💡When There's No Safe Haven

Issue 208

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🫶 If this email was forwarded to you, then you have awesome friends, click below to join!

👉 And you can always check out the archives to read more of The Informationist.

Today’s Bullets:

The Phone Call

The Plumbing

The Pattern

The Playbook

Inspirational Tweet:

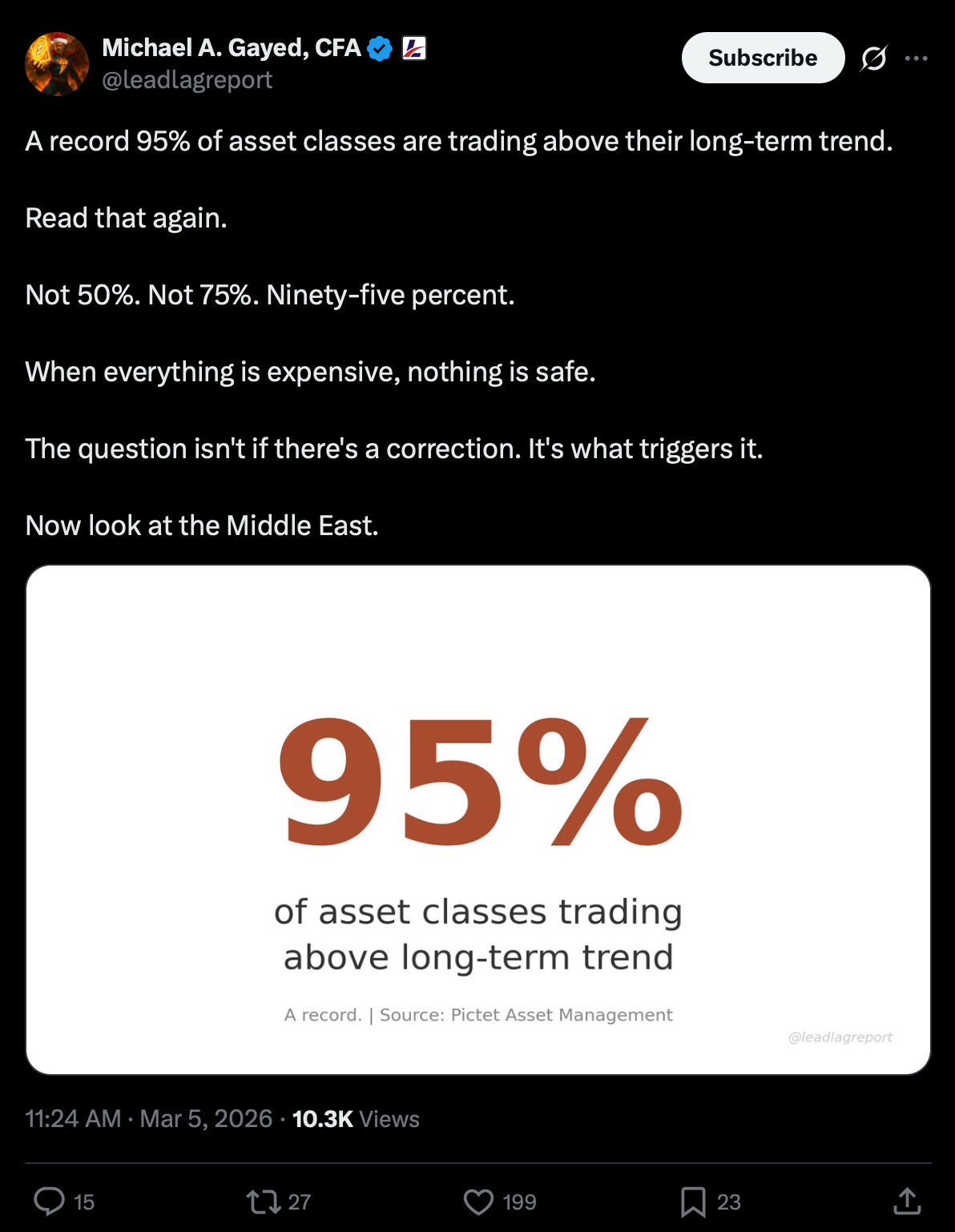

Let’s be honest. This tweet from Michael Gayed deserved a lot more than 10,000 views last week. Buried in a feed full of crude oil price and war-driven inflation worries, it was largely overlooked.

But that other number is the one that stopped me cold.

95%.

That’s how many asset classes are currently trading above their long-term trend. Not 50%. Not 75%. Ninety-five percent. A record.

Think about that. If you own stocks, bonds, real estate, commodities, or crypto, odds are you’re sitting on positions that are all above trend. At the same time.

So what happens when something breaks and everything expensive starts selling at once? Does your diversified portfolio actually protect you? What’s the recovery playbook?

