US CDS Spreads Blowing Out: Are We Headed for Default?

Issue LI

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🧠 Sound smart? Feed your brain with weekly issues sent directly to your inbox:

Today’s Bullets:

What’s a CDS?

Who buys CDSs?

What are the spreads telling us?

Inspirational Tweet:

US CDS spreads have rocketed higher in price recently, suggesting an accelerating probability of default. But why has this happened, and what exactly is the CDS market telling us?

This is an important one and a little longer this week, so grab that cup o’ Joe and let’s dig in, shall we?

The Informationist is a reader-supported publication. To receive new posts and support my work, consider joining our community by becoming a free or paid subscriber.

🧐 What’s a CDS?

First things first, let’s start at the top. What exactly is a CDS, or Credit Default Swap?

If you’ve been a subscriber of The Informationist, you’ve probably read my past newsletters about CDSs and how they work. If you’re new, though, or just need a refresher, this article is a great place to start:

For the TL;DR crowd, we’ll summarize some of that here.

In short, you may recall hearing about Credit Default Swaps back in 2009, when the entire housing market imploded. The movie The Big Short (based on Michael Lewis’ book, which is eve better, BTW) went into great detail about the housing market implosion and how a few gutsy traders made a killing on it. Still, a bunch of people left that theatre confused about CDSs.

Let’s clear it up.

First, a swap is a contract between two parties (like a legal document) that agrees to swap one risk for another. Simple as that. I’ve traded thousands of swaps in my career, typically for foreign currency and hedging out unwanted risks.

During the housing crisis, CDSs were used to swap the risk of a pool of mortgage debt defaulting on its payments. Owners of the mortgages could get insurance on the default of that debt by buying CDS ‘insurance’.

But unlike typical insurance, you don’t have to actually own what you are insuring when you buy a CDS. You just buy the insurance from whoever is willing to sell it to you. Like buying a policy on your neighbors’ car. If he crashes it, you each get an insurance payout.

Also, remember that default just means an event that triggers a payout. A company or country does not have to go bankrupt for the CDS to be triggered.

Here are examples from the ISDA (International Swaps and Derivatives Association), the governing body of—and the entity that rules on the payouts for—the CDS market:

Now, you may be asking, why would someone sell that?

It’s all about probabilities and premiums. The seller is just betting that the bonds do not default, and they just collect the insurance premiums for a profit.

OK, so, who are they, anyway? Who buys these CDSs and can you buy some if you want?

🎩 Who buys CDSs?

The investors and traders buying CDSs are typically institutions, including large endowments, maybe pensions funds, and definitely hedge funds.

Some of these investors have massive positions in corporate or government bonds, like US Treasuries, which we will focus on today. And they use CDS swaps in order to hedge out some of the risk they have assumed by buying these bonds.

See, if a company or country stops paying interest on their debt, they are in effect default. In the worst cases, the debt can become worthless. Though, in most cases, since debt sits higher in the capital structure than equity, even in the event of bankruptcy, there will be some claims on the assets of the company.

If you want to know more about how the capital structure of companies work, I wrote all about that, you can check it out for free here:

The second type of buyer of CDSs are speculators, those using the spreads to make bets for or against the eventual default.

I.e., if you’re a big hedge fund and you think the Italy's chances of defaulting on their debt will rise in the near future, you can buy a CDS on Italian sovereign debt as a trade.

As the risk of default rises, so does the price of the CDS. And vice versa.

Okay, so this seems easy enough, as an individual investor, can I go out and buy some CDS insurance myself?

Well, seeing how these contracts are priced and traded in $10 million contracts and you would need an ISDA agreement with your broker, not likely.

