💡Is Elon Musk the Richest Man in History?

The world just minted its first trillionaire. The number is stranger than it looks.

✌️ Welcome to The Informationist, the newsletter that makes you smarter about money in just a few minutes each week.

🙌 One topic. Exposed and explained so you can make better decisions with your money. Like a simple walk down Wall Street.

🫶 If this was forwarded to you, you have awesome friends. Join 47,000+ readers here.

Today’s Bullets:

🧮 How Do You Measure the Richest Person Ever?

💸 The Number Nobody Can Actually Spend

🔑 How the Ultra-Rich Turn Paper Into Cash

💰 What This Means for You and Your Money

Inspirational Tweet:

“Officially the first trillionaire in human history.”

That crossed my feed Friday morning, along with countless other posts with similar sentiment. In fact, it’s pretty much the only thing people on Twitter were talking about all day.

For the first time in history, a trillionaire has been minted, so to speak.

And it made me think about how someone becomes so insanely wealthy.

Forget a trillion dollars, let’s start with a billion.

I grew up middle class in a small town in upstate New York. Modest. Nobody that I knew had money like that, not anywhere close. Then, in my twenties, I landed on Wall Street. Suddenly surrounded by and trading in millions of dollars daily.

Eventually I began to see multi-millionaires and billionaires do things with money I had no idea were even possible. Things I didn’t know were necessary, until I saw for myself why people with that much actually need them.

Before we get into that, though, let’s step back and ask a few questions that may already be on your own mind.

Is a trillion today even bigger than the billion that crowned the first man ever to hit that mark, a hundred years ago? If almost none of that trillion is money Musk could actually spend, how does he live like the richest man alive? And perhaps the most important question on your mind: what does the way these people really handle their money tell you about handling your own?

All good questions. And ones we are going to answer, nice and easy as always, here today.

So pour yourself a big cup of coffee and settle into your favorite seat for a look at what the biggest number in history is really worth, with this Sunday’s Informationist.

Partner spot

After 17 years, bitcoin is still widely misunderstood. You get it, but what about the bitcoin blind spots you don’t know you have?

Unchained just released Rethink Bitcoin → a free interactive course covering the protocol, savings, custody, and network effects across 12 lessons and 21 interactive figures. This is the kind of thing you wished existed when you were learning, and the new best resource for those just beginning the journey.

For the friend or family member who won’t sit through 12 lessons, we partnered with Atlantic Re:think to make a short film for the curious featuring Natalie Brunell, Natalie Smolenski, and our CEO Joe Kelly. Not the crypto story. The bitcoin story.

🧮 How Do You Measure the Richest Person Ever?

To begin, let’s go back to the last time this happened.

September 29, 1916. Newspapers across the country woke up and crowned a man the first billionaire in history. Not because he had sold anything or cashed a check. His shares of Standard Oil had simply soared, somebody did the calculation, and the number crossed ten figures for the first time anyone had ever seen.

His name was John D. Rockefeller.

Sound familiar? It should.

If you grew up like me, then you would have heard the phrase, “What do we look like the Rockefellers?” any time you asked for something that was not in the budget. More than a century later, the name still means rich beyond reason. That is how completely a single fortune can stamp itself onto a country.

Rockefeller was crowned the richest man alive by a moving stock price, on paper, before he sold a single share. A hundred and ten years apart, Musk on Friday and Rockefeller in 1916 earned their crowns the exact same way.

The Breakup That Backfired

Now, the wrinkle. Five years earlier, in 1911, the Supreme Court ordered Standard Oil broken into 34 separate companies, the most famous forced breakup in American business history. The government meant to cut Rockefeller down to size. Lo and behold, just like almost every single other government-driven intervention, it backfired, spectacularly.

The reason is worth understanding, because the same piece of market machinery is still in use today.

Rockefeller owned about a quarter of the old trust, so when it was split, he received a quarter of the stock in every one of the 34 pieces. Then something strange happened once those pieces traded on their own. Investors added them up and found the parts were worth far more than the whole had ever been.

A giant, opaque monopoly sitting under a legal cloud is hard to price, so the market discounts it. Cut it into clean, separately traded companies, and that discount melts away. Suddenly investors could see exactly what each piece was worth, and they bid them up. Within two years the combined value of the “Baby Standards“ had doubled.

