In this episode, we explore the whirlwind world of hyperinflation: what it is, how it wreaks havoc on economies, and the countries that have fallen prey to its devastating effects. We dive into how markets react during hyperinflation and discuss the potential for the US Dollar, the world's reserve currency, to hyperinflate. Finally, we discuss strategies and steps you can take to safeguard your assets and protect yourself in the unlikely event of such economic turbulence.

Today’s Bullets:

What is hyperinflation?

Other currencies that have hyperinflated

What happens to markets in hyperinflation?

Could the USD hyperinflate?

How you can protect yourself

Relevant Charts:

Links:

Full Transcript:

Hyperinflation.

With quite a bit of the world experiencing high inflation the past two years, we’re starting to hear the term hyperinflation thrown around a lot recently. Especially as we see signs of some currencies beginning to hyperinflate today.

And plenty of people are wondering: could the US Dollar hyperinflate, too?

But before we get ahead of ourselves, let’s start at the beginning.

First things first. What exactly is hyperinflation?

Well, hyperinflation is when a currency experiences extremely high and accelerating rate of inflation, leading to a rapid erosion of its purchasing power.

As a result, the value of the currency falls so quickly that it becomes practically worthless, and people must resort to using alternative forms of money or bartering for goods and services.

Though incredibly subjective, the academic definition for hyperinflation is when a country experiences inflation rates above 50% per month. Not before that.

So, 49% equals regular inflation and 50% equals hyperinflation.

Hmmm.

