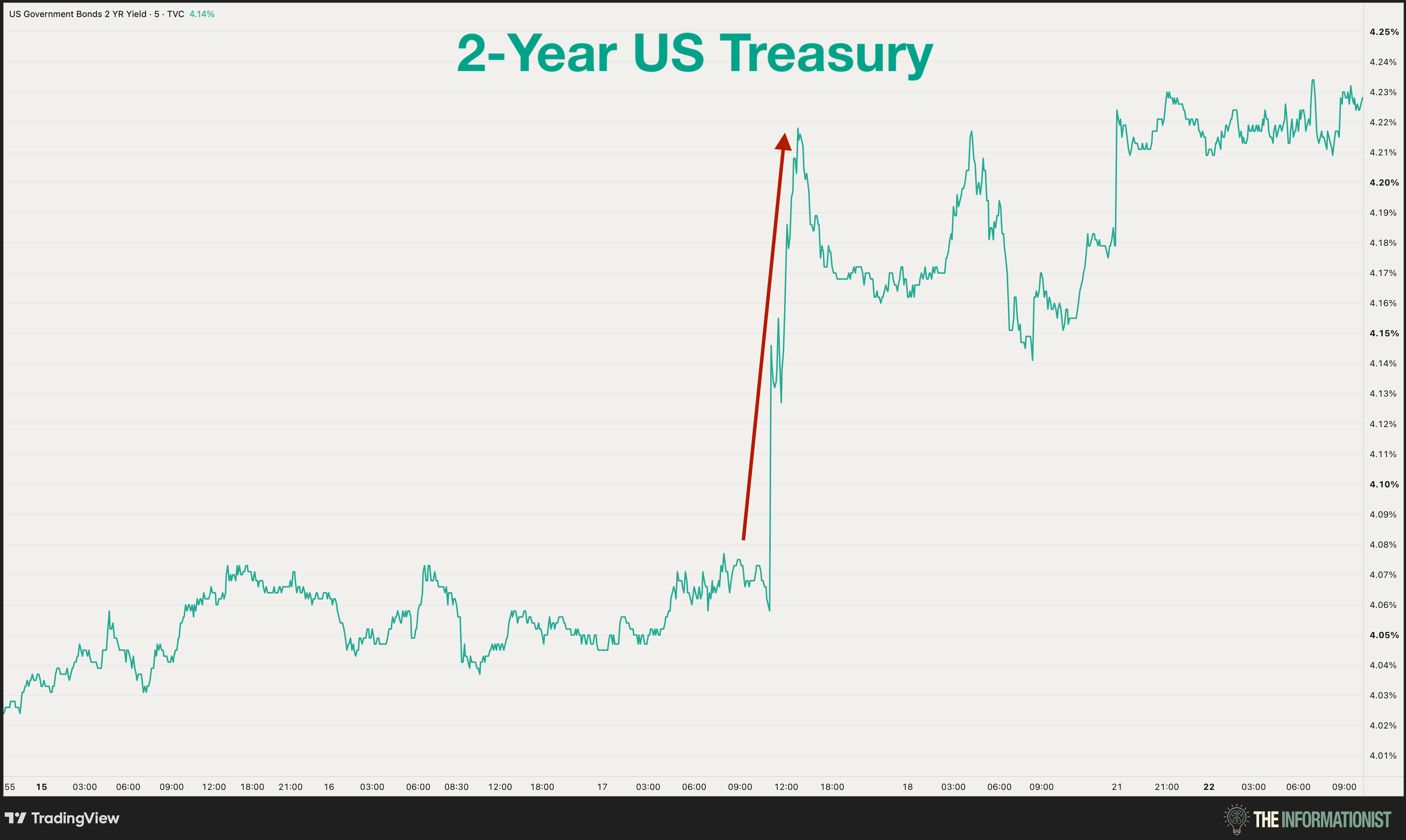

We got a live demonstration on his very first day, when a routine decision to hold rates jolted the two-year Treasury yield 16 basis points higher in a single afternoon, purely because Warsh would not tip his hand.

So the story writes itself, right? Tough new sheriff, inflation in the crosshairs, hikes back on the table, cheap money cancelled.

Hawk. Done.

But that was only the performance the room was meant to see.

Because in that same trip, on that same stage, Warsh did something no true hawk would do.

He turned and pointed at the bond market as proof the inflation fight was already winding down. He talked, almost cheerfully, about going back to “first principles.” And for a man supposedly at war with rising prices, he sounded strangely, conspicuously relaxed.

Which leaves the question this whole letter is going to answer.

If Warsh is really the hawk he played in Portugal, why did he spend the same trip quietly laying out every reason the Fed is about to be done?

And what is the single lever he is already reaching for that lets him declare the war won without firing one more shot?