By 1913 his fortune was pushing $900 million, and within a few years the press would hand him the billion-dollar crown we started with.

Wall Street has a name for what happened to him. Unlocking the sum of the parts. The very same argument gets made in boardrooms and antitrust fights to this day.

The breakup meant to humble him made him richer than ever.

oops.

The Rulers

Alright, back to the question of the day. Is Musk’s trillion actually bigger than Rockefeller’s billion?

Depends entirely on the ruler you use. And there are three of them, each one fairer than the last.

The Raw Ruler

A trillion is a thousand billions.

Inherently, you know this is a flawed comparison. Line the two up and Musk wins a thousand to one. Except that tells you almost nothing, because a 1916 dollar and a 2026 dollar are not the same animal, and neither are the two economies they lived inside.

The Inflation Ruler

Then adjust for it. Ask what Rockefeller’s billion would buy in today’s money. Britannica runs that math and gets about $30 billion, which makes Musk roughly thirty-five times richer.

Closer to fair, but still bent.

The dollar has fallen even harder than the official inflation figures admit, so that $30 billion is, if anything, light. But the bigger flaw is what it ignores: the economy Rockefeller loomed over was a tiny fraction of today’s.

The Economy Ruler

Now the only question that is truly apples to apples. How big was each man’s fortune against the entire economy of his day?

In 1916, the whole United States produced about $48 billion in Gross Domestic Product, or GDP. Rockefeller’s billion was therefore around two cents of every dollar in the country.

Today the US economy runs about $32 trillion in GDP. Musk’s trillion comes to roughly three cents of every dollar.

Good God, man.

In any case, two cents then. Three cents now. That is the honest comparison, and look how far it sits from where we began. The raw numbers scream a thousand to one. Inflation says thirty-five. Measured against the economy each man actually stood on, it is three cents against two.

Musk is still ahead. But three-to-two is a different universe from a thousand-to-one.

The dollar is a piece of chewed gum, at best. As it stretches and stretches, the “richest man in history” changes right along with it.

Even once you pick a ruler, though, two things stay true about Musk’s trillion that were never quite true about Rockefeller’s billion.

First, he can’t actually spend most of it.

And it is a fundamentally different kind of wealth than the kind that made Rockefeller rich.

Let’s walk through each of those to understand how and why, and then we will talk about how this all may relate to you and your own financial situation.

💸 The Number Nobody Can Actually Spend

Start with that first claim. He cannot spend most of it.

To see why, you have to know where the number even comes from. Because nobody counted Musk’s money on Friday. They calculated it. A net worth headline is a math problem, and once you can see the equation, the whole illusion comes apart in your hands.

Where the Number Comes From

Every net worth figure you have ever read rests on one piece of arithmetic. Take the price of the last single share that traded, and multiply it by every share a person owns. That is the entire formula. Wall Street has a name for it: mark to market. You take whatever the market last paid, and you mark the whole pile to that price.

Watch it happen in real time on Friday.

Before the opening bell, SpaceX was a private company with no public price at all, and the trackers pegged Musk somewhere in the high hundreds of billions. Then SpaceX shares, ticker SPCX, started trading. They priced at $135, opened around $150, and by the close had run to $160.95.

Musk owns roughly 4.8 billion of those shares.

Do that multiplication and, by CNBC’s tally, the listing piled more than $180 billion onto his fortune in a single session. He crossed a trillion dollars somewhere in the middle of a Friday afternoon.

Now ask the question that actually matters. What did he do that day to earn that $180 billion?

In certain corners of Washington, the answer is “nothing,” and the follow-on is that a number this size is really just untaxed cash the government ought to be helping itself to.

Senator Elizabeth Warren’s Ultra-Millionaire Tax Act, back on the table this spring, would tax a billionaire’s net worth directly, the paper figure itself, whether a single share has been sold or not.

It’s a seductive idea to gain votes, right up until you understand what the number actually is.

Musk didn’t pull that $180 billion out of a vault, because there is no vault.

The market simply slapped a public price tag on a company he already built, the calculator multiplied that tag across his pile, and his number leapt. He sat there and watched it happen, the same as you or I would.

Here’s an important part of that tally.

The price that re-marked all 4.8 billion of his shares was set by the last shares to trade. Maybe a few million changed hands at $160.95. That one price then got stamped onto every share behind it, including the billions that never moved an inch all day. The marginal share, the very last one to sell, sets the official value of every share standing behind it.

