💡 What If The Fed Raises Rates?

Why a Fed rate hike no longer does what most people think it does.

✌️ Welcome to The Informationist, the newsletter that makes you smarter about money in just a few minutes each week.

🙌 One topic. Exposed and explained so you can make better decisions with your money. Like a simple walk down Wall Street.

🫶 If this was forwarded to you, you have awesome friends. Join 45,000+ readers here.

Today’s Bullets:

🦅 What Warsh Just Walked Into

💥 The September Paradox: When the Fed’s Lever Broke

🚪 The Trap Doors Beneath His Feet

💰 What It Means for Your Money

Inspirational Tweet(s):

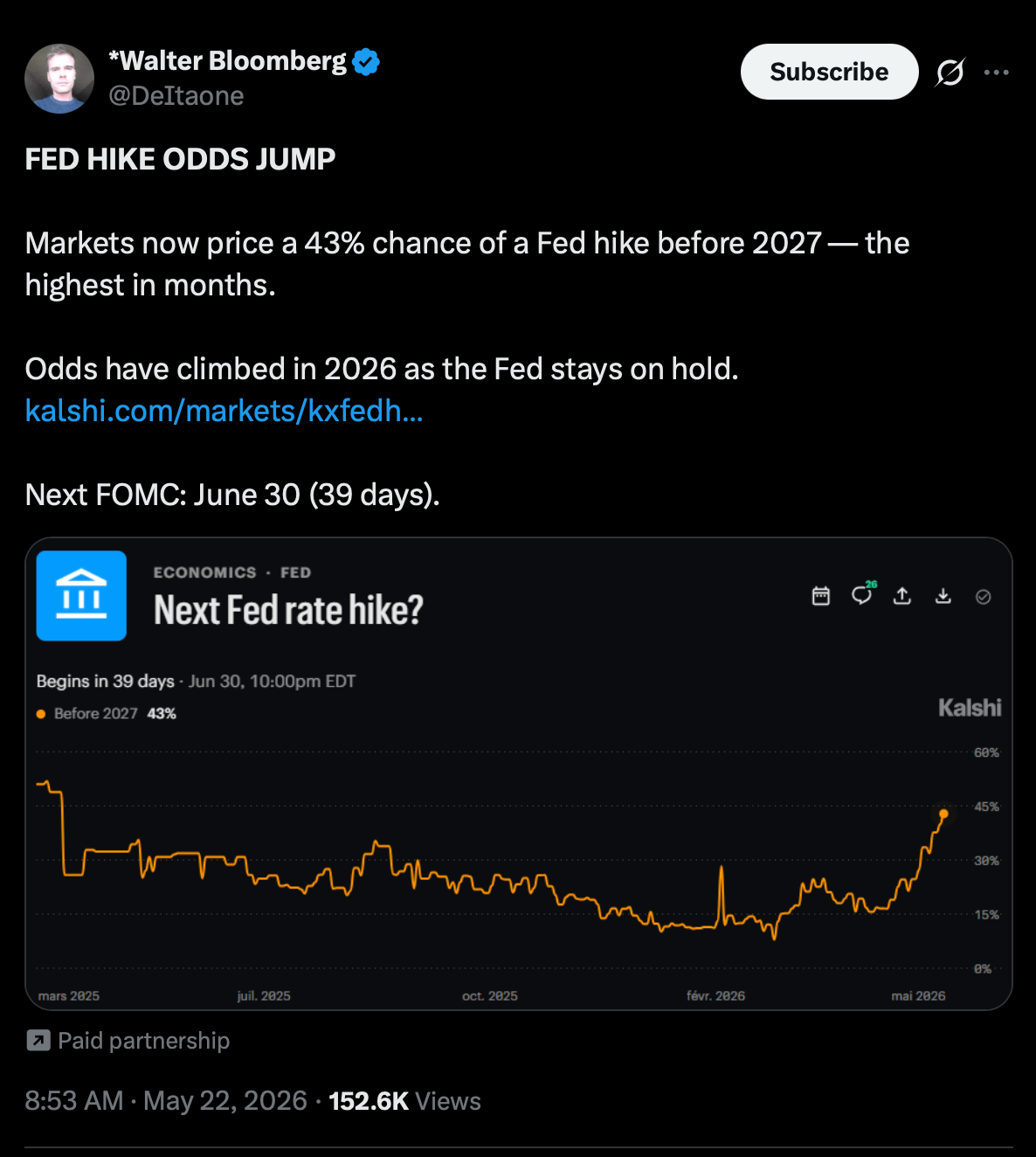

FED HIKE ODDS JUMP.

That headline blasted across financial Twitter Friday morning. Literally the same moment that Justice Clarence Thomas swore in Kevin Warsh as the new Chair of the Federal Reserve, in the East Room of the White House.

Translated: “Rate hikes are back on the table for the first time in over a year.”

Interesting.

Now look at this one.

That was the President of the United States, on the very same day, at a campaign rally in Suffern, New York.

“Housing’s all about interest rates.“

“Get the interest rates down, everybody’s going to be very, very happy.“

Rates coming down “very quickly.”

Same day, two diametrically opposed opinions blasted from opposite directions.

The market pricing hikes. The President promising cuts. A new Fed Chair sworn in between the two of them, the Bible still warm from his oath.

If you have been paying attention to bond markets or reading The Informationist, you are well aware that this rate hike conversation has been building for months. Quietly at first, pretty much ignored. Then the data turned and inflation reaccelerated. Oil spiked. And now, the possibility has gone from fringe theory to deeply real.

And now a few questions are hanging over many Americans this morning.

If Warsh actually pulls the trigger from here, what happens to my mortgage? My credit card APR? My home value, investment portfolio? My 401(k)?

And maybe the biggest question of all:

Does a Fed hike even still work the way it used to?

All good questions, super important. And ones we are going to answer, nice and easy as always, here today.

So, pour yourself a big cup of coffee, and settle into your favorite seat for a candid look at exactly what would happen if the Fed actually raises rates from here with this Sunday’s Informationist.

Partner spot

After 17 years, bitcoin is still widely misunderstood. You get it, but what about the bitcoin blind spots you don’t know you have?

Unchained just released Rethink Bitcoin → — a free interactive course covering the protocol, savings, custody, and network effects across 12 lessons and 21 interactive figures. This is the kind of thing you wished existed when you were learning, and the new best resource for those just beginning the journey.

For the friend or family member who won’t sit through 12 lessons, We partnered with Atlantic Re:think to make a short film for the curious featuring Natalie Brunell, Natalie Smolenksi, and our CEO Joe Kelly. Not the crypto story. The bitcoin story.

🦅 What Warsh Just Walked Into

As we get into this today, try to picture the scene Friday morning.

The East Room of the White House. Two Supreme Court Justices in attendance, Clarence Thomas administering the oath and Brett Kavanaugh looking on from the audience. Jane Lauder Warsh, the new chairman’s wife, watching from the front. President Trump making the introductory remarks.

The most eyebrow-raising line from Trump, given his track record of publicly hammering Jerome Powell to cut rates? “want Kevin to be totally independent... Don't look at me, don't look at anybody, just do your own thing...”

Then Warsh took the podium.

His first words struck a particular note. Humble. Serious. The opening of a man who appeared to understand exactly what he was being handed:

“These duties are now mine, Mr. President, because of the trust you have placed in me. I accept them with gratitude and will strive every day to serve our fellow citizens well.”

Then he laid out his guiding philosophy, the lens through which he intends to run the most powerful central bank in the world:

“Our mandate at the Fed is to promote price stability and maximum employment. When we pursue those aims with wisdom and clarity, independence and resolve, inflation can be lower, growth stronger, real take-home pay higher, and America can be more prosperous.”

A few key words in there.

Price stability. Independence. Resolve. Lower inflation. Stronger growth.

That is the same language Paul Volcker used. Serious. Deliberate. Hawkish to its core.

By the close of trading Friday, Fed funds futures were pricing a 50 to 60 percent probability of a rate hike by early 2027. Better than a one-in-three chance before this year is even out.

It appears that the market heard Warsh exactly the way he intended to be heard.

But here is where things get a bit strange.

Look at what the institution Warsh just inherited has actually been doing for the last six months. (Note: this is not on Warsh. He literally got there yesterday. He has done none of it.)

Quantitative Tightening (the Fed’s process of letting bonds roll off its balance sheet and shrinking the money supply) formally ended on December 1, 2025. That was Jerome Powell’s last meaningful call before stepping toward the door. After nearly three years of unwinding, the Fed stopped letting bonds mature without replacement.

Then it went further.

On December 12, 2025, the Fed started actively buying T-bills again. $40 billion a month.

Ah yes, a new need for stealth liquidity always comes with a new acronym.

This one is RMP, short for Reserve Management Purchases.

Nifty.

In any case, the pace was trimmed slightly in April. But combined with mortgage-backed security reinvestments, the Fed’s balance sheet has still been growing by roughly $40 billion a month, every single month, right up to today.

That’s right.

For the last six months, while the Fed was holding the policy rate steady and lecturing the country about being patient on cuts, the balance sheet was growing. Quietly. Mechanically.

Now, before the word police come at me here, it is true that RMPs are not QE.

I agree. The distinction is fair.

Reserve Management Purchases exist to maintain bank reserves at “ample” levels, a lesson the Fed learned the hard way in September 2019, when reserves drained too low and caused great stresses on debt and Treasury markets.

The intent of RMPs is different from QE. The transmission is different. The Fed will tell you, loudly and accurately, that RMPs are just plumbing or maintenance, not stimulus.

Sure, sure, sure.

But the point that survives it is the one that matters.

See, even when the Fed is not trying to ease, even when the operation is purely technical, the balance sheet still grows. The institution has become a structural net buyer of Treasury debt just to keep the system functioning.

I do believe that Warsh has entered the arena with the best intentions, a clear philosophy, and a serious mandate. He also walked into a Fed that has been quietly expanding for six months running, before he ever set foot in the chair.

And that contradiction is about to get worse. Much worse.

Now we have to ask a question.

If the Fed has to grow its balance sheet by $40 billion a month just to keep money markets running under calm conditions, what happens when real stress arrives?

To answer that, we have to go back to one very specific Wednesday in September 2024. A Wednesday when the Fed cut interest rates by half a percentage point. The biggest opening move in any cutting cycle since the 2008 financial crisis.

And the bond market did something it was not supposed to do.

What happened that Wednesday, and across the hundred days that followed, may be the single most important event in US monetary policy this decade.

Why?

Because it told us, in real time, that the Fed’s most powerful tool no longer reaches the part of the curve that matters.

And it told us, by extension, that whatever Kevin Warsh does next, he is doing it with a broken lever. One that may do the exact opposite of what is expected of it.