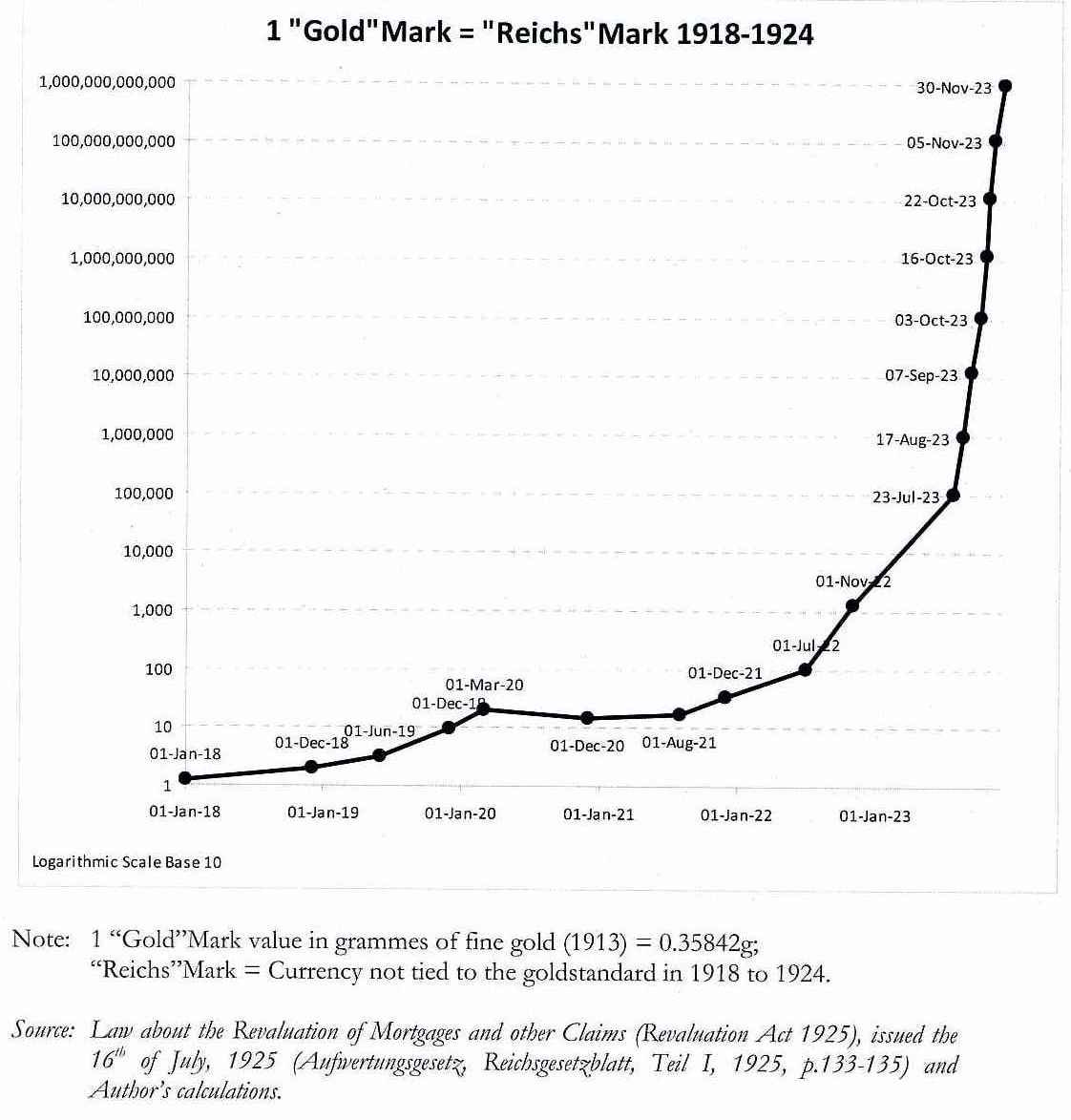

In any case, it’s hard to discuss hyperinflation without examples of the Weimar Republic being raised. And you’ve likely seen charts and graphs of Weimar German mark hyperinflation before.

If not, there’s one included in the show notes. But for those who are just listening, I’ll describe it here.

Basically it shows how many Reich Marks each Gold Mark was worth between 1918 and 1923. And while volatile during the whole period, from 1918 to 1921, each Gold Mark was worth on average somewhere between 1 and 10 Reich Marks. Then, when hyperinflation hit, it skyrocketed higher over the next three years, until each Gold Mark became worth 100 Reich Marks, then 1000, then 100,000, and in late 1923, just three months after hitting 1,000,000, each Gold Mark became worth over 1 billion Reich Marks.

A full and breathtakingly parabolic debasing of a currency.

Hyperinflation.

But what caused it?

Simple. Money printing.

Well, well, well. Where have we heard that term before?

See, in order to pay for war reparations imposed by the Treaty of Versailles, the Weimar Republic German government began printing excessive amounts of money.

This ultimately led to a collapse in the value of the German mark, as you can see above, with prices doubling every few days by the end of 1923.

In a span of just a few years, a gold-backed currency that was ‘worth’ one paper mark was suddenly worth one billion of them.

And so, the Weimar Republic German mark was eventually replaced with a new currency, the Rentenmark, which was backed by real estate assets.

As for causes, hyperinflation is basically the result of poor monetary and fiscal policy, leading to large budget deficits (government spends far more than it makes), which eventually requires excessive money printing (it has to print money to buy its own bonds to keep the debt charade going), and this leads to a total collapse of confidence in the currency (who wants to hold a currency that is rapidly devaluing?)

And finally, a collapse of the currency itself.

In short,

poor fiscal policy leads to budget deficits, which leads to money printing, which leads to the collapse of confidence in a currency, which ultimately leads to the total collapse of a currency

You may now be asking, where else has this happened, can it happen again, and could it happen to the USD, too?

Let’s answer these one by one.

First. Hyperinflation has, in fact, occurred in a number of currencies in modern history.

For instance, during the breakup of Yugoslavia in 1992 to 1994, the government resorted to printing money to finance war efforts and social programs. This led to an inflation rate of over 300 million percent per month.

And it ended with the introduction of a new currency, the convertible dinar.

