💡 How to Read a Fed That Stopped Talking

Warsh killed forward guidance, pulled his own dot, and launched five task forces. The Fed stopped narrating itself. You can still read what it does.

✌️ Welcome to The Informationist, the newsletter that makes you smarter about money in just a few minutes each week.

🙌 One topic. Exposed and explained so you can make better decisions with your money. Like a simple walk down Wall Street.

🫶 If this was forwarded to you, you have awesome friends. Join 45,000+ readers here.

Today’s Bullets:

🤫 What Warsh Just Deleted

🔵 The Dot Plot Problem

🛠️ The Five Task Forces

🏦 The Balance Sheet Tell All

💰 What a Silent Fed Means for Your Money

Inspirational Tweet:

Wait, what?

The Fed isn’t going to give us guidance anymore? No clues to what they are thinking about rates and action in the future?

The new Chairman made it abundantly clear in his first presser.

The Fed, the institution that has spent the last two decades explaining itself in exhausting detail, will stop guiding us now.

Leaving us to wonder whether our mortgages get cheaper. Whether our savings finally earn something. Whether the market we are all counting on for retirement keeps climbing or rolls over.

For years we have had an important place to look for the answers. Eight times a year, the Fed laid out its plan, drew us a map of where rates were headed, and put a chairman in front of the cameras to walk us through it.

But Kevin Warsh just took the map away.

He scrapped the guidance that told us what comes next. And he made clear there is far more of this coming, meaning far less communication from him and the Fed.

So what are we supposed to do now? How do we know where our money is headed when the Fed stops telling us? How can we make decisions about our own investments if we don’t have at least the Fed’s guidance as an anchor for how they are thinking about and addressing inflation and other market matters?

Good questions, serious ones that can make a big difference in how we approach our own finances. Our own investments.

But have no fear, because we will answer all of them and more, nice and easy as always, here today.

So, pour yourself a big cup of coffee, and settle into your favorite seat for a look at how to read a Fed that just went silent with this Sunday’s Informationist.

Partner spot

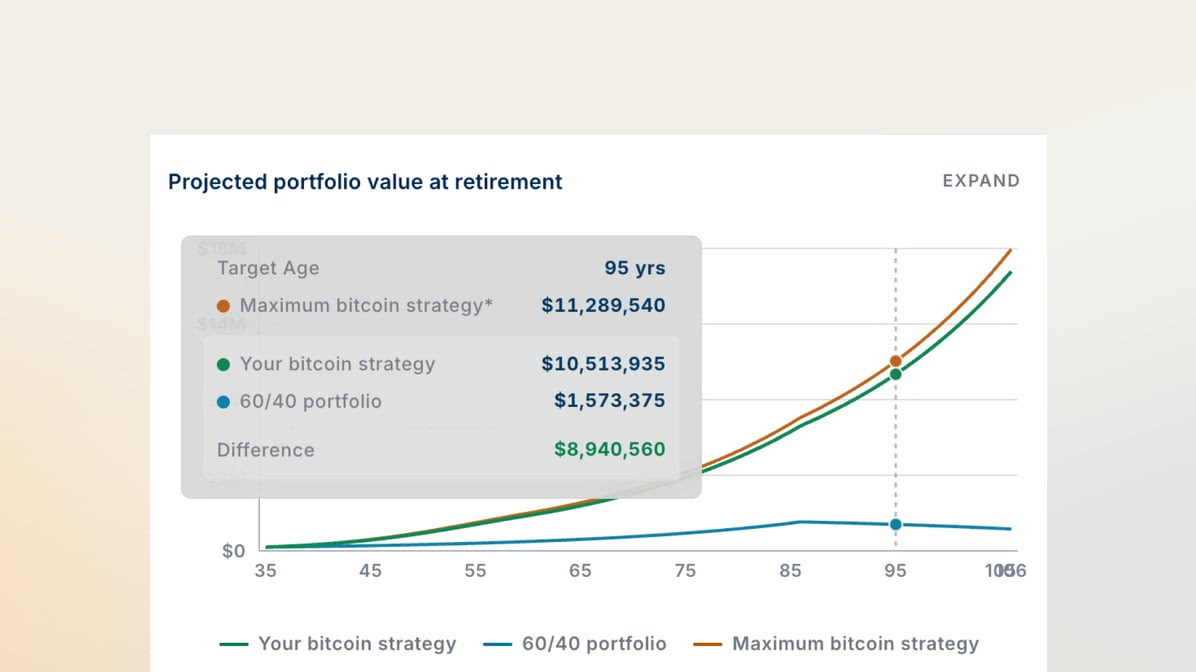

Most people know how much money they want in retirement. Few know how much bitcoin it could take to get there.

In a free one-on-one session, an Unchained specialist will walk through your numbers using our proprietary retirement calculator and model multiple outcomes based on your goals and timeline.

You'll leave with a personalized retirement projection you can revisit anytime and use to make more informed decisions about your future.

Availability is limited to ensure each session receives dedicated attention.

🤫 What Warsh Just Deleted

First, let’s talk about the term “forward guidance,” because it’s a concept that Wall Street has become somewhat addicted to in recent years.

In short, forward guidance is the Fed telling us, on purpose, what it expects to do next.

Not the rate it sets today, but the signal about tomorrow. And when the Fed wants to steer us, it says so out loud, and it gets specific.

For instance, in August 2011, with rates already pinned near zero, the Fed told us it expected to keep them “exceptionally low at least through mid-2013.” A promise nearly two years out. When that was not enough, it stretched the date to late 2014, then to mid-2015.

And in June 2020, in the teeth of lockdowns, Jerome Powell said it in plain English: the Fed was “not even thinking about thinking about raising rates.” Once again, reaching into the future and setting our expectations on purpose.

Now, the reason those words land on us has almost nothing to do with the rate the Fed sets that day. The Fed sets one rate, the overnight rate banks charge each other. By itself, that rate does not price our mortgage.

What prices our mortgage, our car loan, the cost of borrowing money for years at a time, is the 10-year Treasury yield. And the 10-year is built from three things stacked together:

Where the Fed has rates right now,

where the Fed signals they are going next along with its own read on inflation,

and what the market itself expects inflation to do.

Forward guidance is the Fed leaning hard on that middle piece.

Shift the expectation, and the 10-year moves. Move the 10-year, and mortgage rates, auto loans, and the cost of long-term borrowing move right along with it, before the Fed has touched its actual rate at all.

Go back to that August 2011 promise. The Fed did not cut a thing. It simply told us rates would stay low for two more years, and Treasury yields dropped as if the Fed had cut by the better part of a full percentage point. Borrowing costs eased right behind them.

The words did the work of a rate cut.

That is the addiction. When the Fed guides, our financial lives move. It has conditioned the market to pay attention to Fed communications almost religiously.

The Fed has shown us their hand in three main ways.

The statement. Eight times a year, the Fed puts out a short written statement after its meeting. The clues live deep in the words, the choice of words, the absence of them, and especially the elimination of them. These clues can often tell us if the Fed is leaning toward cutting, hiking, or holding. And especially whether they are adding liquidity to markets or taking it away.

The dot plot. You’ve likely seen this plot before. I’ve talked about them extensively. Four times a year, every official anonymously marks where they think rates are headed over the next few years. (Hold that thought. This one has a checkered history we will get into.)

The press conference. After the meeting, the Chairman stands before the cameras, explains the Committee’s thinking, and takes our questions from reporters in the room.

That is the main instrument panel. For years, that is how we read the Fed.

This past week, Warsh went after all three.

Start with the statement.

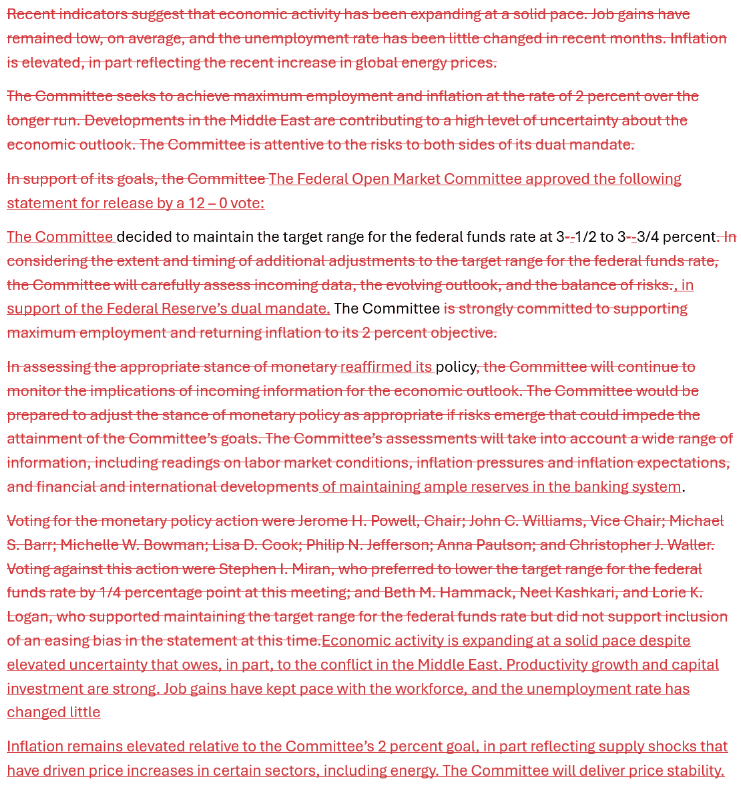

Powell’s final statement in April ran 341 words. Warsh took it all the way down to a mere 130 words.

I mean, look at this red-ink bloodbath.

Look at what Warsh cut.

The whole passage about how the Committee “will carefully assess incoming data, the evolving outlook, and the balance of risks,” the careful language that always hinted at what came next, deleted. In its place sit a few plain sentences about the economy and one flat promise: the Fed will deliver price stability.

That’s it. A few facts and a pledge. No roadmap whatsoever.

Then the dots.

The other eighteen officials submitted theirs. Warsh refused to submit his own. The one person whose view moves markets more than anyone else’s left his blank. (We will get into exactly why that is such a loaded move in a moment.)

And the podium. In his first press conference, Warsh leaned on a line from his old mentor, former Secretary of State George Shultz: a press conference is only worth holding when you actually have something important to say.

Translation for the rest of us: do not expect to hear from this Chairman often.

So in a single afternoon, the new Fed took a chainsaw to all three communication channels. The statement, the dot, the podium.

Quieter on every one.

The question is why. And the answer starts with the one piece of the old system that has embarrassed the Fed the most.