Debt Ceilings and Is The US About to Default?

Issue LXI

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🧠 Sound smart? Feed your brain with weekly issues sent directly to your inbox:

Today’s Bullets:

Debt ceilings

Default on the horizon?

What are the markets saying?

What happens if US defaults (and how to position for it)?

Inspirational Tweet:

Here we are again, talking about debt ceilings and defaults. The Republicans offer a deal, but the Democrats won’t negotiate. Yet, if we don’t get to a resolution, the US will default on its debt.

We’ve heard it all before, many of us…many times before.

Just switch out the parties in the sentence above and plug it into past years’ battles.

Ah, the joys of political theater.

Problem is, this kind of theater has consequences. Like if after watching Les Misérables, you went back home, only to find your own house had been burnt down, too.

The irony.

But what exactly is the issue at hand? What’s the debt ceiling? Why are we approaching it? And what happens if this all doesn’t get resolved…and fast?

If this sounds confusing or daunting, no worries. We’ll unpack it all nice and easy, as always. So grab your coffee, get comfy, and settle in.

It’s Informationist time.

Join the 🧠Informationist community and get access to every single post + the entire archive of articles, all for a fraction of the cost of a college finance course.

You’ll learn a whole lot more, faster and easier. That’s my guarantee.

🤑 Debt ceilings

In the most basic terms, the debt ceiling is the limit to the amount the US Treasury can borrow.

In other words, it’s like the limit on a credit card. Once you reach that limit, you can no longer borrow any more and have to either take out a new credit card, or ask the bank to raise your limit.

Same thing here, but a few nuances.

First, the limit is set by Congress, not the Treasury itself. This means it can become a political football every time the limit is in danger of being breached. As we now witness.

See, the game here is for one party to make the other party look bad:

If the Democrats breach the limit without raising it, the government defaults on its debt. A big no-no, as we will discuss in a bit.

If the Democrats cut spending to avoid breaching the limit, it will upset special interest groups, i.e., campaign donors.

On the other side, the Republicans are not incentivized to cut spending themselves, because in this current cycle of debt madness, it is not their problem (as far as they are concerned, it all happened the Democrats’ watch).

And this is why it will get pushed right up to the edge, and a default could become not just possible, but in fact, likely.

Another nuance is that the federal government—Congress—has already committed to spending a certain amount of money. The Treasury isn’t asking for the ability to spend more, it’s asking for the ability to pay for what Congress has already spent.

Congress went shopping.

They spent and spent and spent.

And spent.

And…

Spent.

But now the bills are coming in, they have just a few bucks left in the bank, and their credit limit is fast approaching.

And their trusty executive (branch) assistant, the US Treasury, is soon going to be unable to send money for all the invoices.

And now Congress fights about whether to commit to spend less in the future or just raise the limit.

Meanwhile, they keep spending.

I would say it’s truly comical, if it wasn’t so serious. This reckless behavior of spending and raising and spending and fighting will someday haunt this country.

We are in a hopeless debt spiral, one we will never escape.

I’ve talked about this ad nauseam, and if you have somehow not heard me explain it yet, you can find a whole article about the debt spiral right here:

TL;DR: because the US operates in a perpetual deficit, the Treasury must borrow more each year to meet the country’s obligations. This borrowing only leads to a larger deficit, due to higher and higher interest expense, and more borrowing.

It is what we call a debt spiral, and there is no way out of it.

So instead, we just keep raising the limit and pretty much ignore the underlying spending problem.