All good questions, and ones we will answer, nice and easy as always, here today.

So, pour yourself a big cup of coffee and settle into your favorite seat for a deep look at what happens when there’s no safe haven, with this Sunday’s Informationist.

Partner spot.

Most People Will Waste This Cycle

Bitcoin bear markets test your wits—and create opportunity for those prepared to act. Our new field guide, 21 Moves to Make in the Downturn, walks you through a clear, practical plan to steady your thinking, accumulate with discipline, and strengthen your long-term position while others lose focus.

Inside, you’ll learn:

How to orient your thinking around bitcoin’s long-term properties

Common psychological traps to avoid during market downturns

Practical accumulation strategies like dollar-cost averaging

Ways to optimize savings, retirement accounts, and idle capital

A small minority will quietly make the moves that matter. We wrote 21 Moves to Make in the Downturn for that minority. If you’re serious about building a position that survives the next decade, start here.

☎️ The Phone Call

March 16, 2020.

I’m sitting at my desk, coffee barely touched, scanning the pre-market numbers. Futures are limit down. Again. The S&P has already lost 20% in three weeks and the bleeding won’t stop.

Then the email hits.

Our prime broker’s normal morning operational summary lands in my inbox. But today, the subject line is anything but normal.

“Immediate Margin Call Required.”

All in red.

I open it. Scan the margin summary first. Then the details.

My stomach drops.

A little background. Most individual investors use something called Reg T margin. It’s simple. Your broker lets you borrow roughly half the value of your stocks. You put up $100,000, you can buy $200,000 worth. 2-to-1.

Hedge funds play a different game. We use something called portfolio margining.

Instead of a flat 2-to-1 rule, the broker looks at your entire book as one unit and assigns each position a haircut.

Here’s how it works.

A haircut is how much value the broker shaves off when calculating what you can borrow against. Blue chips in calm markets might get a 5% haircut. So if you own $100,000 of Apple stock, you need at least $5,000 of capital in your account against that position.

Small number. Easy to cover.

Riskier stocks get bigger haircuts. But when the whole portfolio is diversified, the math works in your favor. Instead of 2-to-1 leverage, you might get 5, 10 or even 20-to-1. Put up $100 million, control over a billion in positions.

Without derivatives.

And if you have not worked in a hedge fund before, here is an important detail for you.

All of those haircuts are set by a black box that sits on the prime broker’s risk desk. Not yours. Theirs. They decide, day to day and sometimes minute to minute, how your portfolio can be margined. How much you can borrow. How much collateral you need.

And you agreed to it. Every hedge fund signs a portfolio margining agreement with their prime broker. You’re playing in their house, by their rules. Rules they can change whenever they want.

When markets are calm, this works beautifully. The portfolio manager diversifies strategically, the black box sees low risk. The book gets small haircuts. Everyone’s happy.

Until they aren’t.

Because when volatility spikes, that black box recalculates. And when it recalculates, the prime broker doesn’t call to discuss it. They send you a notice.

That’s what I was staring at.

Virtually every micro-cap position in the fund had been raised to a 100% haircut. Overnight. Zero borrowing value. Those positions were now dead weight on the books.

Regardless of how much confidence we had in them as companies, as far as the prime broker was concerned, they were dead weight.

Even our best investments, the blue chip holdings in the eyes of the prime broker, you know, big S&P Mag 7 type stocks, had been raised from 5 or 6% to 25 or 30%. Overnight.

One email. Every position. The entire margin structure of our fund had just been rewritten while we slept.

And then you do the math in your head. You realize the cascade. Because it’s not just one position that’s underwater. It’s the whole book. Every holding now requires more collateral than it did yesterday. Collateral you don’t have.

I pick up the phone and call the portfolio manager. Our chief investment officer.

Possibly the worst phone call I’ve ever had to make in my career.

This is where the hedge fund manager bypasses the portfolio managers and heads straight to the traders, telling them to sell. Ten percent. Twenty percent. Of everything. He doesn’t care what it is.

“We need liquidity. We need it now.”

The good positions. The bad positions. The hedges that were working perfectly. Didn’t matter.

In these moments, you sell what you can, not what you want to.

That’s what a correlation-to-1 event feels like from the inside. Like sprinting through a fire, every asset in your portfolio burning right alongside you.

And yes, that means Treasuries too. All of it fair game. Everything on the cutting table.

Because you just need one thing.

Cash.

Suddenly, a whole lot of it.

That was March 2020.

Fast forward to today.

A record 95% of asset classes are trading above their long-term trend. And margin debt just hit an all-time high of $1.28 trillion.

The conditions are lining up again.

So how does this actually happen? What breaks inside the plumbing that turns a normal selloff into a cascade where everything goes down together? Is there a pattern to the recovery? And what can you actually do to protect yourself before the next phone call comes?

Let’s get into it.