You already know this feeling. Open your brokerage app tonight. The number it shows you runs on the exact same metric: the last price someone paid for the stock, multiplied by however many shares you happen to hold. You didn’t sell anything. Nobody handed you cash. A screen multiplied two numbers and called it your wealth.

Musk’s trillion is your brokerage balance with a few more zeros, built the very same way.

Well, let’s be honest. A lot more zeroes.

Try to Cash It In

Which leads straight to the trap. That marked price only holds as long as nobody tests it.

Picture the other side of every trade. At any given moment, a stock has only so many buyers standing there willing to pay near today’s price. Traders call that market depth: the stack of real, live bids waiting in the order book. Sell a hundred shares and you barely scratch the top of that stack. The price doesn’t budge. Sell ten thousand and you start eating down through it.

Now try to sell 4.8 billion.

There is no wall of buyers that deep. Not even in the neighborhood.

No. You blow through every bid sitting near $160, then every bid below that, and below that, chasing the price down with your own selling the entire way. The act of cashing out destroys the very price your trillion was marked at. By the time you’d unloaded any serious chunk of it, the shares still in your hands would be worth a fraction of where they started.

And it gets worse, simply because of who he is. Musk heading for the exit is not a quiet transaction. The moment the market so much as smells him reaching for the door, every other holder sprints for it first.

Bloomberg put it plainly this week: he cannot cash this fortune out like a checking account, and even a hint of him dumping SpaceX or Tesla could crater the price overnight.

I concur.

The trillion, then, is real and unreal at the same time.

Real, because the arithmetic is honest and the shares genuinely exist.

Unreal, because the figure survives on one condition only, that he never seriously tries to turn it into money. The largest paper fortune ever printed, holding its shape right up until the instant someone asks it to become cash.

A Different Kind of Rich

Here is where Musk’s trillion and Rockefeller’s billion part ways for good.

Rockefeller’s wealth paid him. Standard Oil and the 34 companies that came out of it were gushers of cash, and they sent him a steady river of dividends, his cut of the profits, mailed out quarter after quarter whether the share price climbed, sank, or sat dead still. He could light cigars with the cash flow and never once touch the underlying stock. His fortune was a claim on oil already pumped, refined, and sold. Money that existed, in hand, today.

Now, a fair objection. Of course Musk gets paid. Salary, bonus, the works, like any chief executive.

Let’s split two things that get tangled together. A dividend is a return on ownership, the company passing its profits back to everyone who holds the stock. A salary is pay for the job. Most executives collect both.

Musk collects neither in cash. And this is where he turns out to be the exception that proves the whole point.

Neither company pays a dividend. SpaceX never has, and Tesla has never paid a single cent of one in its history.

As for his actual paycheck, that Tesla package shareholders approved back in November, the one the headlines breathlessly call a “trillion-dollar pay deal,” is built entirely out of stock options, twelve tranches of them, with no salary, no cash bonus, and no time-based stock attached (it’s right there in Tesla’s own filings).

They pay out only if he hauls Tesla’s market value from roughly $1.5 trillion toward $8.5 trillion over the next ten years. SpaceX ran the identical play this year, handing him a billion fresh shares that vest only if the company is worth $7.5 trillion and there are a million people living on Mars.

Yes Mars. I am not making that up.

Which means the richest man in history draws no dividend and takes essentially no cash salary. Every last dollar of that trillion, his “pay” very much included, is made of the same stuff: equity. Shares. The exact paper we just spent this whole section watching him fail to turn into spendable cash without setting fire to it.

And the reason these companies hand him stock instead of a fat dividend check comes down to what kind of companies they are.