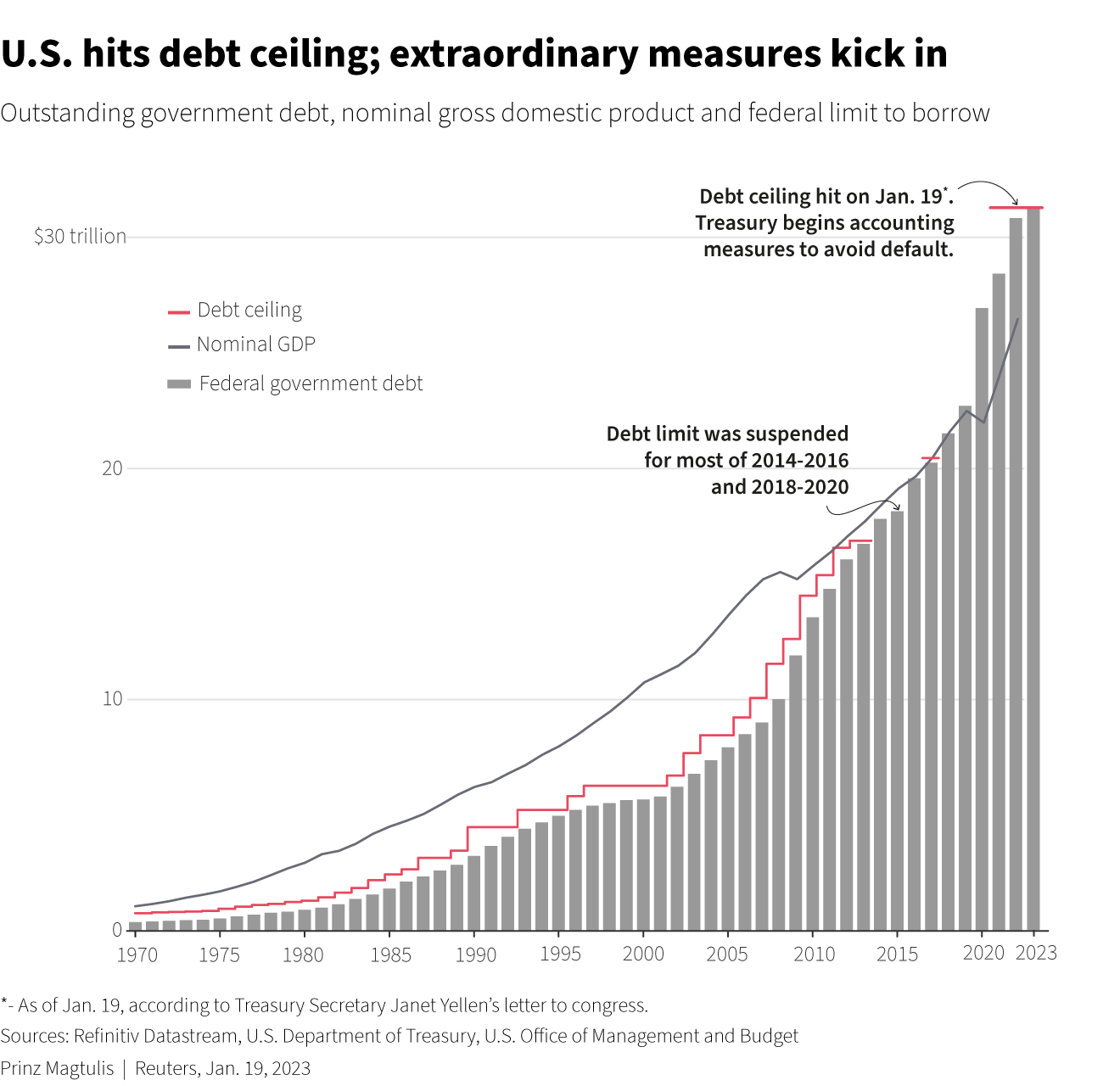

In fact, the US has raised the debt limit 78 times since 1960, and 22 times since 1997.

See that little note up in the right hand corner of the chart? The one that says we already reached the debt limit?

That’s right. We’re already there.

Remember this?

See, the truth is, the U.S. actually formally hit the debt limit on Jan. 19, and in order to buy time and avoid an imminent default, the Treasury has taken extraordinary measures, i.e., suspended new investments in the Civil Service Retirement and Disability Fund and the Postal Service Retiree Health Benefits Fund.

This is nothing more than an accounting maneuver, moving money around in the super complex and convoluted U.S. Treasury in order to stave off an actual default.

Yellen is living on borrowed time now.

But what happens if that last bar is the breached before raised again? Then what?

Put simply, the Treasury would then default on obligations, missing payments on various programs and services (ones they cannot simply put on pause like Civil and Postal Service Retirement funds), as well as payments and return of principle on federal debt.

Default on US Treasuries.

A very large no no, and one that could have short term impacts to the markets, as well as lasting impacts on the US Treasury’s cost to borrow (as we will get into in a bit).

So, how close are we then to a default? How much time does Congress have to wake up and smell the money printer?

Turns out, not as much time as they thought.

😳 Default on the horizon?

If you read the above article about the debt spiral, you know that the Congressional Budget Office periodically releases budget numbers and projections for the US Government’s P&L (read: losses) in the years ahead.

These numbers were recently updated, which I wrote all about here:

TL;DR: We’re still screwed. It’s only gotten worse, with the CBO’s expected deficit this year to be $1.4T, growing to ~$2T by 2028.

In the article, I explained how we would likely hit that $2T deficit mark this year, not 2028.

Low and behold. The Treasury just released the first 6-months’ budget results for 2023:

Yep, that’s $1.1T of deficit in the first six months. Some 1st grade math gives us a run-rate annual deficit of…

$2.2 Trillion.

Because tax receipts are far lower than the CBO expected, the Treasury will have to borrow more than expected.

In other words, they are already borrowing more, and this has accelerated the pace of breaching that debt ceiling.

So much for those extraordinary measures.

Instead of negotiating throughout the summer, as the CBO expected, that timeline has been pushed forward dramatically. In fact, Goldman Sachs just released a report on Tuesday, stating “weak tax collections so far in April suggest an increased probability that the debt limit deadline will be reached in the first half of June.”

