💡 The Fed Has a Big Problem

Issue 174

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🫶 If this email was forwarded to you, then you have awesome friends, click below to join!

👉 And you can always check out the archives to read more of The Informationist.

Today’s Bullets:

What is a Fed Remittance?

How Deep is the Hole?

Will It Ever Get Paid Off?

Inspirational Tweet:

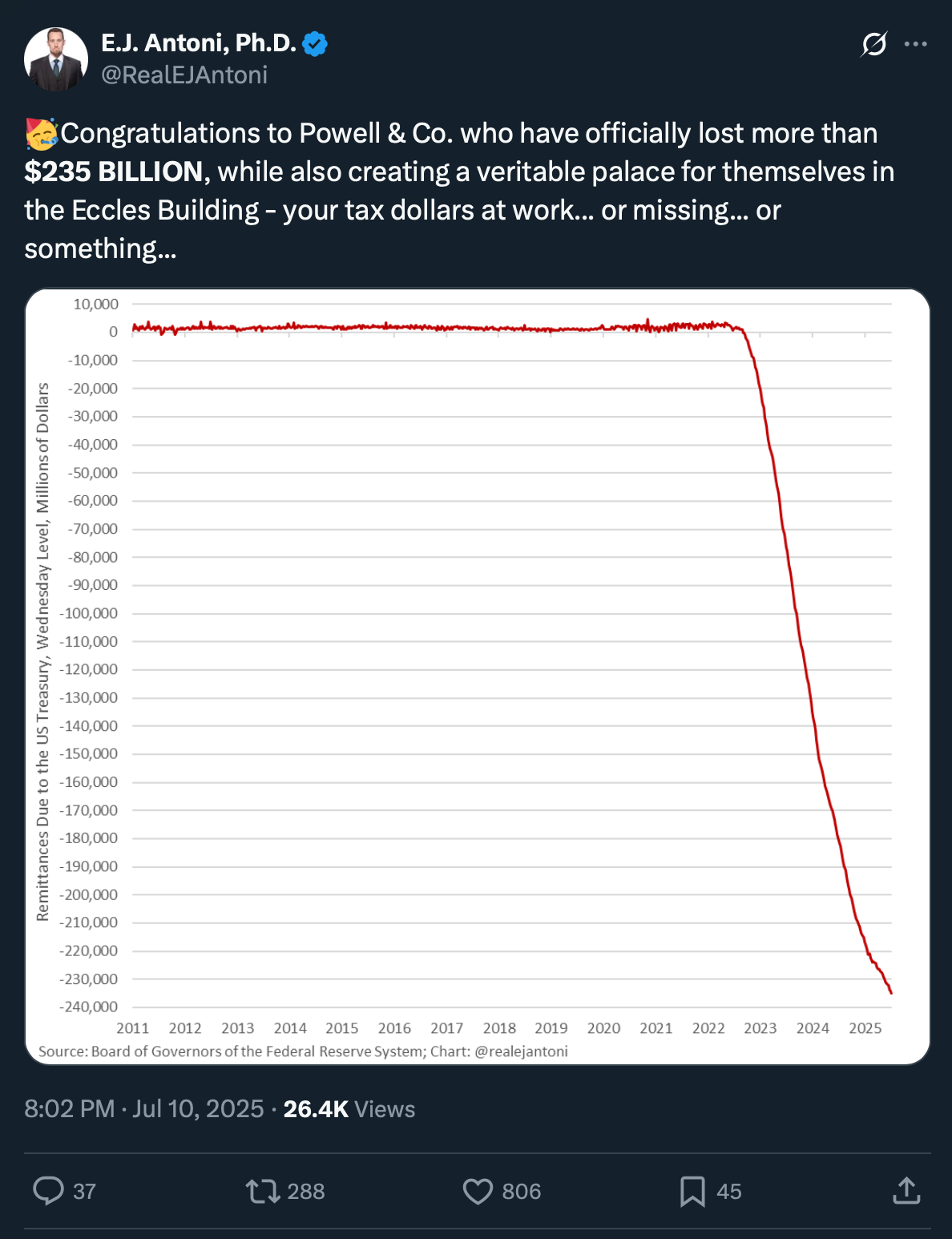

So, that looks bad.

But what exactly is it, and how on earth is the Fed losing money? And does it even matter, I mean to you?

Well, it should, and we’re here to tell you how and why and what it all means.

