💡 Greeks and Gamma Walls

Issue 137

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🫶 If this email was forwarded to you, then you have awesome friends, click below to join!

👉 And you can always check out the archives to read more of The Informationist.

Today’s Bullets:

Gamma

Vanna

Charm

All Together Now

Gamma Walls

Inspirational Tweet:

With the recent approval of Bitcoin ETF options and an uptick in volatility in MicroStrategy (MSTR), you have likely heard many pros talking about The Greeks lately.

Options Greeks, that is…

Like Delta, Gamma, and Vanna and more.

But they are super confusing, you say. I mean, what the heck do they mean and why do we care?

Good and important questions, and ones we will answer today.

But have no fear, this is not going to be an options class with lots of math. Or maths if you’re in the UK.

We will keep it nice and simple, as anyways, and limited to concepts only!

So, pour yourself a nice big cup of coffee and settle into your favorite seat for an easy walk through the land of options today with The Informationist.

📈 Gamma

First things first, and before we get rolling here, let’s review the simple concept of an option.

An option is simply the right to buy or sell a listed security at a certain price that expires on a certain day.

Buy = Call Option, and Sell = Put Option

I reviewed that, equity shorting, and more in a newsletter from earlier this year. You can find it here:

While it is unnecessary to read the above for today, I encourage you to go have a peek at some point, as we build off those concepts here.

But in order to understand the Greeks, we have to get in the heads of the dealers, the ones selling the options to customers/investors.

The base layer of all of this is volatility. In essence, higher volatility in a stock makes options in that stock more expensive and vice versa.

See, a dealer who sells an option is on the other side of the trade from the investor, and has to protect himself from this volatility.

Like this: Dealer sells a Call to the investor. Now the dealer is exposed to being short the stock of the call he sold.

How?

The investor bought the right to buy the stock at a certain price. And so, if the stock gets to that price, then the dealer has to sell it to him.

And unless the dealer already owns the stock in his own book, he will be short that stock.

Simple, right?

So, in order to manage this exposure, the dealer will use complex and sophisticated formulas like Black Scholes and proprietary models. This will tell him the amount he needs to be hedged at each price of the stock in order to protect himself from this exposure.

The Delta.

When delta changes, the dealer must re-hedge by either buying more of the stock or selling some of what he already bought.

If delta is .3, it means he should be long 30% of the stock of the call he sold. If delta is .5, then 50%, and so on…

And the exact opposite would be true if the dealer had sold a Put to the investor. The dealer would need to be short the stock to protect himself.

And so, delta helps us know what dealers are thinking and doing as the price of a stock changes.

These Greeks are known as second-order Greeks, as they affect the first Greek, Delta.

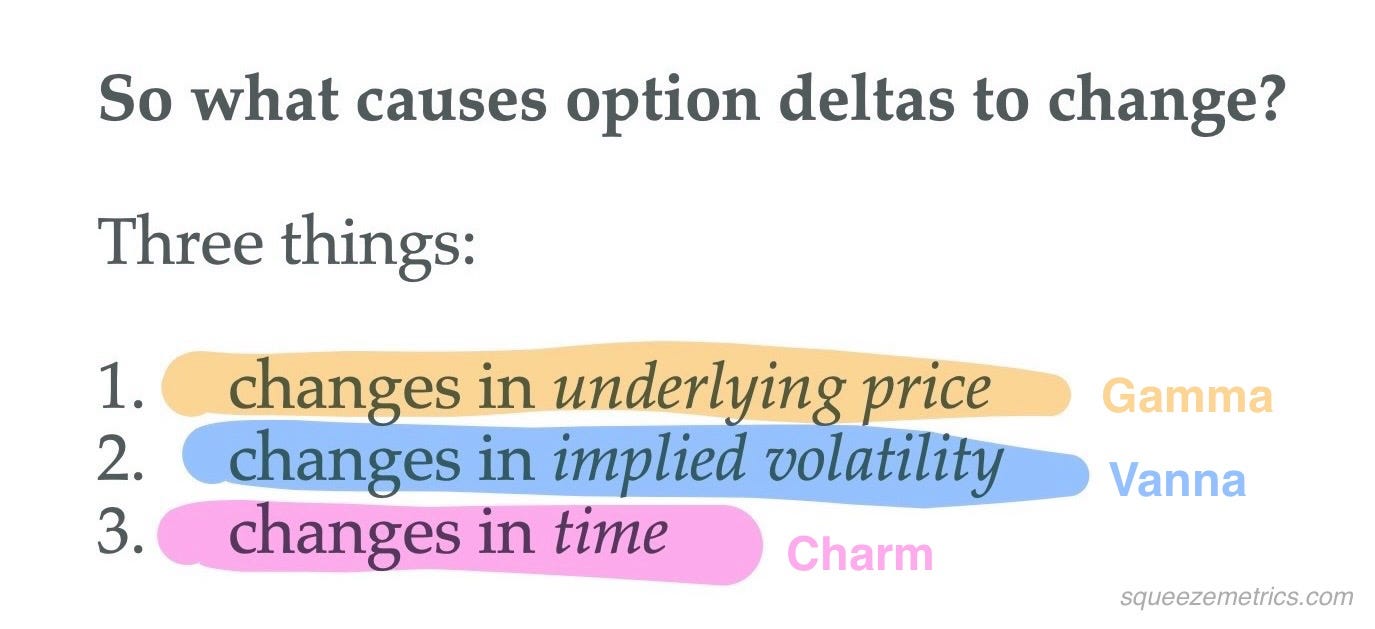

The first of these second-order Greeks is known as Gamma.

I know, finally.

Gamma tells us how sensitive an option's delta is to price changes of the underlying security. A higher gamma means delta changes more quickly.

As gamma increases, dealers need to make rapid adjustments to their hedging, buying or selling more stock as the underlying price moves.

Here’s where it gets fun, though.

When the price of the security gets close to the strike price of the option, where the customer gets to own it (call) or be short it (put), then the delta rises toward 1.0.

Where the dealer must be fully hedged in the security to protect himself.

This need can lead to amplified price movements—often referred to as a gamma squeeze.

Essentially an overreaction by the dealers scrambling to get hedged and protect themselves.

A few years ago, a Goldman Sachs equity derivatives strategist named Rocky Fishman explained: “gamma is one of the larger sources of non-fundamental economic activity in global markets. Market makers who delta-hedge their option positions are economically driven to trade substantial amounts of underlying shares or futures, strictly as a result of the price of the underlying itself changing, not as a result of fundamental news and without regard to the liquidity available. As a result, gamma can cause markets to overreact to fundamental news (short gamma) or to under-react to fundamental news (long gamma).”

Read that again, slowly.

The gamma squeeze.

Ouch.

OK, if that’s what happens to delta when the price of the underlying security changes, what happens when the volatility of the stock changes?

The velocity of the changes in price.

This is where the next second-order Greek comes into play.

Vanna.

🌪️ Vanna

Whereas gamma tells us how sensitive an option's delta is to price changes, Vanna measures the sensitivity of delta to changes in the security’s implied volatility.

Let’s unpack that.