💡 Has The Fed Conquered Inflation?

Issue 135

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🫶 If this email was forwarded to you, then you have awesome friends, click below to join!

👉 And you can always check out the archives to read more of The Informationist. Premium subscribers have access to over 130 issues.

Today’s Bullets:

The Measures

The Current Status

The Short and Long of it

How to Protect Yourself

Inspirational Tweet:

The latest inflation data were released on Friday, and as Nick Timiraos (nicknamed Nikileaks on X, due to his alleged access to some sort of Fed’s inside hotline 🤨) points out, the number was “Not far from the Fed’s 2% target.”

So, is that it? Is the Fed’s inflation battle finished? They won?

Well, if you listen to White House economists, the answer is an emphatic YES.

But not for us. No, we will perform some much-needed critical thinking by reviewing these official inflation measures and how they may differ instead.

We’ll talk about the inflation trajectory and where we’re going, and perhaps most importantly, how we can protect ourselves along the way.

So, grab a nice big mug of coffee and settle into a comfortable seat for a Sunday peek into the world of inflation with The Informationist.

🤓 The Measures

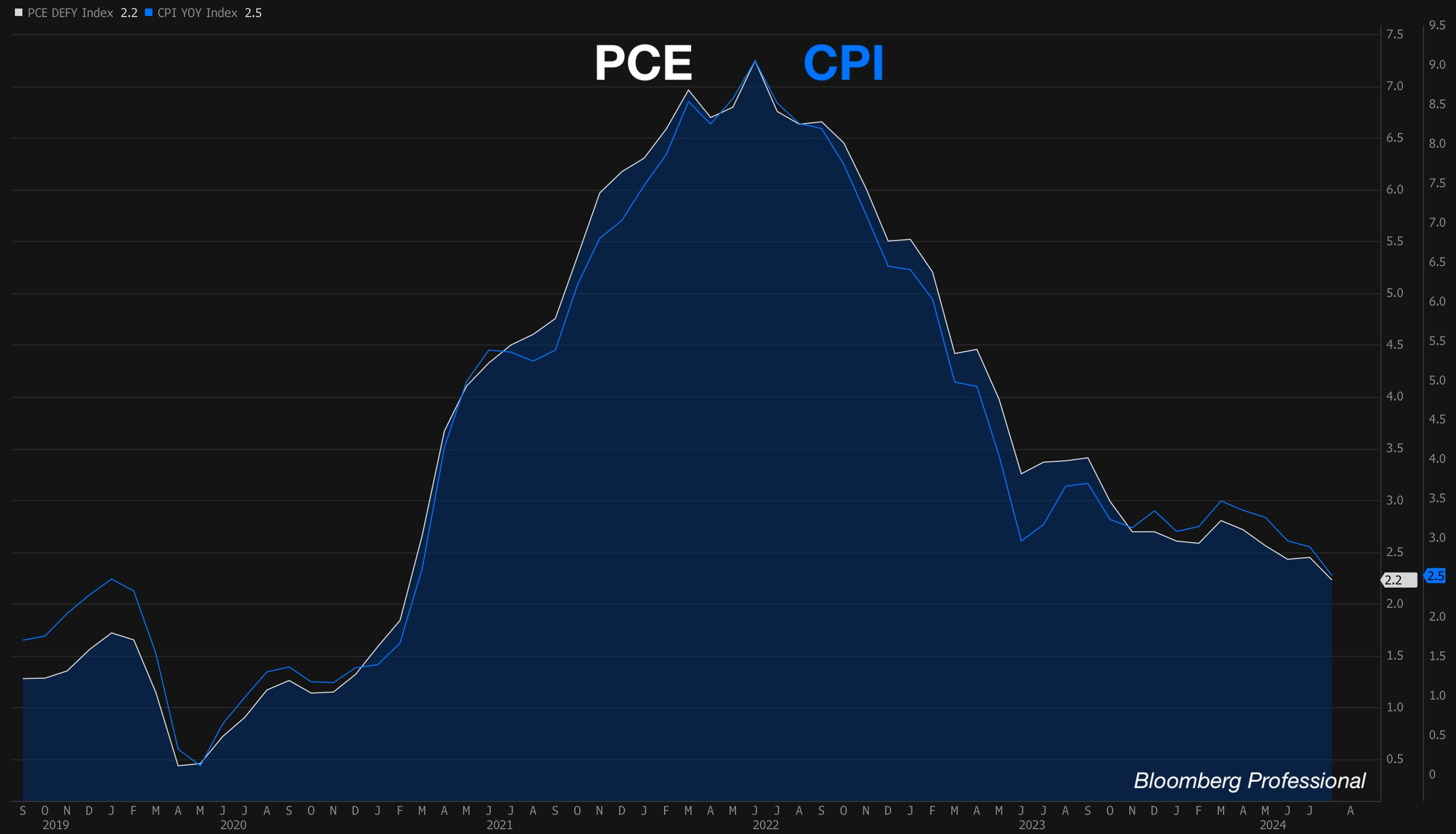

First off, we have two main measures of inflation that the Fed and investors watch, the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) index.

The CPI is compiled by the Bureau of Labor Statistics (BLS), and the PCE is measured by the Bureau of Economic Analysis (BEA). Both government-funded agencies.

Some key differences, though:

CPI measures price changes for a fixed basket of goods based on urban spending. Updated every 2 years, it uses something called the Laspeyres index, which can overstate inflation by not properly tracking consumer substitutions.

PCE tracks all household spending, including broader categories. Using a Fisher-Ideal index that better adjusts for substitutions, weights are updated frequently, providing a more responsive measure of inflation.

Because the PCE supposedly more accurately reflects consumer changes, the Fed has stated it prefers the PCE as its primary measure of inflation for policy decisions.

For those of you who want to learn more about CPI or PCE and their ‘challenges’, you can find full newsletters all about them here:

And a bit of TL;DR: The CPI relies solely on BLS surveys, tracking ~94K prices per month.

For PCE, the BEA uses multiple sources of data, including Census Bureau data, as well as various BLS surveys.

Did you catch that last part? The one about using BLS data?

That’s right. The PCE integrates some of the CPI and PPI data for its own inflation measure (using broader categories and different weightings, of course 🙄).

It’s no surprise, though, when charted together they look almost exactly the same.

So, two numbers, seemingly completely different methodology, but with the most important measure (inflation) being coordinated between the two.

Ah well, close enough for government work.

One more thing.

The Fed likes to use an adjusted form of CPI and PCE, namely the Core CPI and PCE.

If you’ve ever heard these terms and wondered what the heck they mean, it’s simple.

Core numbers just remove food and energy from the equations.

Why?

Because food and energy tend to be more volatile (they rise and fall more often) than the other components. And so, removing them can help smooth out short-term volatility and provide a more stable view of inflation trends.

I mean, who needs groceries and gas anyway, amiright? 🤡

Regardless, it’s a measure that Fed officials love love love to point to, unless of course, it doesn’t fit the story they are crafting to the public, that is…

About that.

🧐 The Current Status

You likely know that the Fed lowered the Fed Funds target rate by .5% last week.

In the Press conference, Powell said. “Our economy is strong overall and has made significant progress toward our goals over the past two years. The labor market has cooled from its formerly overheated state…Inflation has eased substantially from a peak of 7 percent to an estimated 2.2 percent as of August.”

Translated: the jobs market is softening, and though inflation has yet to settle down to 2%, it has apparently cooled enough for the Fed to act now.

But even then, this is still above 2%, and it isn’t the ‘preferred’ Core PCE measure, which just came in higher at 2.7%.

So, what gives?