But don’t worry, we’re going to do it nice and easy, as always.

And by the end of today’s little deep dive into the backroom plumbing of the Fed, you’ll not only be smarter, but you’ll have an idea how you can protect yourself from these kinds of government shenanigans in the future.

So, pour yourself a big cup of coffee and settle into your favorite chair for this Sunday’s Informationist. It’s a long, but good, one.

🥸 What is a Fed Remittance?

First off, let’s clear up the chart we are looking at above, what it represents.

I know it says, Fed Losses, but how? and why?

Well, to put it simply, the Fed has numerous geographically located units that operate much like regional branches of a big commercial bank—all feeding into one central balance sheet. This balance sheet can impact its total revenues and expenses, especially the interest-related line items.

Two of the largest interest bearing assets on the Fed’s books are US Treasuries and Mortgage Backed Securities (MBS). You know, all that paper that the Fed bought during 2021 and 2022 in what is known as Quantitative Easing.

AKA, money printing.

Exactly. The US Treasury presses a button, placing a cash balance at The Fed, who turns around and uses it to buy bonds in the open market, and then the US Treasury pays the Fed interest on the majority of those bonds (the USTs).

A government-entity circular reference.

Incredible, isn’t it?

OK, what about the liabilities? What is the Fed is paying interest on, and to who?

Good question.

See, there are over 5,000 banks, credit unions, etc. that hold accounts at Federal Reserve Banks and maintain balances in these accounts to make and receive payments.

These are called reserves, and the Fed pays the depositors interest on these reserves at a rate known as the interest rate on reserve balances (IORB rate).

A hefty one, too, as you will see in a moment.

In any case, you add up all the payments made and received, as well as operating expenses—you know, salaries, benefits, travel expenses (like conferences and symposiums at Jackson Hole and Davos) and you get to the bottom line.

The net profits (or losses) of the Fed.

Here’s where it gets interesting.

Under U.S. law (specifically 12 U.S.C. § 289), each of the twelve Federal Reserve Banks is required to send any net earnings to the Treasury on a weekly basis. These “earnings remittances” are what’s left after covering the Fed’s own operating costs and paying a small dividend to member banks. In effect, they serve as a kind of cash rebate to the federal government.

See, the Fed is then supposed to send all of its net profits back up to the Treasury, help the budget, so to speak.

The remittence.

And during the free-and-easy-money-decade of 2011–2021, those remittances were substantial, as you can see here.

That’s right, somewhere around $1 to 2 billion per week sent from the Fed to the Treasury. That adds up to nearly $920 billion—payments that helped quietly reduce the federal deficit without any actual financial responsibility out of Congress.

As if.

But that spigot shut off in 2023.

And to understand why that spigot shut off, and why it may not flow again for years, we first need to look under the Fed’s financial hood. Check the Fed’s assets and liabilities.

Here are the Assets:

We see $4.2 trillion of USTs and 2.1 trillion of MBS securities. Remember, the Fed collects interest on these from the Treasury.

What’s the yield on all that debt? According to the NY Fed, it’s approximately 2.3 to 2.4%.

Then the Fed has its own interest-related items on the liability side of its balance sheet—where it pays interest to another party.

This is mainly paid to thousands of banks, credit unions, etc. that have accounts at Federal Reserve Banks.

The reserves.

$3.34 trillion of reserves, to be exact.

So, it holds more securities than it has to pay interest on.

All is good, right?

Right?

Not exactly. Because the rate the Fed is paying is a bit higher than what it is receiving from the Treasury.

Oh. And let’s not forget the second item on the list on the liabilities above, the Reverse Repurchase Agreements—where the Fed pays banks or other institutions interest on cash that they park at the Fed. The IORB rate we mentioned above.

What a deal.

So, what rate is the Fed paying on all these liabilities?

Currently, the Fed pays 4.4% on 3.34 trillion on the bank reserves, and it is paying between 4.25 and 4.5% on the $609 billion of reverse repos.

Ouch.

You don’t have to be a math genius to figure out the math isn’t mathing for the Fed here.

OK, so how bad is it, exactly? What kind of losses are we talking about here, will it continue? And is there anything else we need to know?

🧐 How Deep is the Hole?

Now that we’ve seen the balance sheet, let’s take a peek at the reported financials of the Fed for 2024 to get a sense of how much pain all this interest expense imbalance has caused, shall we?

Here’s a snip of the official 2024 Financials, as reported by the Fed: