💡A Tale of Two Economies

Issue 138

✌️ Welcome to the latest issue of The Informationist, the newsletter that makes you smarter in just a few minutes each week.

🙌 The Informationist takes one current event or complicated concept and simplifies it for you in bullet points and easy to understand text.

🫶 If this email was forwarded to you, then you have awesome friends, click below to join!

👉 And you can always check out the archives to read more of The Informationist.

Today’s Bullets:

The Cantillon Effect

Stimulus Checks

QE & Liquidity

Inflation’s Future

Inspirational Tweet:

An astute observation here by @StealthQE4, that there seems to be widespread consumer misery at the exact same time that markets are soaring to new highs.

So, what gives?

Well, it has to do with the Treasury and stimulus, the Fed and money printing, and relentless inflation disproportionately affecting some people versus others.

Something called The Cantillon Effect.

If you have been wondering caused and continues to cause this phenomenon (read: problem) and what you can do too protect yourself from—and maybe even benefit from—it, then you came to the right place today.

Because we are going to answer all these questions and a whole lot more, nice and easy as always, today.

So, grab your favorite cup of coffee and settle into a comfortable seat, as we dive into the haves and have-nots with this Sunday’s Informationist.

🤨 The Cantillon Effect

Truth is, @StealthQE4 is not the only one who senses something isn’t adding up here, perhaps you have felt it, too.

I see it all around.

I have friends who are absolutely thriving, portfolios rocking, houses priced at all-time highs, and others who have fallen behind, feel they can’t catch up or keep up, and are drowning in bills and rent payments.

Hoe could this be?

It is almost as if two economies emerged from the lockdowns.

What we are experiencing is called The Cantillon Effect, something I wrote about recently. If you have not yet read that piece or want a refresher, you can find it here:

For the TL;DR crowd: The Cantillon Effect is a term describing how those closest to newly created money—like bankers and politicians—benefit disproportionately before the rest of the economy feels its impact.

Named after economist Richard Cantillon, who profited from financial schemes himself 🙄, the concept studies the uneven distribution of wealth that arises from monetary expansion.

In modern day, the Fed’s Quantitative Easing (QE) programs create a similar effect, where financial institutions and asset holders benefit first, leaving wage earners and everyday consumers to be squeezed by the onset of inflation later.

But this last few years is a bit more nuanced, something we will get into in a bit.

First, let’s see what has been happening recently and then let’s dig into the why.

And finally, we will talk about what we can do about it to protect ourselves.

Forget about the quoted CPI inflation rate of 3%, this is a highly manipulated set of data that is created by the BLS, a government entity, that obfuscates the true effects of inflation over time. The reality is that most people are feeling inflation pain, and have been for years.

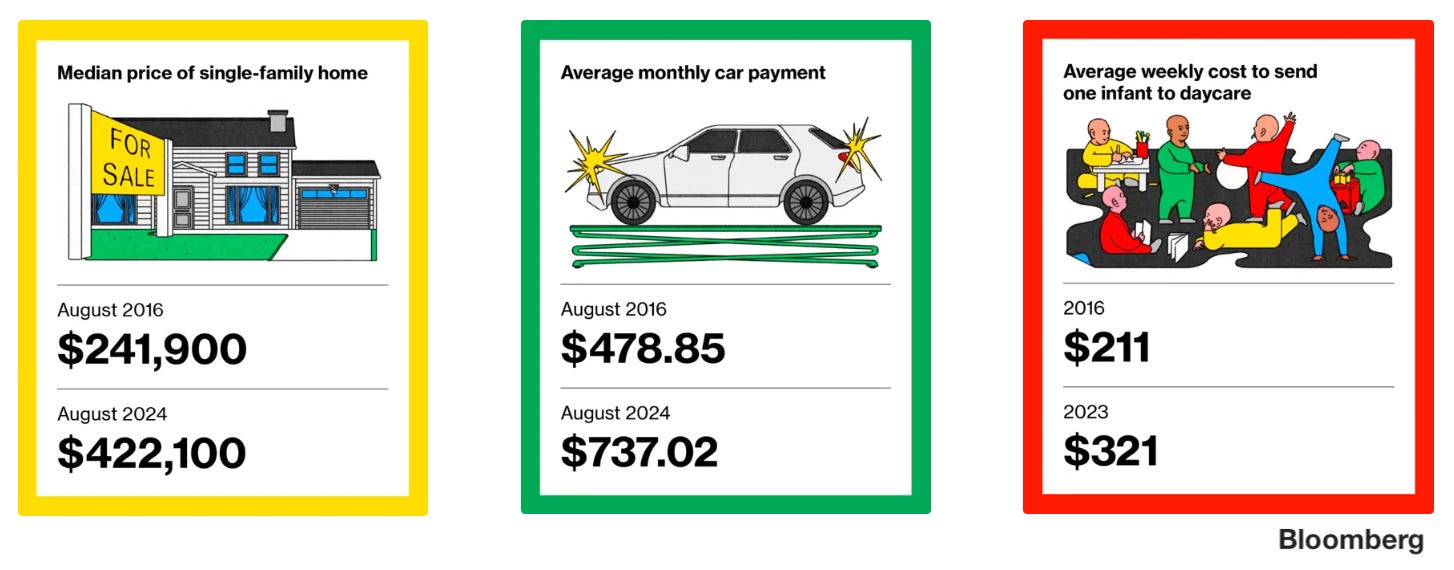

Let’s face it, it’s hard to have a conversation about inflation and not have rent or housing costs come up. In fact, just eight years ago, it would have taken about 13 years to save up enough money for a 20% down-payment on a median-priced home.

Today, it takes about 20 years to accumulate the same down payment on the same home.

Even worse, the monthly mortgage payment on that median-priced house, has doubled from 14% of median income in 2016 to 26% this year.

Ouch.

Car payments aren’t much better, up an average 54%, and daycare was up about the same amount over a year ago.

Factor in food and gas and the rest of the essentials, and because these expenses make up a large proportion of their overall earnings, it has become simply impossible for many lower-income consumers to keep up.

So, what do they do? Charge it, of course. Evidenced here, with balances rising fast:

But many people received stimulus checks, right? Didn’t that help?

Initially yes, as you can see credit card balances being reduced in 2020 and 2021, but more on that.

🤑 Stimulus Checks

As you recall, The White House sent out a series of Stimulus Checks, two under Trump and one under Biden, for a total of $3,200 per individual, $6,400 per couple, and $2,400 per dependent/child.

These checks went to anyone whose income was $75K for individuals and $150K for married couples filing jointly, with phase outs above these levels.

And what did each income-level do with these checks? Let’s see: