💡 Why the Treasury's Nightmare May Soon Be Yours

Issue 211

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🫶 If this email was forwarded to you, then you have awesome friends, click below to join!

👉 And you can always check out the archives to read more of The Informationist.

Today’s Bullets:

📉 The Reversal

🔢 The Loop

🏛️ The One Outcome

💰 What It Means for Your Money

Inspirational Tweet:

If you’ve been watching the bond market recently, you’ve noticed something has shifted. Something that makes an already dangerous situation dramatically worse for the Treasury, for the Fed, and ultimately for you and your money.

As I implied above, the surprising rise in the expected Fed Funds rate sets up the story, but it leads to a host of questions.

Like, What happens to the Treasury when rates suddenly start going the wrong direction? What are they forced to do about it? And how does it end up affecting you?

All critical questions. And ones that all lead to one place. One outcome.

Today, we are going to pull back the curtain on what’s really happening with the US Treasury right now, why the situation just became significantly more dangerous, and where it’s all heading.

But don’t worry, we will do it nice and easy, as always.

So pour yourself a big cup of coffee and settle into your favorite seat as we explore the US Treasury’s growing nightmare with this Sunday’s Informationist.

Partner spot

The Downturn Advantage

Bitcoin’s volatility is its advantage. For long-term investors, volatility creates opportunities to build and refine positions over time. Mark Moss recently joined Unchained to explore how bitcoin fits into long-term strategy, and how downturns can be used to position more effectively.

The discussion covers:

How bitcoin’s volatility can support long-term accumulation

Why the current environment is putting pressure on traditional approaches

How to think about downturns as opportunities for more intentional positioning

Download the recent collaborative report from Mark Moss and Unchained, Retire Off Bitcoin: The Freedom Investor’s Guide, to access both the report and the full event replay.

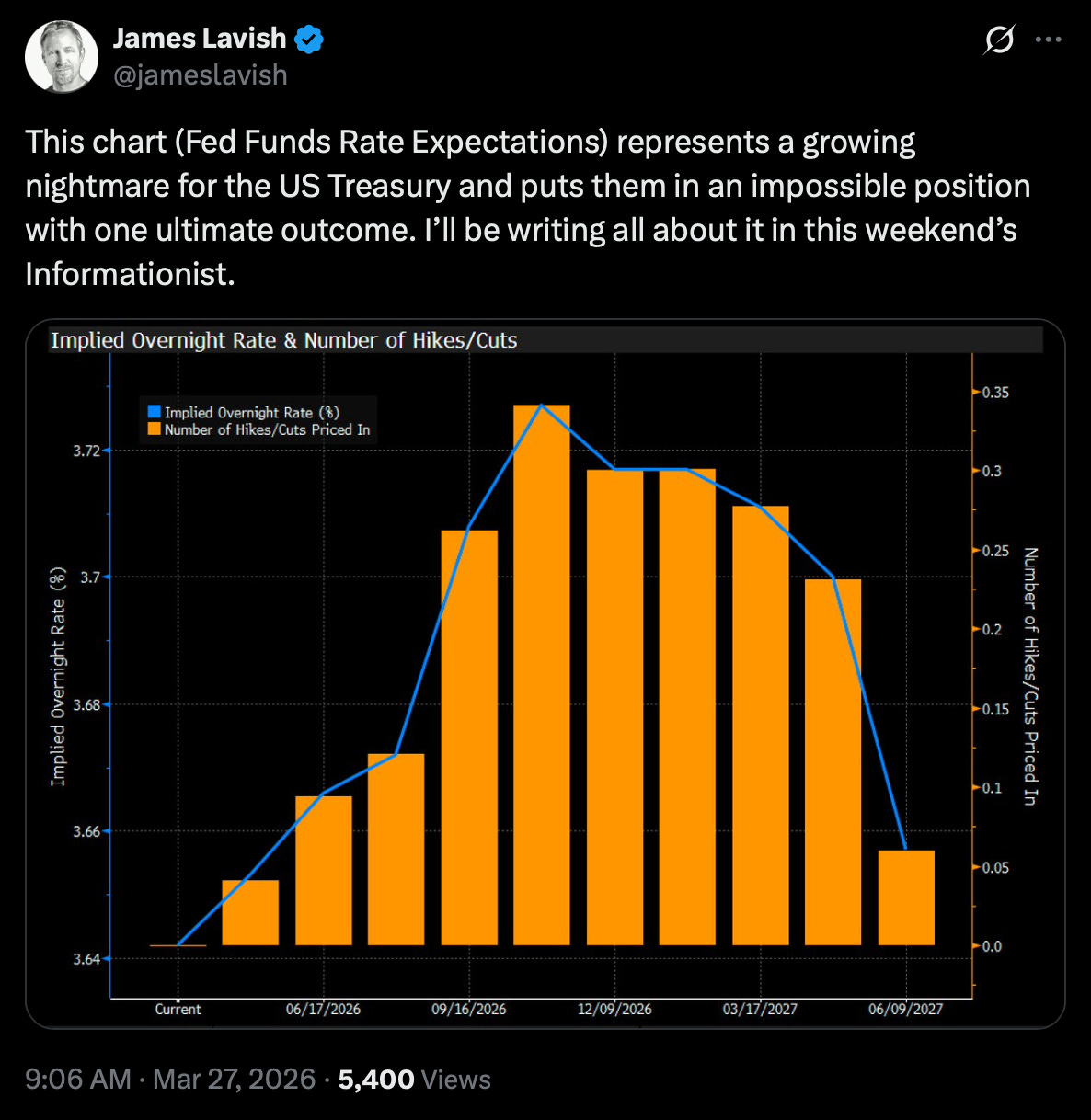

📉 The Reversal

First things first. That chart in my X post above? The one showing where investors expected the Fed Funds Rate to move in the near and longer term?