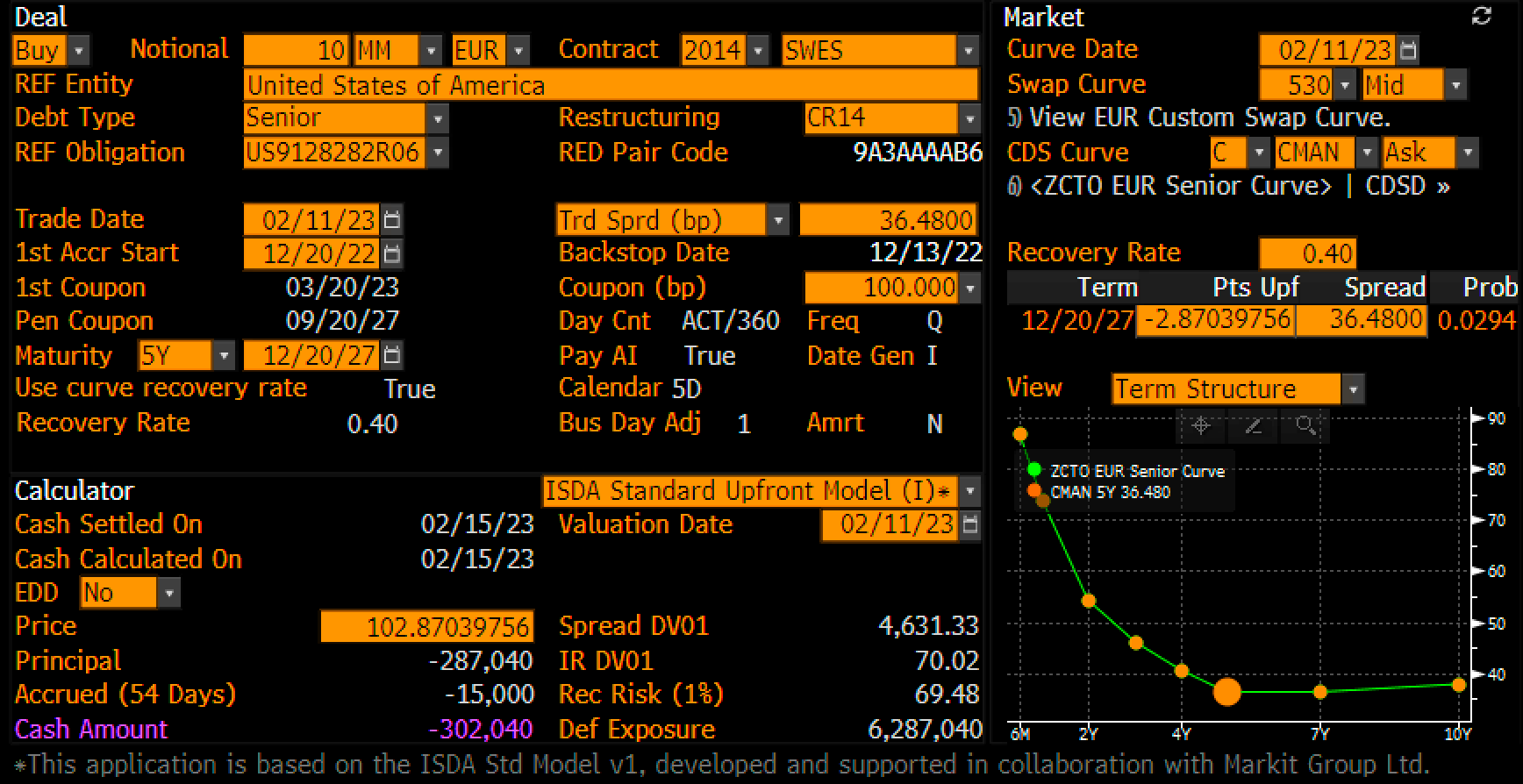

Also, I’m simplifying things greatly here for everyone to grasp the basic concepts. In reality, when an investor goes to price out a CDS they want to buy, they use complicated probability and duration based models that look something like this:

😱 Moving on…

😵💫 What are the spreads telling us?

Getting back to the whole point of all this, what exactly are the current CDS prices on US sovereign debt, in particular, telling us?

As Gianluca pointed out above, the 1-year US CDS has skyrocketed this past month.

What’s more, is the US 1-year CDS is almost twice as expensive as the US 5-year CDS (the contract that is normally quoted for sovereign CDSs). And US is the only country that has spiked recently.