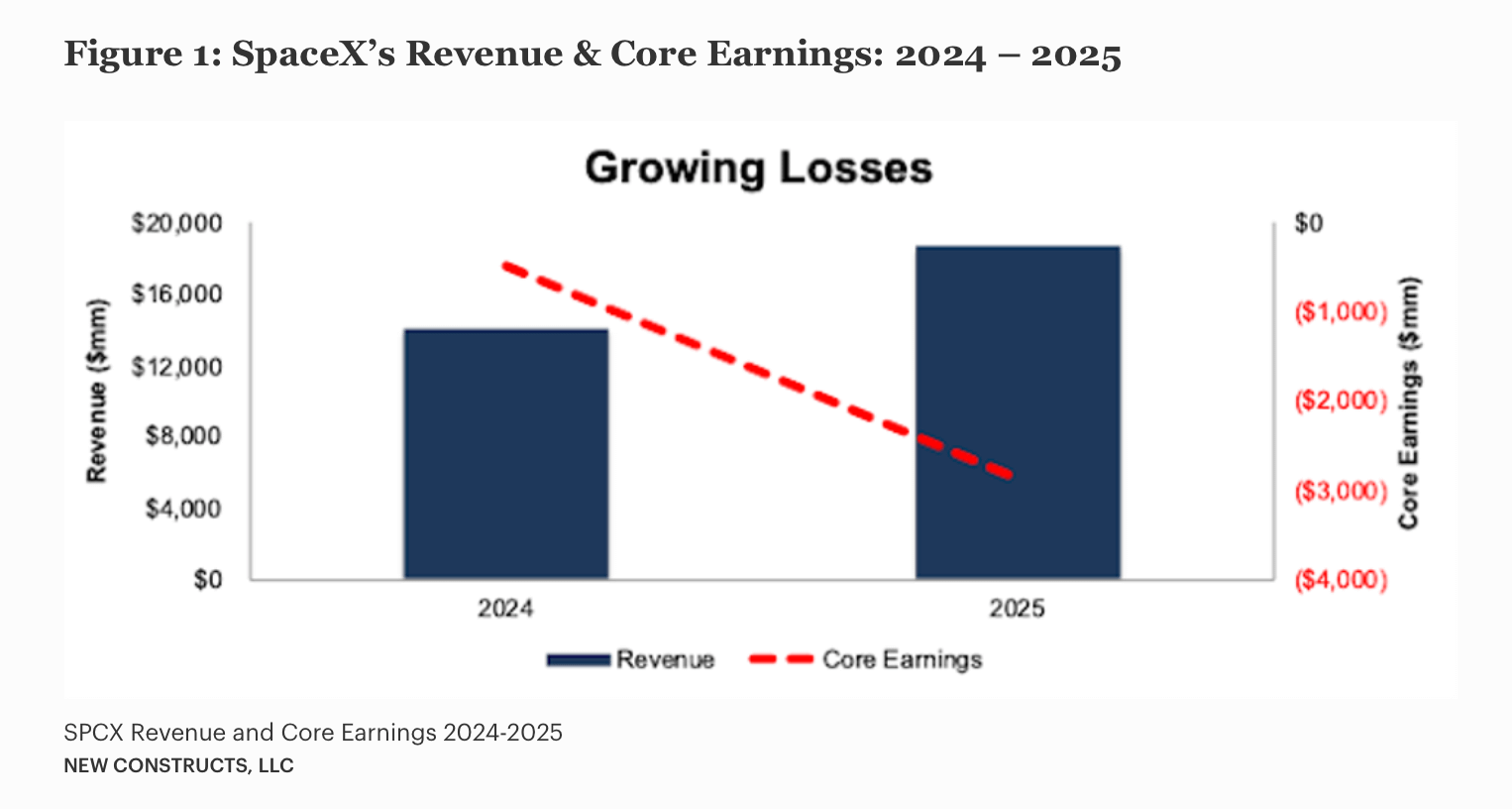

A growth company exists to be fed.

SpaceX pulled in $18.67 billion in revenue last year, up a blistering 33%. And the more it sold, the more it lost. As the chart shows, the losses on its core business widened right alongside the revenue, from under a billion dollars to nearly three billion in a single year. The faster it grows, the more cash it swallows.

At least for now.

In direct contrast, Rockefeller’s billion was a claim on a business minting money right then and handing it over. Musk’s trillion is a claim on what his companies might someday become, a wager that the future shows up and pays.

One man owned a printing press for cash. The other owns a brilliant, ravenous promise.

That distinction is going to matter enormously when we get to your own money in a bit. Tuck it away for now.

Which leaves us with a strange knot. The richest man who has ever lived sits on a fortune he can’t spend without wrecking it, attached to companies that don’t send him a dime to live on.

Then how on earth does he, or anyone with wealth shaped like his, actually live?

Because they certainly do. The ultra-rich buy the yachts and the islands and the influence without ever, as far as the public record shows, selling the golden goose out from under themselves. They cracked this exact riddle generations ago, and the answer is quieter, and a good deal stranger, than almost anyone would guess.