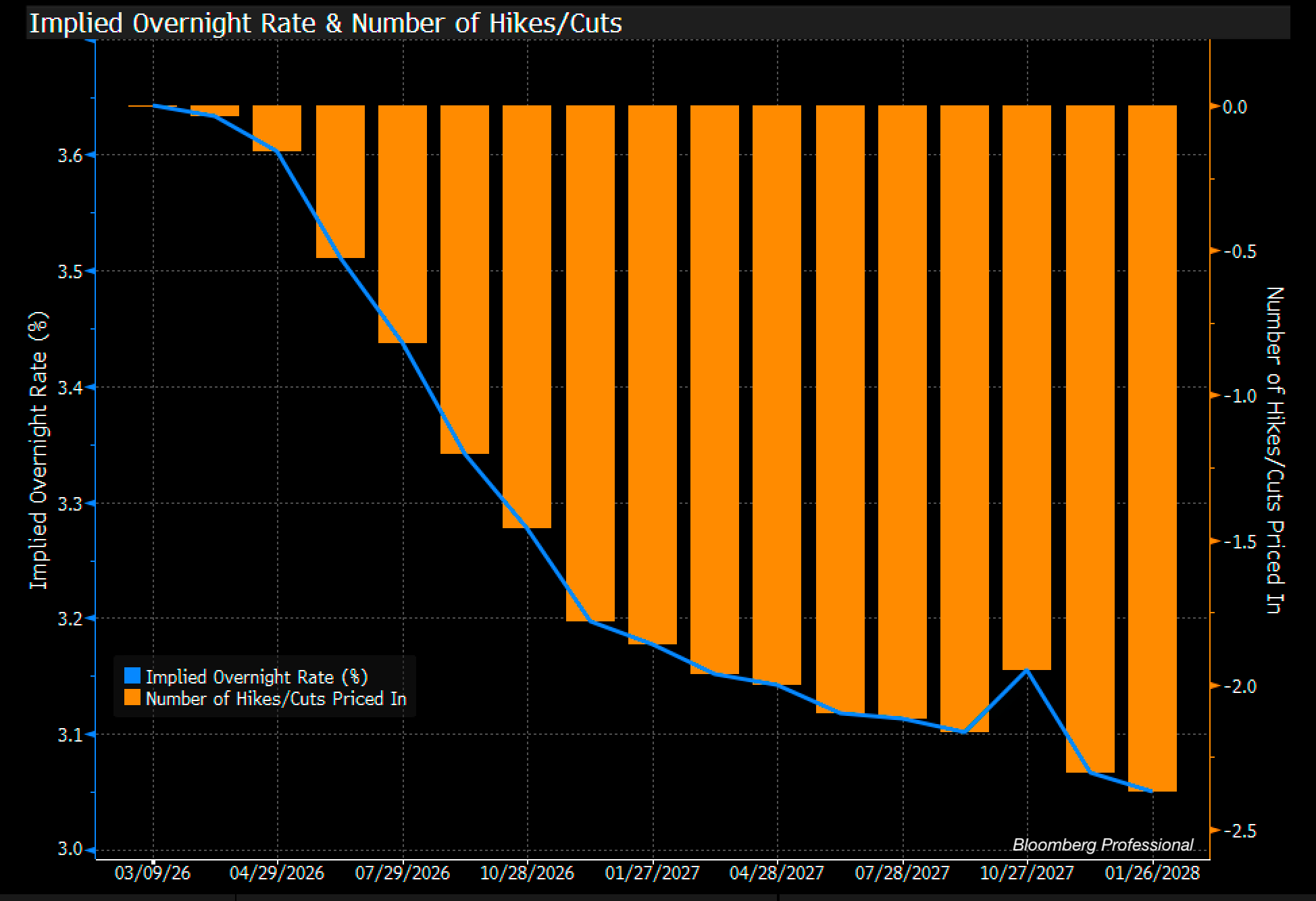

This is what it looked like just two weeks ago.

What do we see?

More than two rate cuts were expected by early 2027 (right side of chart). The implied overnight rate falling steadily from 3.65% down to just above 3% (left side).

For anyone who needs to borrow money, this was great news. Lower rates ahead. Cheaper financing on the way.

And nobody on the planet needs to borrow more money than the US Treasury.

