💡 Informationist Alpha Newsletter

May, 2024

👊 Hey there Informationist Alpha, this is your monthly macro update. Unpolished and raw, these are the main macro themes and factors I'm taking into account for my own portfolios.

Let's get right to it!

As you all know by now, I’ve been paying close attention to the fiscal dominance (read: exceptionally irresponsible spending out of DC), and its impact on the economy.

It’s perhaps has no greater impact than confusion at The Fed.

On the one hand, we have Fed officials eager to cut rates. But with continued strength in the economic numbers, some officials are leaving the door open to rate *hikes*.

Though this is being tempered with possible recession concerns and consumer confidence.

The choices:

Cut Rates Now: The Fed is most inclined to cut interest rates soon in order to avoid an all-out recession, which would be super negative for US Treasury liquidity and may necessitate more QE (a program the Fed is loathe to re-ignite).

That said, there are challenges to this dovish lean.

First, the economic data is simply not bad enough to warrant a cut yet.

Employment (even if being juiced by the White House and all the government hiring) is too strong to suggest a cut. Inflation has been stuck above 3% for almost a year now.

Sticky inflation, indeed.

Also, credit availability (financial conditions) has been loosening for the past year already, regardless of rates and QT.

And so, the money supply (M2) has stopped contracting and is expanding again.

Is anyone surprised now about inflation sticking above 3%? 🙄

In any case, this all limits the Fed’s ability to justify lowering rates without risking a spike in inflation or creating larger asset bubbles.

So, what about rate hikes?

While this remains a non-zero probability, especially if inflation does flare back up again, I rate it a v. low probability at this point.

However.

We are in an election year.

This administration has shown it will do what it takes to appear like it is helping the consumer:

the ‘Inflation Reduction Act’ that has created near-boundless fiscal spending

draining the SPR to keep gas prices low

forgiving student loan debt willy nilly

creating subsides for new home buyers, etc.

In reality, all of these are either short-term fixes or actually exacerbate the inflation problem.

So, I don’t put it past the current administration from creating an inflation forest fire. One that The Fed will be left to clean up (and likely blamed for).

It’s no surprise then that The Fed has been purposely vague in communications.

The Fed’s minutes and public statements have strategically avoided signaling a strong bias towards either rate hikes or cuts. This ambiguity helps manage market expectations and keeps financial conditions tight without causing market overreactions.

By being vague, Powell & Co. aims to prevent financial markets from rallying excessively, which could further loosen financial conditions and further counteract the Fed's policy goals.

JayPow is walking a wire tightrope stretched between Twin Towers.

What are they waiting on, then?

Unemployment to spike.

And while it has ticked up slightly, it has not yet jumped. This is something I am watching closely. Once this happens, we are already in a recession, and the Fed knows this.