Let’s walk into that room next.

🔑 How the Ultra-Rich Turn Paper Into Cash

Welcome to the room.

This is the part I have watched up close for most of my career, and it is the answer to the riddle we just tied off. A man with a trillion dollars he cannot sell, attached to companies that pay him nothing, still buys the islands and funds the rockets. How exactly?

He borrows.

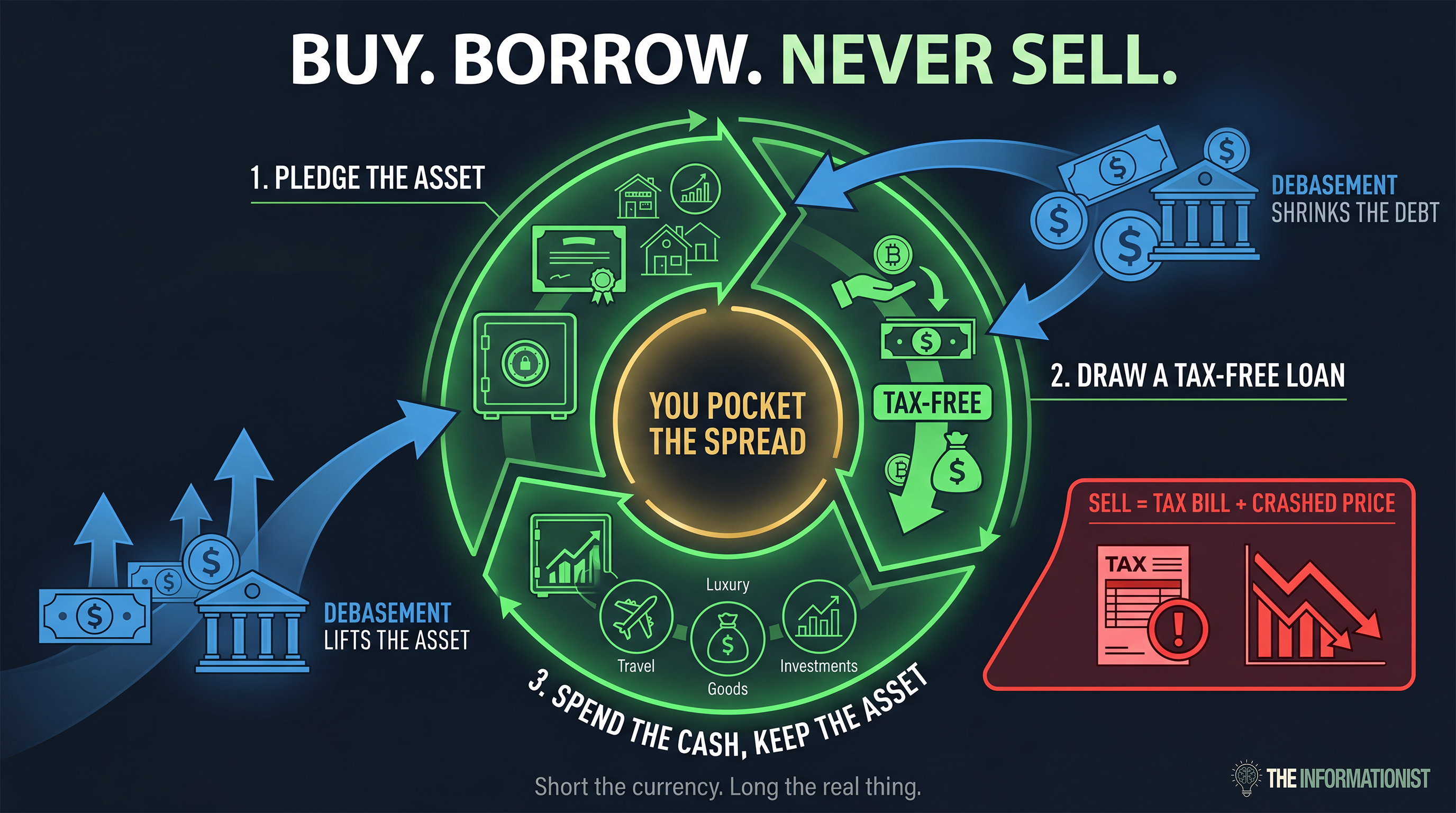

Buy, Borrow, Never Sell

The whole strategy fits in three words, and the estate lawyers have framed them so effectively, they have built entire, and incredibly lucrative, careers around them.