And since we have only really seen partial data from individual tax returns, thus far, if capital gains taxes come in even lower than the current data, the timeline would be even worse.

It’s like Congress is standing on the train tracks and playing a game of chicken, in the fog.

They don’t know where the train is, or exactly how fast it is coming.

By the time they decide to act, it may be too late.

🧐 What are the markets saying?

There are two key pieces of data that are telling us exactly what the market is thinking and how it is handicapping the likelihood that the US does, in fact, default on its debt.

First, taking a peek at the short end of the yield curve, the 1-month and the 3-month US Treasuries, we can see that the market is attaching a huge premium on the 1-month paper versus the 3-month.

In fact, I’m unaware of there ever being a spread quite this large between durations just two-months apart.

If you buy a 1-month UST, you will be paid an annualized yield of 3.35%, and if you buy the 3-month UST, it would give you an annualized yield of 5.11%.

Whoa.

That’s a 1.75% yield premium for the longer paper.

The only difference between these two USTs is one matures two months later than the other. Normally, this would be seen as immaterial on the yield curve.

the risk of one not being paid on time.

In other words, the market is saying there is a high chance that the 3-month USTs will default.

And because investors cannot really buy the Fed Funds rate, they are all piling into the 1-month USTs, shortest USTs they can get their hands on, and avoiding the 3-month USTs.

Another place to look for clues is the CDS market.

I talked all about this in a recent newsletter that you can find here:

But to refresh, the short-term US sovereign CDS market has exploded since then.

The price of insuring against a default has doubled since January, now costing investors $130K per contract to protect $10 million of bonds.

This math suggests that the market is pricing in a 100% probability that the US defaults with a recovery of less than 98.71% today.

Put another way, the market believes that if the Treasury does default, they will pay back less than 98.71% of the principle.

Wow.

Clarification: What I believe the market is that investors are buying protection at extremely high costs to be compensated for the event that their supposedly matured debt capital becomes tied up in a technical default while Congress and the Treasury sort out details of making everyone whole after the fact.

In reality, if the Treasury defaults, it will be a technical default, in that they will eventually fix the debt ceiling situation, pay back all the principle and interest owed to the bondholders, and add in some extra interest to make up for the lost time value for money due to the delay.

So, the market is saying that investors are willing to pay for insurance against the loss of opportunity (aka, opportunity cost), in the event there is a default. Investors want access to all their capital and the ability to capitalize on market moves, accordingly.

And you should, too.

😱 What happens if US defaults (and how to position for it)?

Before going further, some of you may be asking, has this ever even happened before? Has the US ever defaulted due to debt ceiling showdowns?

The answer is yes.

In 1979, Congress was playing the same exact game of chicken with the debt ceiling. They waited, and waited, and waited…and waited to lift the ceiling. Raising it right at last moment.

Problem was, the Treasury’s accounting system was not equipped to get interest payments and checks in the mail fast enough, and the US technically defaulted for a short period of time.

All investors were paid the interest due and made whole, but it happened. Period.

As a result, short-term interest rates spiked by 60bps and remained higher for a number of months.

The main issue we now have is that all this discussion and focus on the US debt ceiling and possible default is making the world take notice of our desperate and deepening debt problem.

The political wrangling, the overspending, and any default places a giant 🎯 on our USTs.

Remember, the protracted debt ceiling standoff in 2011 is what prompted Standard & Poor's to downgrade the US credit rating for the first time, and the next day, the stock market crashed 5.5%.

As I have said before, at some point, the world will just stop trusting that the US always pays its debts. Or at the very least, in the short term, it will charge a premium to the US Treasury to borrow from them.

Because I attach a high probability that the US at least technically defaults on its debt this summer, I’m using the KISS principle, and am personally weighted heavily in fully FDIC-insured cash-equivalent securities in my portfolio.

This dry powder will allow me to take advantage of any market weakness due to a default, rather than having all my extra cash tied up in USTs that may be the victim of the exact reason that the market sells off.

Because I personally don’t trust the actors in this show.

Do you?

That’s it. I hope you feel a little bit smarter knowing about debt ceilings and defaults and have yourself positioned accordingly. Before leaving, feel free to respond to this newsletter with questions or future topics of interest.

And if you are a paid subscriber, leave a comment, answer a comment, join the awesome 🧠Informationist community below!✌️

Talk soon,

James

James,

When you say you are "weighted in FDIC- insured cash equivalent securities", aren't you saying your in money market funds that hold short term US treasuries? If yes, wouldnt those funds experience a short term liquidity problem in the event of a default? If yes, how is that better than holding one month treasuries directly?

Nothing is safe. Let’s just hope the commercial banks don’t default or more bank runs don’t occur. Could get 1930s nasty