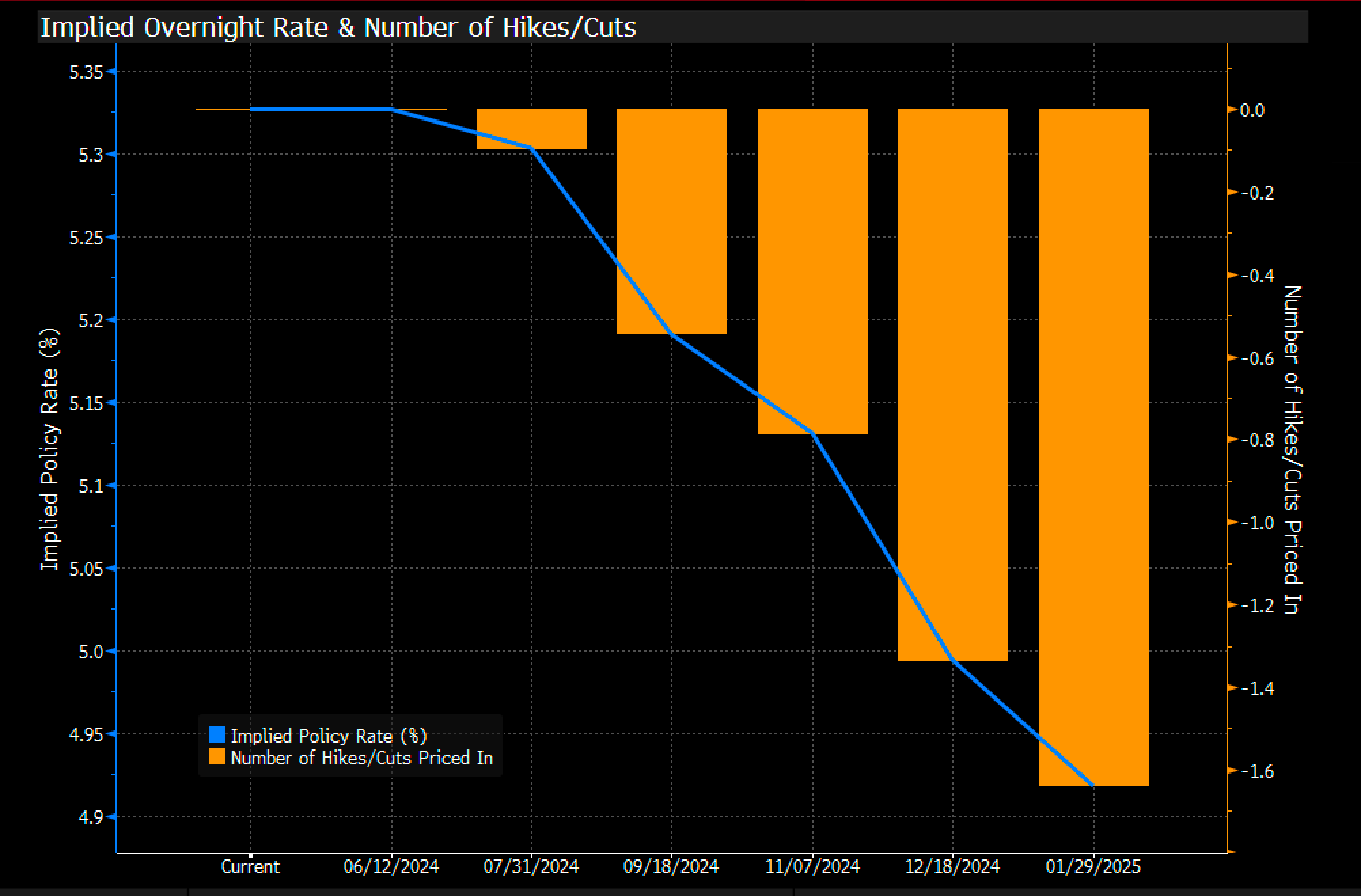

And what does the market think?

Fed futures show investors expect ~50% chance of a rate cut by September and ~80% of one before the election.

The market expects at least 1 rate cut by the end of the year.

Upcoming Economic Indicators

The most important ones:

Home Prices (May 28): Likely to cool due to high borrowing rates

Consumer Confidence (May 28): Anticipated to drop due to job market cooling and high prices

GDP Growth (May 30): Expected to be lower for Q1, showing fading momentum in economy

Jobless Claims (May 30): Predicted to be in-line or rise slightly from last reading

Personal Income & Spending (May 31): Expected to show moderation, with slow progress on disinflation

Core PCE Deflator (May 31): *THIS IS POWELL’S PREFERRED INFLATION MEASURE * - Expected to show a favorable reading for April, indicating slower but still persistent inflation

Market and Economic Outlook

US Equity Market: Nvidia's dominance still in spotlight, worrisome for sheer size and % of indices now

US Rates Market: Tempered expectations of Fed rate cuts are causing money funds to shorten maturities, with continuous T-bill supply

Commodities Market: Industrial metals are catching up with gold; long-term outlook favors metals, with talks of gold reaching $3K/oz

With these main macro factors I am looking at today, and so I remain quite diversified in asset classes to weather the continued uncertainty in risk assets coupled with the ongoing and persistent inflation. I am more concerned that if the market is impacted from an unforeseen event that the Fed wand Treasury will rush in to provide liquidity than a drawn out economic downturn leading to disinflation.

**Remember: The Treasury *needs* nominal GDP growth coupled with *negative* real rates. This points to ongoing allowance for inflation and refusal of precipitous asset disinflation.

As a result I'm not making substantive changes in my portfolios this month. I am happy where they stand.

->> LINK TO NEW PORTFOLIOS <<-

Portfolio Adjustments:

Overall, I remain widely diversified in asset class exposures:

Cash-equivalent T-Bills

Gold, silver and commodities

Bitcoin

Equities with select sector exposures

The one change I am making is not really significant, but I am consolidating the Energy exposures (GNR & GUNR) into GNR and and topping up the Uranium/Nuclear holdings (NLR) in the 10YR portfolio.

That's it.

If you have questions or ideas, you can find me in the Informationist Alpha community!

Talk soon,

James✌️