Buy, borrow, die.

Buy assets that grow. Borrow against them when you need cash to live. Never sell if you can possibly help it, and let the next generation sort out the rest.

The genius hides in that middle word. Borrow.

When you sell a stock that has climbed, you hand the government a slice. Sell a billion dollars of stock you bought cheap, and a couple hundred million can go straight to the IRS as capital gains tax, gone, before you have spent a dime of what is left.

A loan plays by entirely different rules, and this is the hinge the whole game swings on. Borrowed money comes to you tax-free. You have to pay it back, so the law treats it as a debt, and a debt is not income. No gain, no tax. You can borrow a hundred million dollars against your shares tomorrow morning and owe the Treasury exactly nothing on it.

You keep the asset. You pocket the cash. And the taxman waits at a door you simply never walk through.

As for the die part, that is the closer. Under current US law, when assets pass to your heirs, their cost basis resets to the market value on the day they inherit. A lifetime of gains that was never taxed, because it was never sold, resets for tax purposes. The estate clears the outstanding loans, the heirs keep the asset, and the capital-gains bill nobody ever paid quietly disappears.

That is the whole reason the strategy ends on that particular word.

The Loan That Lives on Your Shares

Here is the actual machinery, the part everyday people don’t get a chance to see.

The vehicle has a name: a securities-backed line of credit, an SBLOC for short. The private banks dress it up with grander titles for their biggest clients, pledged asset lines and the like, but it’s essentially the same animal.

Here’s how it works:

You pledge your shares to the bank as collateral → the bank opens a credit line against them, and → you draw on it like an enormous checking account

The stock never leaves your name. You still own every share, still keep any upside, still hold the votes. The bank simply gets a claim on them if you stop paying.

How much will they lend?

A portion of the collateral’s value, set by the loan-to-value ratio. Against a big, liquid, blue-chip holding, that amount can run well north of half the value. The richer and more diversified you are, the better your terms, because the bank sees a safer pile to lend against.

Here’s the key, though.

The first dollar is always the hardest to borrow. After that, money gets cheap.

You want to see who runs this play better than almost anyone alive? The man this whole letter is about.

Musk has used his own stock as a cash machine for years, right out in the open in Tesla’s filings. Back in 2020, the proxy showed he had borrowed roughly $515 million against 265 million Tesla shares, which had a market value on that date of $52.9 billion, more than 100 times the amount of the loans (per the Institute for New Economic Thinking’s read of the filings).

Sounds like a lot to borrow until you do the math. Just look at the ratio.

A half-billion-dollar loan, secured by fifty-three billion dollars of stock. The loan is a rounding error against the collateral behind it.

And he continues to run the same playbook. Tesla recently disclosed Musk had pledged roughly a third of his Tesla shares to secure personal loans, with the board capping what he can actually draw against them at the lesser of $3.5 billion or 25% of the value of the stock.

And he funds his life the same way he built his fortune. Without selling a thing.

The Engine Underneath It All

Now the piece that turns a clever tax maneuver into something close to a wealth machine. Longtime readers, you can already feel where this is headed.

Debasement.

When you borrow, you lock in a debt denominated in today’s dollars. A fixed number.

The melting ice cube itself.

Like I have said before, it does not matter who is in office, who is at the helm of the Fed, the reality is the math. And the math is ugly.

Year after year the dollar gets debased, quietly bleeding purchasing power, and that fixed debt you owe shrinks right alongside it in real terms. You end up repaying tomorrow’s cheaper dollars on a loan struck in today’s more valuable ones.

See, the very same debasement that eats away at the dollar tends to lift the price of the scarce, real asset you borrowed against. The stock. The Bitcoin. The land, the building.

Look at what that combination does. Your debt melts. Your collateral climbs. You are, in plain terms, short the currency and long the real thing, and the spread between the two is yours to keep.

That is the quiet engine humming under a great deal of generational wealth: a loan against an appreciating asset, serviced by a steadily depreciating dollar.