In Zimbabwe from 2007 to 2009, reckless monetary policies, including massive money printing to finance budget deficits, led to hyperinflation of a staggering 89.7 sextillion percent per month

That’s an 897 followed by 21 zeros of inflation. Per month.

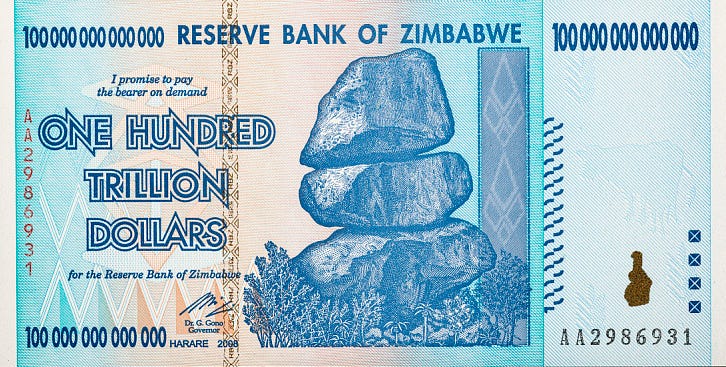

You may have seen photos of hyperinflated Zimbabwe currency, like the one in the show notes.

A One Hundred Trillion Dollar Bill.

Zimbabwe eventually abandoned its currency and adopted a multi-currency system, primarily using the USD.

The worst inflation ever recorded occurred in Hungary in 1956 to 1946, where after WW2, the Hungarian government printed endless amounts of money to finance reconstruction efforts and repay war debts.

The result?

Prices in Hungary doubled every 15 hours. This means the Hungarian pengő lost over 90% of its purchasing power every 4 days.

Because that’s so hard to even conceptualize, let’s put it in theoretical pricing reality.

This means,

A gallon of gas that costs $4 today:

Costs $8,192 after a week,

and $112,000,000,000,000 (112 trillion dollars) after a month.

Groceries that cost $120 today:

Cost $245,760 after a week,

and $336,000,000,000,000 (336 trillion dollars) after a month.

Rent of $1500 today:

Costs $3,072,000 after a week,

and 4.2 quadrillion dollars after a month.

Hard to even conceptualize with the numbers right there in front of you.

In the end, Hungary introduced a new currency, the forint, which was pegged to?

You got it. The USD.

And some countries where inflation is currently raging out of control are Argentina, Lebanon and Venezuela, where rates are being reported at over 100%, 250%, and 500%, respectively.

There’s little doubt that each will fall victim to the academic definition of hyperinflation soon.

But let’s next look at what happens to markets before, during, and after hyperinflation.

It would seem to reason that certain markets fluctuate wildly due to hyperinflation. But there’s an evolution to the fluctuations that we should look at to understand what we can do to protect ourselves in the event of hyperinflation in our own currencies.

The domestic stock, housing and precious metals markets become extremely volatile, especially when priced in the hyperinflating currency.

Before hyperinflation:

Stock markets: Initially, stock prices may rise as investors seek to hedge against inflation by investing in companies that hold real assets or have pricing power. However, the stock market can become increasingly volatile as inflation expectations grow and uncertainty increases.

Home prices: Home prices might initially increase due to inflation expectations and the increased cost of building materials. However, demand may decline as uncertainty grows.

Hard asset prices: Hard assets like gold, silver, and other commodities often become more desirable as investors seek to own assets valuable in any currency.

During hyperinflation:

Stock markets: The stock market becomes highly volatile with periods of rapid growth followed by sharp declines. The real value of stocks (adjusted for inflation) decreases significantly, and many companies will fail due to economic challenges from the hyperinflation, including reduced purchasing power, higher input costs, wage problems, fx impacts, etc.

Home prices: Home prices in nominal terms may rise, but their real value (adjusted for inflation) likely declines. Still, prices remain somewhat stable, as people seek ways to protect their money by buying hard assets, and foreign investors buy at decreased exchange rate values.