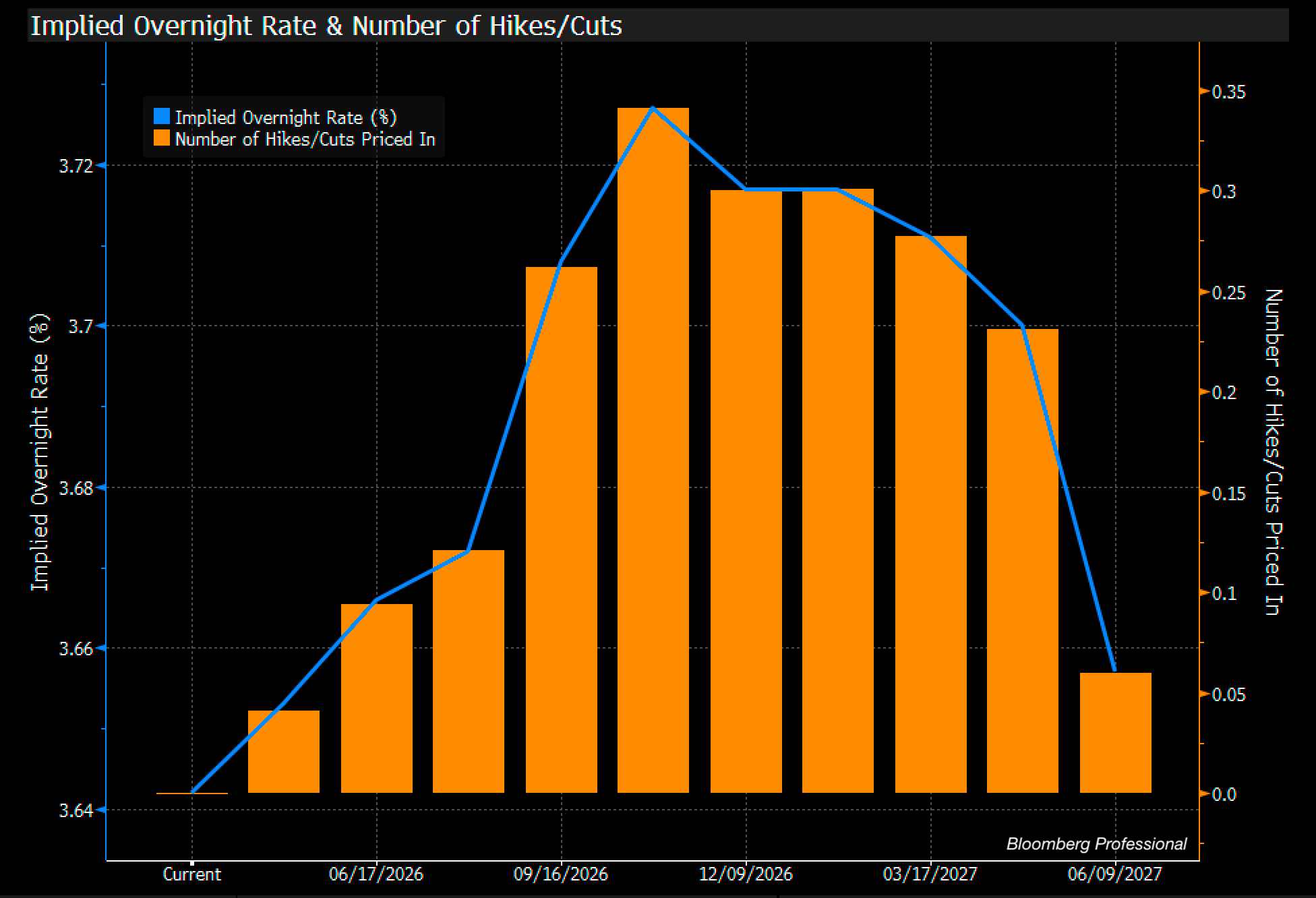

Now look at the one from my post again:

Same chart. Two weeks later. The cuts have vanished. And in their place, the market is pricing in a hike.

If you caught last week’s issue, you know what triggered this. Iran. Oil spiking over $100, causing inflation to reaccelerate. A Fed that can’t cut. And a bond market that now thinks they may have to hike.

If you’re the Treasury Secretary reading these headlines, seeing these developments, you feel sick.

To understand why, we need to go back a few years. Because this crisis didn’t start last week. It started with a decision.

An astonishingly poor one.

By none other than former US Treasury Secretary Janet Yellen.

See, when Yellen became Treasury Secretary in 2021, she helped facilitate trillions of dollars being printed during COVID. Stimulus checks, PPP loans, direct payments. The printing press was running full speed.

She also had something no Treasury Secretary is likely to see again.

Interest rates at historic lows. The 10-year yielding barely 1%. The 30-year at 1.80%.

She had a once-in-a-generation window to term out the debt. (Translated: issue longer dated debt, like 7 or 10 or even 30-year Treasuries) Lock in those rates for decades.

She didn’t do it.

Instead, she kept borrowing short. Bills and notes that mature in months, not decades. Instruments that roll over constantly and refinance at whatever rate the market happens to be charging at that moment.

When rates are falling, that works fine. You keep getting cheaper deals.

When rates are rising, it’s a disaster.

Now, I know what you’re thinking. How was she supposed to know? How could anyone have predicted rates would go up so much? Should she have somehow anticipated this?

The answer is Yes.

Janet Yellen had been the Chair of the Federal Reserve. She sat in that seat and understood, better than almost anyone alive, what that kind of money creation does to inflation. She knew the risks. She saw them coming.

And she ignored them. Leaving the problem for the next Treasury Secretary to deal with.

Enter Scott Bessent.

Bessent took the job in January 2025. He had publicly voiced similar concerns about Yellen. But he also believed rates would continue to come back down, and that he could gradually shift toward longer maturities and stabilize things.

But then Powell stopped cutting.

Iran happened. Oil spiked. And inflation expectations reversed.

And those two charts above? That’s Bessent’s plan falling apart in real time. The rate relief he was counting on isn’t coming. It’s going the other way.

To be honest, I’d be surprised if he doesn’t just quit at this point, but let’s assume he doesn’t. Let’s assume he stays and does whatever he can to remedy the situation.

Then we have to ask, how bad is it, exactly? How much does the government actually need to borrow at these rates? And where does it all lead?

The answer is what makes this personal. For every one of us.