And once you get to a certain level of wealth, banks will just start to lend to you based on your balance sheet alone. It’s called an unsecured line of credit. I watched my hedge fund boss draw from an unsecured line of credit to the tune of over $20 million. No assets pledged against it, no collateral. Just the strength of his personal balance sheet and a promise to pay it back.

But of course he was also borrowing against actual securities and investments in private equity. Massive amounts of collateral to play with and borrow against.

God only knows what that total tally was. I wasn’t privy to that one.

What a world, eh?

The Catch, Because There Always Is One

Before anyone files this under free lunch, hear the other half, because it is the half that wrecks people.

You’ve heard me say it before. Loud and unabashed.

Leverage cuts in both directions.

The entire structure rests on the collateral holding its value. Let the asset fall far enough and the bank issues a margin call: post more collateral, or we sell yours to cover the loan, right now, at the worst possible moment, straight into the very weakness that triggered the call.

It is not hypothetical, even for Musk.

When Tesla stock has slid hard, a deep enough fall could push his pledged shares toward exactly that margin-call line, the same trapdoor that sits under anyone running this play. And for all his aversion to selling, when he needed real money to close the Twitter deal, even he had to unload billions of dollars of Tesla stock to get it done. The master of never-sell, forced to sell.

That, my friends, is the bill leverage always eventually sends.

Hear me clearly on what this is. It is the machine the wealthy actually use, laid bare. Not a recommendation. I am not telling you to phone your broker about a line of credit, and that margin-call story is precisely why.

I am showing you how the gears turn, so that the next part, the part about your money, lands with both eyes open.

Because the surprising thing is how much of this very same machine may already be sitting in your own life. You might even be running a piece of it without realizing.

Let’s go find it.

💰 What This Means for You and Your Money

Start with the biggest thing most people own. The roof over your head.

If you own a home with a mortgage, you are already running a small, quiet version of the exact play we just watched the billionaires run.

Look at the pieces.

You bought an asset that tends to appreciate. You borrowed against it, the mortgage, instead of paying all cash. And you have no intention of selling it to fund your life. Buy, borrow, don’t sell.

Sound familiar?

Now add the part that turns it into an engine.

Your mortgage is very likely a fixed number, locked at the rate you signed years ago. The dollar, as we have established, melts relentlessly. Every year it gets debased a little more, and every year the real weight of that fixed payment gets a little lighter. The $2,500 you owe the bank this year is the same $2,500 you will owe in 2034, except 2034 dollars will buy noticeably less.

You are repaying a yesterday-sized debt with tomorrow-sized dollars.

Meanwhile, that same force tends to push the price of the house itself up over the years.

Look at what you pulled off, quite possibly without ever thinking about it. Your debt is quietly melting. Your asset is quietly climbing. You, the ordinary homeowner with a thirty-year fixed, are short the dollar and long a real asset, the very same position Musk holds with his pledged shares.

Smaller, yes. The same machine, though. Almost exactly.

Now, the usual caution, and you have heard me say it a hundred times. I cannot and will not tell you what to do with your own money. My job here is to help you see the dollar clearly. Because the very same debasement you feel as a pickpocket at the grocery store wears a second face. On your savings, it is a slow leak. On a fixed-rate debt held against a real asset, it works quietly in your favor.

Learning to see both faces at once is the whole point.

Two Questions to Keep in Your Pocket

Set Musk aside for a moment. The reason we walked through any of this is so that the next time a giant number lands in front of you, yours or anyone else’s, you can take it apart yourself. Two questions do most of the work.

First. What is the ruler?

We opened this letter learning that Musk’s trillion and Rockefeller’s billion only mean something once you choose what to measure them against. Raw dollars said a thousand to one. Inflation said thirty-five to one. Set against the whole economy each man stood on, it came down to three cents against two.

Same two men. Three completely different verdicts.

Hold your own numbers to that same test. A portfolio that “doubled” over a decade did what, exactly, after inflation? A gain of 4% in a year when inflation ran at 5% moved you which direction, honestly?

What I’m saying is, the number on the screen tells you very little on its own. The ruler you measure it against tells you the rest.

Second. What is it a claim on, and could you actually spend it?

Every asset you own is a claim on something. A dividend stock or a rental property is a claim on cash showing up today. A growth stock, a stake in a private company, even Bitcoin, those are bets on a bigger tomorrow. Each has its place.

Knowing which one you are holding tells you whether it will ever feed you or only ever grow.