Hard asset prices: Hard assets retain their value during hyperinflation, as they are seen as a store of wealth. Demand for gold, silver, and other commodities surges in the region, along with local prices for them.

After hyperinflation:

Stock markets: As a country stabilizes its currency and implements economic reforms, stock markets can start to recover. However, this process can take time and is marked by significant volatility.

Home prices: The housing market can also stabilize as the new currency or monetary reforms are adopted. As the economy recovers, home prices may begin to rise again, at a more sustainable pace.

Hard asset prices: Outsized demand for hard assets declines as stability returns, and investors regain confidence in the currency and financial system. But hard monies retain their global purchasing power.

One key to note in all of this, is that countries with hyperinflation typically have a collapse of confidence in their banking system, and a run on the banks.

Investors, seeking to buy hard assets, withdraw as much capital as they can before the banks freeze accounts and refuse to distribute cash to customers. We’ve seen this exact thing happen in Lebanon this year, with irate customers resorting to robbing their banks in order to get their own money back.

Any way you cut it, hyperinflation is a painful currency phenomenon that leads to serious civil unrest and financial devastation for the average citizen.

Unfortunately, no single country is immune to the phenomenon.

So, does that mean that the US Dollar could hyperinflate, too?

Will it?

Well, let’s be clear. While it is a non-zero chance that the US Dollar hyperinflates in the near future, my personal belief is that the US Dollar will be one of—if not the—last currency to hyperinflate in the world.

And even then, it is a long, long way off—again, in my opinion.

Did you notice in the examples above, how a number of the currencies that hyperinflated eventually created a currency that was pegged to the US Dollar?

This means that the currency exchange rate does not fluctuate against the US Dollar, and is essentially fixed to the US Dollar, moving with it lock and step. The only way to do this is to maintain a constant supply of the currency and not print excessive amounts of it due to fiscal deficits or other problems.

This also means the country will issue a significant portion of their debt, and hence reserves, in US Dollar because of its stability and liquidity.

This keeps global demand for US Dollar high, and as more and more currencies hyperinflate in the future, many folding into the US Dollar, demand for US Dollars simply grows.

But if you’ve seen me write about the US debt problem, the so-called debt spiral, you know this simply cannot last forever.

If you have not yet seen that article and want to read more about it, you can find a link to that in the show notes.

TL;DR: Like a financially deadly game of musical chairs, the US Treasury will keep playing the music (issuing debt and monetizing that debt), as investors slowly wise up to the risks of holding the so-called risk-less USTs and buy hard assets instead.

The music will keep playing until there are no seats left.

And when the music stops, if you’re left standing with no seat—no hard assets—tough luck, kid. You’ve been devalued.

Broke.

The US Dollar gets reset and the game starts all over again.

So, How can you protect yourself?

I’ve been talking about it quite a bit recently, and as we’ve outlined above, one of the best ways to protect your hard-earned money is to own hard assets.

Gold. Silver. Bitcoin.

And yes, real estate, too.

I personally own all of these things as long-term investments, stores of value. How much you own is personal and up to you and your financial advisor.

But as we saw above, in times of hyperinflation, no matter where you live, buying these assets is essential to protecting your money.

One thing to note here, is that it is also essential to buy physical assets, not just paper contracts of them. Owning a house, you have the land, the dwelling, the physical property.

Owning gold or silver coins, you have the physical hard monies.

Owning Bitcoin in cold storage, where you manage and maintain the keys, is hard money.

But owning a gold paper ETF, i.e., one that is not exchangeable for physical gold, only a theoretical paper derivative of it, is not hard money. It’s an IOU.

Same thing goes for Bitcoin owned and held on a trading exchange.

These IOUs will be the first to evaporate in the times of a crisis.

So please, be super aware of what you own, and how you hold it.

It may be the difference between having a seat, or being left standing when the music does in fact, stop.

And the music, eventually…always stops.