Then the harder half, the half Musk’s trillion just taught us.

Could you turn it into real money if you had to, without wrecking the price on the way out the door?

A few hundred shares of Apple, easily. Your house, slowly and expensively. A large, concentrated position in your own company’s stock, maybe not without the market moving against you the whole time you sold. Wealth on paper and wealth you can spend are two entirely different animals, and the distance between them has humbled people far richer than you or me.

Back to the Crown

Which brings us right back to where we started.

Is Elon Musk really the richest human being in history?

The honest answer is that there is no clean answer, and now you understand exactly why. Line up enough rulers and the question splinters into a dozen different ones.

By raw dollars, he laps the field and everyone who ever drew breath.

Against the economy he stands on, he sits a whisker ahead of a man from 1916.

And measured by what he could actually walk into a bank and spend tomorrow, the honest figure is a small slice of that trillion, the very same bind Rockefeller was in a century before him.

The crown was only ever the hook that got us in the door.

What you carry back out is the better prize. You can read a giant number now and put the right questions to it. You understand why the richest man alive borrows rather than sells, and why the same dollar that nibbles at your savings can quietly help retire your mortgage. And you can look at your own modest balance sheet and recognize the very same machine, turning slowly, that runs the largest fortunes on earth.

Nice and easy, as always.

Which brings me to the short list of things I will be watching in the days ahead.

👀 What I’m Watching This Week

A quick word before the list. Every Sunday, paid subscribers find this same forward look in their inbox: the handful of things I'm tracking, and why they matter for your money. Today it's open to everyone. Glad to have you reading it.

Warsh’s first meeting, the decision Wednesday at 2pm. The rate is a near-lock hold at 3.50 to 3.75%. What matters is everything riding alongside it: the fresh dot plot, the new projections, and Warsh’s first press conference as Chair. Does the plot push the first cut out to 2027, or leave September open? His tone sets the table for the rest of the year.

The 20-year bond auction, Tuesday. Long-end supply landing the same day the Fed sits down and Tokyo reports. The 20-year is a clean stress test of real appetite for long US debt. I’m watching the tail, the bid-to-cover, and the foreign bid. A soft auction into two central bank meetings is how a long-end wobble starts.

The Bank of Japan, deciding the day before the Fed. The bigger story for our long end may be in Tokyo. The BOJ meets June 15 and 16, its scheduled checkpoint on how fast to taper its own bond buying. With the yen pinned near 160 and the 10-year Japanese Government Bond (JGB) near 2.6%, just off an all-time high, the risk is simple: climbing Japanese yields pull Japanese capital home out of US Treasuries, thinning demand for our debt right as we sell that 20-year. Watch the yen and the JGB.

The consumer and housing, Tuesday into Thursday. The last real read before the Fed speaks: May retail sales around Tuesday, housing starts just behind. Retail sales show whether the consumer, nearly 70% of this economy, is still spending. Housing shows what high rates are doing to the corner we spent this letter inside. Jobless claims land Thursday, the last data before Friday’s holiday.

The paper trillion itself. A fitting close. This is SPCX’s first full week trading publicly, the first real price discovery for the stock that minted the world’s first trillionaire. Does the mark hold above a trillion, or do a few red days hand the crown back? Either way, a live lesson in what we just covered: paper wealth is only ever worth the last price someone paid. An observation, plain and simple.

That's it. I hope you feel a little bit smarter knowing what Musk's trillion is really worth, why he can't simply spend it, and how the world's biggest fortunes get borrowed against, never sold.

If you want this kind of deep-dive analysis every single week, join the paid Informationist family right here:

And if you enjoyed this free version of The Informationist and found it helpful, please share it with someone who you think will love it, too!

Talk soon,

James✌️

───

Join 1,598 premium subscription readers who get the full breakdown every Sunday

Interesting read! While aware of the “playbook” of borrow, spend, never sell, how do they actually service their debt? A cash-flowing Rockefeller is obvious, but Elon or Saylor borrowing against his personal BTC stack?

Do they let the interest get added back to principal at YE, and simply refi against the current (higher) asset value?

I know you can’t comment on how specific individuals do this, just curious about the typical options.

James, I'm curious why you didn't compare their wealth measured in gold?

* $1 billion in 1919 bought about 48.4 million ounces of gold.

* $1 trillion in 2026 buys about 237 million ounces of gold.